Among all banking categories, Small Finance Banks are currently leading the interest rate spectrum.Among all banking categories, Small Finance Banks are currently leading the interest rate spectrum.

Among all banking categories, Small Finance Banks are currently leading the interest rate spectrum.Among all banking categories, Small Finance Banks are currently leading the interest rate spectrum.Fixed deposit (FD) rates across India are witnessing a clear divergence, with Small Finance Banks (SFBs) offering the most attractive returns, followed by select private banks and NBFCs. Recent data as of April 17, 2026, indicates that SFBs have emerged as the top yield providers, while public sector banks continue to offer relatively lower but stable rates.

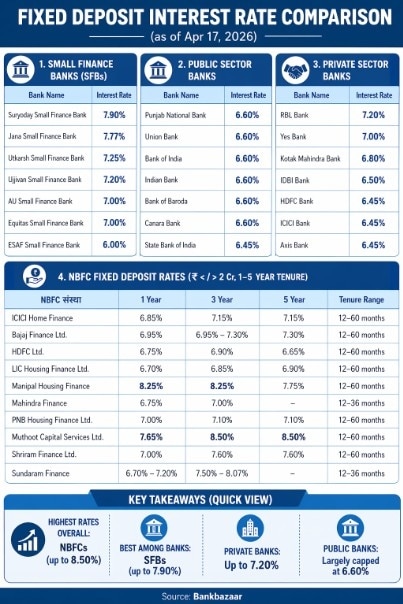

SFB FD rates

Among all banking categories, Small Finance Banks are currently leading the interest rate spectrum. Suryoday Small Finance Bank tops the chart with FD rates of 7.90%, followed by Jana Small Finance Bank at 7.77% and Utkarsh Small Finance Bank at 7.25%. Ujjivan SFB offers 7.20%, while AU and Equitas SFBs are at 7.00%. ESAF SFB trails slightly at 6.00%. The higher rates offered by SFBs reflect their need to attract deposits to fund credit growth, particularly in underserved and retail segments.

Do checkout: FD Calculator: Fixed Deposit Calculator, Invest in FD Online

Private vs public banks

In comparison, private sector banks offer moderately competitive rates. RBL Bank leads at 7.20%, followed by Yes Bank at 7.00% and Kotak Mahindra Bank at 6.80%. Large lenders such as HDFC Bank, ICICI Bank, and Axis Bank offer rates in the range of 6.45%–6.50%, while IDBI Bank stands at 6.50%.

Public sector banks, meanwhile, remain conservative in their offerings. Most PSU banks—including Punjab National Bank, Union Bank, Bank of India, Indian Bank, Bank of Baroda, and Canara Bank—offer 6.60%, while State Bank of India provides 6.45%.

This spread highlights a roughly 100–150 basis points gap between SFBs and large public banks.

NBFC FDs

Non-Banking Financial Companies (NBFCs) continue to offer competitive FD rates, often surpassing traditional banks across select tenures.

Muthoot Capital Services offers up to 8.50% for 3- and 5-year tenures

Manipal Housing Finance provides up to 8.25% for shorter durations

Shriram Finance offers 7.60% for 3- and 5-year deposits

PNB Housing Finance and Bajaj Finance provide rates up to 7.10%–7.30%

Other players like ICICI Home Finance, LIC Housing Finance, and HDFC Ltd. offer relatively stable returns in the 6.65%–7.15% range.

NBFCs determine FD rates based on repo rate trends, internal cost of funds, and profitability requirements. They raise capital through bonds, commercial papers, long-term lending spreads, and foreign investments.

Key features of NBFC fixed deposits

AAA-rated NBFC FDs (ICRA/CRISIL) are generally considered relatively safe

Senior citizens typically receive an additional 0.25% interest

Interest earned is fully taxable

NBFCs cannot issue cheques as they are outside the payment settlement system

Investment perspective

For yield-focused investors, SFBs and NBFCs present compelling opportunities, offering returns significantly higher than traditional banks. However, the risk-return trade-off remains critical. While PSU banks provide safety and stability, SFBs and NBFCs demand closer scrutiny of credit ratings, liquidity, and issuer credibility.

'Iran taking too long to negotiate a deal, will have to pay the price': Trump's fresh warning to Tehran

'Iran taking too long to negotiate a deal, will have to pay the price': Trump's fresh warning to Tehran Centre likely to take measures to stem net FDI outflows

Centre likely to take measures to stem net FDI outflows Why is India’s obesity drug market thinning despite the GLP-1 rush?

Why is India’s obesity drug market thinning despite the GLP-1 rush? Planning to fly from Jewar? Air India Express pulls out. What changes for you

Planning to fly from Jewar? Air India Express pulls out. What changes for you Shocker for Mamata: Saayoni Ghosh, Yusuf Pathan, Shatrughan Sinha among 19 TMC MPs on rebel list

Shocker for Mamata: Saayoni Ghosh, Yusuf Pathan, Shatrughan Sinha among 19 TMC MPs on rebel list Why SpaceX, OpenAI, Anthropic IPOs Are A Pipe Dream For Indian Investors

Why SpaceX, OpenAI, Anthropic IPOs Are A Pipe Dream For Indian Investors Why Are Oil Prices Cooling Despite Renewed U.S.-Iran War ? | Narendra Taneja

Why Are Oil Prices Cooling Despite Renewed U.S.-Iran War ? | Narendra Taneja Foreign Capital Could Return As Oil Prices Stabilise, Market Outlook Improves

Foreign Capital Could Return As Oil Prices Stabilise, Market Outlook Improves PoK Uprising: 27 Dead As Pakistan Army Cracks Down On Banned JAAC Protests; India Demands Justice!

PoK Uprising: 27 Dead As Pakistan Army Cracks Down On Banned JAAC Protests; India Demands Justice! Market Commentary: Ashish Kila's Wealth-Creation Strategy For Investors

Market Commentary: Ashish Kila's Wealth-Creation Strategy For Investors Ather Energy, Ola Electric, Bajaj Auto or TVS Motor: Which EV two-wheeler stock is best placed for the next leg of growth?

Ather Energy, Ola Electric, Bajaj Auto or TVS Motor: Which EV two-wheeler stock is best placed for the next leg of growth? Trapped at the Terminal - Where Even Your Stop-Loss Won't Work

Trapped at the Terminal - Where Even Your Stop-Loss Won't Work Stock market today: Why Nifty failed to hold gains and closed lower

Stock market today: Why Nifty failed to hold gains and closed lower SpaceX IPO demand surges as investors chase Elon Musk's biggest market bet

SpaceX IPO demand surges as investors chase Elon Musk's biggest market bet Bharti Airtel vs Vodafone Idea: Poring over key financials of telcos

Bharti Airtel vs Vodafone Idea: Poring over key financials of telcos