From April 1, 2026, TCS on education remittances above ₹10 lakh drops to 2%, and tour packages move to a flat 2% rate.

From April 1, 2026, TCS on education remittances above ₹10 lakh drops to 2%, and tour packages move to a flat 2% rate. From April 1, 2026, TCS on education remittances above ₹10 lakh drops to 2%, and tour packages move to a flat 2% rate.

From April 1, 2026, TCS on education remittances above ₹10 lakh drops to 2%, and tour packages move to a flat 2% rate.In the Union Budget 2026–27, Finance Minister Nirmala Sitharaman proposed a restructuring of the Tax Collected at Source (TCS) framework to simplify compliance and rationalise rates across categories. Presenting her ninth consecutive Budget, she said the changes are aimed at reducing multiplicity in TCS rates while easing upfront cash outflows for taxpayers.

Under the proposals, TCS on the sale of alcoholic beverages for human consumption will rise from 1% to 2%. The rate on tendu leaves will be reduced from 5% to 2%, while scrap will see an increase from 1% to 2%. Similarly, the TCS rate on minerals such as coal, lignite and iron ore has been proposed to be raised from 1% to 2%.

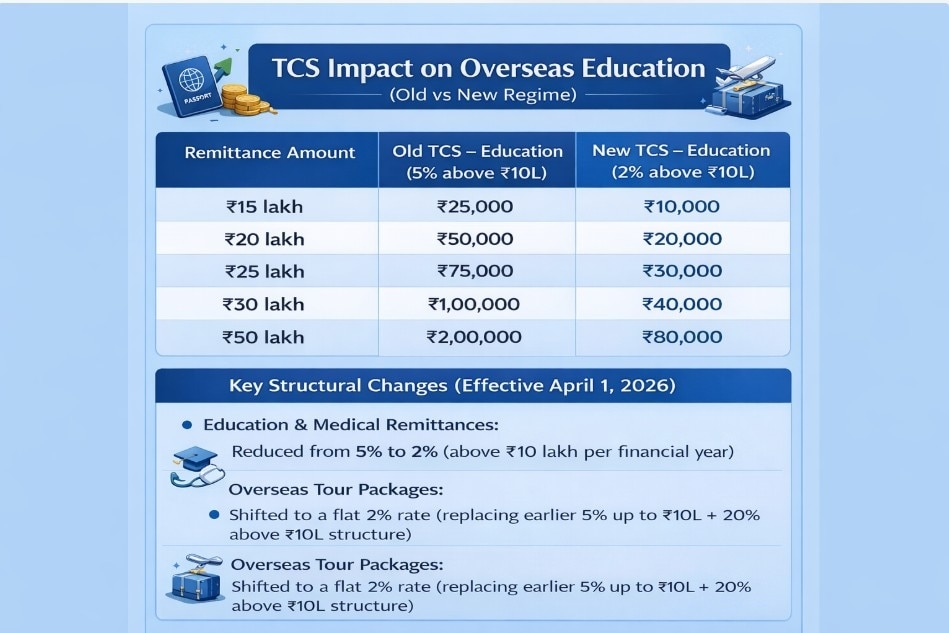

Significant relief has been proposed for households incurring overseas education and medical expenses. The TCS rate under the Liberalised Remittance Scheme (LRS) for education and medical treatment exceeding ₹10 lakh has been reduced from 5% to 2%. For overseas tour packages, the rate has been cut to 2% across all slabs, including amounts above ₹10 lakh, where it earlier stood at 20%.

Ankit Mehra, CEO & Founder of GyanDhan, explains the implications in detail.

Q1. Can you explain the key changes in the revised TCS framework and how they differ from the earlier regime for overseas education expenses?

Answer: The revised TCS framework under the Liberalised Remittance Scheme (LRS) significantly rationalises upfront tax collection on overseas remittances.

Earlier:

Overseas education remittances attracted 5% TCS above ₹10 lakh per financial year.

Non-education categories, such as tour packages, attracted 5% up to ₹10 lakh and 20% beyond ₹10 lakh.

Revised (effective April 1, 2026):

Education and medical remittances: 2% TCS above ₹10 lakh

Overseas tour packages: flat 2%

The key difference is liquidity relief. While TCS was always adjustable against final income tax liability, the earlier regime blocked significantly higher capital at the time of transfer.

Q2. How has the higher TCS rate altered the upfront cost of studying abroad for middle-class families?

Answer: TCS is not an additional tax; it is collected in advance and adjusted during income tax filing. However, it directly impacts immediate cash flow.

Example: ₹30 lakh remittance under the old regime meant ₹1,00,000 blocked as TCS.

Under the revised regime, it becomes ₹40,000.

Immediate liquidity released: ₹60,000.

For middle-class families funding tuition, visa, insurance and living costs simultaneously, this difference can determine whether they dip into emergency savings.

Q3. Which categories of students or families are most affected by the revised TCS norms, and why?

