In the current environment, where gold prices are fluctuating and equity markets are volatile, FDs provide capital protection, assured returns.In the current environment, where gold prices are fluctuating and equity markets are volatile, FDs provide capital protection, assured returns.

In the current environment, where gold prices are fluctuating and equity markets are volatile, FDs provide capital protection, assured returns.In the current environment, where gold prices are fluctuating and equity markets are volatile, FDs provide capital protection, assured returns.Fixed deposit (FD) schemes are regaining prominence in the current volatile market environment, offering stability and predictable returns as equity and commodity markets remain uncertain. With interest rates still elevated, FDs are increasingly being viewed as a safe parking option for surplus funds, particularly among conservative investors.

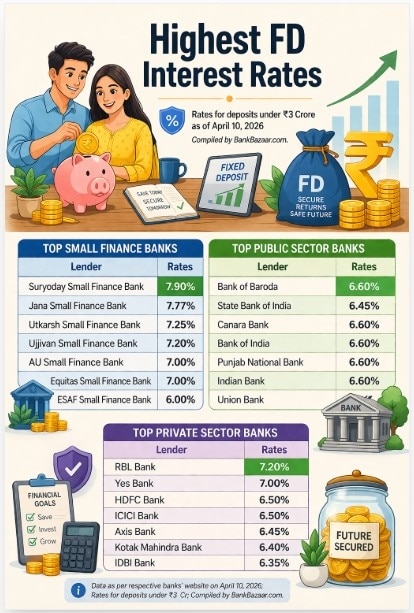

According to data compiled by BankBazaar from respective banks’ websites (as of April 10, 2026), FD rates continue to remain attractive across tenures, with small finance banks leading the pack.

Rates steady for now

The Reserve Bank of India (RBI), in its first Monetary Policy Committee (MPC) meeting for FY 2026–27, kept the repo rate unchanged at 5.25% and maintained a neutral stance. Since FD rates are closely linked to the interest rate cycle, this pause indicates that deposit rates are likely to remain stable in the near term.

For investors, this creates a window to lock in relatively higher rates before any potential shift in the rate cycle.

1–3 year FD rates

For shorter tenures of 1–3 years, small finance banks are offering significantly higher returns compared to their larger counterparts. Suryoday Small Finance Bank tops the chart with rates of around 7.90%, followed by Jana Small Finance Bank at 7.77% and Utkarsh Small Finance Bank at 7.25%. Ujjivan and AU Small Finance Banks offer rates in the 7.00–7.20% range.

In comparison, private sector banks such as RBL Bank and Yes Bank offer up to 7.00%, while HDFC Bank and ICICI Bank are offering around 6.50%. Among public sector banks, rates are relatively lower, with Bank of Baroda at 6.40% and State Bank of India at 6.30%.

ALSO READ: Akshaya Tritiya Special: Gold vs stocks — What gives you better returns; what history suggests

3–5 year FD rates

For longer tenures of 3–5 years, rates remain broadly stable but slightly more uniform across banks. Public sector banks such as Punjab National Bank, Union Bank, Bank of India, Indian Bank, Bank of Baroda, and Canara Bank are offering around 6.60%, while SBI offers about 6.45%.

Private sector banks continue to offer a slight premium. RBL Bank stands out with 7.20%, followed by Yes Bank at 7.00% and Kotak Mahindra Bank at 6.70%. HDFC Bank, ICICI Bank, and Axis Bank are clustered around 6.45–6.50%.

ALSO READ: Gold ETF vs Sovereign Gold Bond vs physical gold — which is smarter investment this Akshaya Tritiya?

Small finance banks FD rates

Small finance banks remain the most competitive segment in the FD space, offering rates ranging from 6.00% to as high as 7.90% for comparable tenures. ESAF Small Finance Bank offers around 6.00%, while Equitas and AU Small Finance Banks offer about 7.00%. These higher rates reflect their need to attract deposits, though investors should balance returns with considerations such as deposit insurance limits and bank-specific risk factors.

Why FDs are gaining traction again

In the current environment, where gold prices are fluctuating and equity markets are volatile, FDs provide capital protection, assured returns, and flexibility across tenures. They also serve as an effective tool for portfolio diversification, especially for risk-averse investors.

ALSO READ: Will gold prices rise after Akshaya Tritiya? What history shows

With the RBI maintaining status quo on rates, FD yields are likely to remain at current levels in the near term. Historically, FD rates tend to decline when the interest rate cycle turns downward, making the present phase attractive for locking in higher returns.

For investors with idle cash or those seeking stability, FDs offer a compelling opportunity to secure predictable income while insulating a portion of their portfolio from market volatility.

'Human capital is...': Satya Nadella says AI success will hinge on ecosystems, not frontier models

'Human capital is...': Satya Nadella says AI success will hinge on ecosystems, not frontier models FinMin notifies expanded class of overseas individual investors for listed equities

FinMin notifies expanded class of overseas individual investors for listed equities ‘We’re close to peace’: Trump rebukes Israel over Beirut strike; Iran says attack ‘won’t go unanswered’

‘We’re close to peace’: Trump rebukes Israel over Beirut strike; Iran says attack ‘won’t go unanswered’ FIFA World Cup 2026 in India: Where to watch live and free on mobile

FIFA World Cup 2026 in India: Where to watch live and free on mobile How much gold, equity and debt should you hold in uncertain times? Experts explain

How much gold, equity and debt should you hold in uncertain times? Experts explain I.T. And Real Estate Stocks: Expert Reveals His Top Stock Picks For The Next Rally

I.T. And Real Estate Stocks: Expert Reveals His Top Stock Picks For The Next Rally “The World Is Rebalancing”: EAM Jaishankar Explains Why Global Politics Is Getting Messier

“The World Is Rebalancing”: EAM Jaishankar Explains Why Global Politics Is Getting Messier Xi Jinping Meets Kim Jong Un In Pyongyang: China Counters Russia, Warns U.S. In Mega Power Shift

Xi Jinping Meets Kim Jong Un In Pyongyang: China Counters Russia, Warns U.S. In Mega Power Shift I.T. Stocks Crashed Too Much? Expert Says These Stocks Could Surprise

I.T. Stocks Crashed Too Much? Expert Says These Stocks Could Surprise Explained: Why Rawalakot & Muzaffarabad Are Burning & The Real 1947 History Behind The Crisis!

Explained: Why Rawalakot & Muzaffarabad Are Burning & The Real 1947 History Behind The Crisis! ITC shares trading strategy: Stock in consolidation mode - Road ahead for investors

ITC shares trading strategy: Stock in consolidation mode - Road ahead for investors HDFC Bank, ICICI Bank, Axis Bank, RBL Bank, IndusInd Bank, BOB, SBI: Target prices

HDFC Bank, ICICI Bank, Axis Bank, RBL Bank, IndusInd Bank, BOB, SBI: Target prices Vedanta demerger entities listing: Valuations, debt allocation, expert views & fair values

Vedanta demerger entities listing: Valuations, debt allocation, expert views & fair values Vedanta demerger: Aluminium vs Power vs Oil & Gas vs Iron & Steel — Which stock to buy after listing?

Vedanta demerger: Aluminium vs Power vs Oil & Gas vs Iron & Steel — Which stock to buy after listing? 'SpaceX valuation does not fit any traditional matrix': Uday Kotak on historic IPO

'SpaceX valuation does not fit any traditional matrix': Uday Kotak on historic IPO