Answer: The most affected segments are:

Self-funded middle-income families remitting above ₹10 lakh annually

Families funding living expenses separately from tuition

Parents supporting multiple children studying abroad

These households rely on accumulated savings, fixed deposits or partial asset liquidation, making upfront liquidity critical.

Education loans remain largely insulated. Earlier, loan-funded remittances attracted only 0.5% TCS above ₹7 lakh. Under the revised framework, loan-funded cases continue to benefit from concessional or near-zero effective TCS structures depending on the lender.

Q4. Has the new framework changed the choice of destination countries or universities?

Answer: TCS does not directly dictate destination choice but influences affordability perception.

For example, if a family has ₹30 lakh allocated, under the old regime ₹1 lakh was blocked immediately. Under the revised structure, only ₹40,000 is blocked. That improves financial flexibility, even if aspirations remain unchanged.

Q5. Are families delaying or restructuring education loans to manage the TCS impact?

Answer: Visa timelines and university payment deadlines remain the primary drivers. Most families are not delaying education loans solely due to TCS changes.

Under the earlier regime, loan-funded remittances attracted only 0.5% TCS above ₹7 lakh, compared to 5% for self-funded remittances above ₹10 lakh. Under the revised regime, self-funded remittances now attract 2% TCS above ₹10 lakh, while loan-funded remittances continue to enjoy concessional treatment.

Q6. How significant is the cash-flow impact?

Answer: The impact is meaningful because TCS is collected instantly but refunded only after income tax filing.

For middle-income households:

₹1–2 lakh may remain blocked for several months

No interest is earned

Families may rely on short-term borrowing

Effectively, families provide an interest-free float.

Q7. Have you seen a shift towards scholarships or alternative funding?

Answer: Students have always sought scholarships and assistantships. Under higher TCS regimes, lower remittance automatically reduced TCS exposure, increasing their attractiveness. The revised 2% structure reduces this distortion but does not eliminate the push toward cost efficiency.

Q8. What challenges do families face in claiming TCS refunds?

Answer: There are many challenges, these include:

Limited awareness of TCS credits in Form 26AS

Delays in reconciliation

Tax filing literacy gaps

Confusion between TCS and TDS

For first-time overseas education funders, this creates psychological stress.

Q9. Could TCS discourage overseas education?

Answer: TCS alone does not discourage overseas education. However, when combined with rising tuition, forex volatility and living cost inflation, higher upfront blockage amplified affordability concerns. The revised structure mitigates that pressure.

Q10. How are consultants, banks and universities responding?

Answer: Consultants can position this as positive for overseas education. Banks and NBFCs may use it to offer structured financing solutions, though education loans were never heavily impacted by high TCS.

Q11. What are the key numerical differences between old and new regimes?

Q12. How do the revised TCS rules impact students' funding for education through bank or NBFC education loans?

Answer: This remains consistent with the earlier explanation. Education loans are largely insulated from major disruption under the revised framework.

Under the earlier regime, remittances funded through education loans from specified banks and NBFCs attracted a concessional 0.5% TCS on amounts exceeding ₹7 lakh per financial year. In contrast, self-funded remittances above ₹10 lakh attracted 5% TCS.

Under the revised regime effective April 1, 2026, while self-funded remittances now attract 2% TCS above ₹10 lakh, loan-funded remittances continue to benefit from concessional or near-zero effective TCS structures depending on the lending institution and compliance structure. Therefore, loan-funded cases remain structurally less exposed to liquidity pressure.

Q13. Has the differential treatment of loan-funded versus self-funded expenses changed financing decisions?

Answer: Yes, the differential TCS rates meaningfully influenced financing behaviour, especially among middle-income households.

Under the earlier 5% regime, families remitting ₹40–50 lakh annually would see ₹1.5–2 lakh blocked immediately as TCS. Although refundable, it created a temporary liquidity gap.

As a result:

Loans were used strategically as working capital management tools.

Families preferred structured disbursement via banks rather than liquidating long-term investments.

Under the revised 2% regime:

₹50 lakh remittance

Earlier: ₹2 lakh TCS

Now: ₹80,000 TCS

This sharply reduces liquidity pressure. Financing decisions are now shifting back to rational comparisons between:

Cost of borrowing (9–12%)

Opportunity cost of liquidating investments

Tax efficiency and liquidity comfort

The earlier distortion caused by high upfront TCS has reduced.

Q14. What is the cash-flow impact on families directly funding tuition and living costs abroad?

Answer: Parent-led funding faces the highest first-year impact because remittances are front-loaded.

Typical first-year outflow:

Tuition: ₹20–30 lakh

Living expenses: ₹8–12 lakh

Insurance, visa, flights, deposits: ₹2–3 lakh

Total: ₹35–45 lakh.

Under the earlier 5% regime:

₹40 lakh → ₹1.5 lakh blocked

₹50 lakh → ₹2 lakh blocked

Under the revised 2% regime:

₹40 lakh → ₹60,000 blocked

₹50 lakh → ₹80,000 blocked

Blocking ₹1–2 lakh earlier could disrupt liquidity buffers. The 2% regime materially eases first-year financial compression.

Q15. Under the new regime, how much additional upfront outlay are families facing?

Answer: For a middle-income household earning ₹15–25 lakh annually, freeing up ₹1 lakh in working capital is significant. It can cover months of expenses or hedge forex volatility.

While TCS was never an additional tax long-term, the upfront blockage functioned as a friction cost.

Q16. How does timing of TCS collection and refund affect households?

Answer: The structural issue is timing mismatch.

TCS is collected immediately at remittance.

Refund or adjustment happens during income tax filing later.

This means:

Funds remain blocked for 6–12 months.

No interest accrues.

Families effectively provide an interest-free advance.

Households may:

Use short-term credit

Pay 12–18% interest on personal loans

Deplete emergency funds

Thus, the issue is liquidity timing, not taxation.

Q17. Are parents restructuring savings or borrowing plans?

Answer: Under the earlier regime, families:

Liquidated fixed deposits prematurely

Redeemed mutual funds at suboptimal timing

Increased short-term borrowing

Split remittances across financial years

Timed payments near year-end to accelerate refunds

Liquidity planning became as critical as university selection. Under the 2% regime, such tactical adjustments may reduce, though financial discipline remains essential amid rising tuition and forex volatility.

Q18. Has the revised framework increased reliance on education loans?

Answer: Earlier, higher TCS nudged families toward loans because:

Loan disbursements are staggered

Banks remit directly to universities

EMIs begin post-moratorium

Section 80E deductions apply

Borrowing at 9–11% was sometimes preferable to locking ₹1–2 lakh.

Under the revised 2% structure, this behavioural push softens. Loans remain attractive when:

Investment returns exceed borrowing costs

Families want to preserve retirement capital

Risk diversification is prioritised

The revised regime restores financing neutrality.

Q19. What challenges do taxpayers face in tracking and claiming TCS credits?

Answer: Operational challenges remain:

Bank-reported TCS must reflect in Form 26AS and AIS.

PAN mismatches delay credit.

Taxpayers must correctly report remittance details.

Many first-time funders lack reconciliation familiarity.

Common confusion includes:

TCS vs TDS

Whether refunds are automatic

Timeline for receipt

For middle-income families without tax advisors, this can be intimidating. Fintech platforms and banks can simplify digital reconciliation and improve literacy.

Big news for commercial petrol, diesel buyers: India lifts emergency curbs on retail sales from July 1

Big news for commercial petrol, diesel buyers: India lifts emergency curbs on retail sales from July 1 ") 'Never seen so many tankers': India's Russian crude imports may hit record high in June

'Never seen so many tankers': India's Russian crude imports may hit record high in June Delhi EV Policy 2026 Explained: What's changing for car, bike and auto buyers

Delhi EV Policy 2026 Explained: What's changing for car, bike and auto buyers space – Prism Hybrid Long-Short Fund") Why Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF space

Why Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF space Where should investors put their money? PL Wealth CEO has some tips

Where should investors put their money? PL Wealth CEO has some tips  Why Jio BlackRock AMC Is Launching Hybrid Long-Short As It's First SIF

Why Jio BlackRock AMC Is Launching Hybrid Long-Short As It's First SIF Delhi Unveils ₹15,000 Crore EV Policy: What It Means For Auto Companies And Consumers

Delhi Unveils ₹15,000 Crore EV Policy: What It Means For Auto Companies And Consumers Gold, Silver Or Crude? Where Should Investors Bet Now? | Vandana Bharti

Gold, Silver Or Crude? Where Should Investors Bet Now? | Vandana Bharti How India Strategically Managed LPG & Crude Oil Supplies During West Asia War | K. Surana Explains

How India Strategically Managed LPG & Crude Oil Supplies During West Asia War | K. Surana Explains Delhi’s Green Revolution: CM Rekha Gupta Unveils Massive ₹15,000 Crore EV Policy To Combat PollutionWhy Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF spaceWhere should investors put their money? PL Wealth CEO has some tips

Delhi’s Green Revolution: CM Rekha Gupta Unveils Massive ₹15,000 Crore EV Policy To Combat PollutionWhy Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF spaceWhere should investors put their money? PL Wealth CEO has some tips  Axis Bank CFO Puneet Sharma steps down; stock likely in focus on Tuesday

Axis Bank CFO Puneet Sharma steps down; stock likely in focus on Tuesday Apollo Hospitals, Medanta, Healthcare Global, Max Healthcare, Artemis Medicare: Check target prices, outlook

Apollo Hospitals, Medanta, Healthcare Global, Max Healthcare, Artemis Medicare: Check target prices, outlook Polycab: Amid record FII buying, shares at all-time high but brokerages expect more upside

Polycab: Amid record FII buying, shares at all-time high but brokerages expect more upside