Niranjan Avasthi, Senior Vice President at Edelweiss Mutual Fund, emphasises that the ₹40 crore estimate is valid only under specific conditions. “The number sounds alarming, but it depends heavily on the kind of inflation and lifestyle trajectory you assume,” he said.

The math behind the ₹40 crore figure

The logic supporting a ₹40 crore corpus rests on three key variables: inflation, time horizon, and life expectancy. According to wealth manager Sandeep Jethwani, an individual currently spending ₹2 lakh per month in a metro city could see that expense rise sharply over two decades due to compounding inflation.

Urban households often experience inflation closer to 8–10%, significantly higher than headline CPI. This is driven by rising healthcare costs (12–14%), domestic wages (10–12%), and discretionary spending such as travel and education. Over 20 years, this can push a ₹2 lakh monthly expense to over ₹11 lakh per month, or roughly ₹1.3 crore annually at retirement.

Add to this a retirement period of 25–30 years, and the total corpus requirement can approach ₹35–40 crore, especially if post-retirement returns only partially offset inflation.

Inflation isn’t one number

However, experts caution against treating inflation as a single, fixed figure. Avasthi breaks it into two components: price inflation and lifestyle inflation.

Price inflation includes essentials like food, fuel, and healthcare—largely outside individual control. Lifestyle inflation, on the other hand, comes from discretionary upgrades such as bigger homes, premium schooling, travel, and consumption habits.

“In your 30s and early 40s, lifestyle inflation can push your effective inflation rate into double digits,” Avasthi explains. “That’s when retirement numbers start looking exaggerated.”

But this trend doesn’t continue forever.

MUST READ: Are you missing out on these govt pension, insurance schemes costing you under ₹500 a year?

Why the ₹40 crore target

As individuals approach retirement, lifestyle upgrades typically stabilise. Post-retirement, spending is largely limited to essential consumption and healthcare, which tends to moderate overall inflation.

Under more realistic assumptions, the required corpus drops significantly. For the same ₹2 lakh monthly expense today, a controlled lifestyle inflation scenario could result in a retirement requirement in the ₹9–15 crore range.

Experts also point out that geography plays a crucial role. While metro-based retirees may face higher costs, those in smaller cities or with more modest lifestyles may need far less. Some estimates suggest that in non-metro settings, even ₹1.5–2 crore could be sufficient, depending on spending patterns.

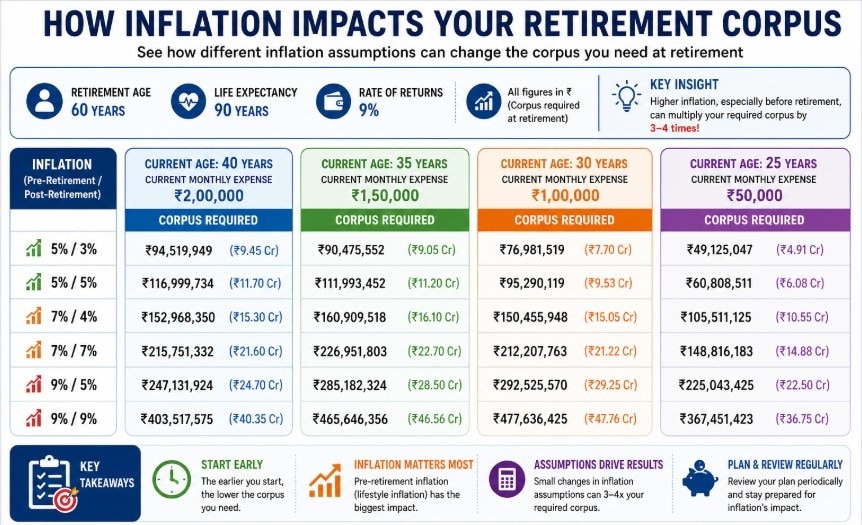

How retirement corpus requirements vary

As per Avasthi, retirement corpus requirements vary significantly based on inflation, age, and current expenses. For instance, a 40-year-old with monthly expenses of ₹2 lakh may need anywhere between about ₹9.4 crore and over ₹40 crore, depending on whether inflation assumptions are moderate (5% pre-retirement, 3% post-retirement) or aggressive (9% for both phases).

A similar pattern is visible across age groups—while starting earlier and having lower expenses reduces the absolute corpus needed, higher inflation can still push requirements sharply upward. The key takeaway is that inflation, particularly pre-retirement lifestyle inflation, is the most critical factor driving retirement needs. Even small changes in inflation assumptions can multiply the required corpus by three to four times, making realistic planning essential.

The role of compounding

Another critical factor often overlooked in headline numbers is compounding. While ₹40 crore sounds daunting, it is a future value. Adjusted for returns during the accumulation phase—typically assumed at around 12%—this translates to roughly ₹4–5 crore in today’s terms.

This reframes the challenge. The focus shifts from chasing a large absolute number to building a disciplined, long-term investment strategy through SIPs and asset allocation.

Moving target

The consensus among experts is clear: retirement planning is deeply personal and dynamic. A fixed corpus target can be misleading if it ignores changes in lifestyle, income, and inflation over time.

Financial planners recommend reviewing retirement goals every few years, tracking actual expenses, and keeping lifestyle inflation in check. Overestimating the corpus can lead to unnecessary stress and overly conservative decisions, while underestimating it can create financial shortfalls later.

MUST READ: NPS charge structure updated: What changes for pension subscribers from July 2026

Your takeaway

The ₹40 crore figure is not a universal requirement — it is a scenario based on aggressive assumptions around inflation and lifestyle. For many investors, especially those who manage lifestyle creep and plan systematically, the actual requirement could be far lower.

Ultimately, retirement planning is not about chasing a single headline number. It is about aligning savings, investments, and lifestyle choices with realistic assumptions — and adjusting along the way as those assumptions evolve.

MUST READ: Need ₹40 crore to retire in India? Here’s the math behind the big number

For the same ₹2 lakh monthly expense today, a controlled lifestyle inflation scenario could result in a retirement requirement in the ₹9–15 crore range.

For the same ₹2 lakh monthly expense today, a controlled lifestyle inflation scenario could result in a retirement requirement in the ₹9–15 crore range. Missed your minimum balance? Banks pocketed ₹26,100 cr in penalties in just 4 years

Missed your minimum balance? Banks pocketed ₹26,100 cr in penalties in just 4 years increase in consolidated net profit to Rs 13,349 crore for the June quarter (Q1 FY27), compared with Rs 12,760 crore in the year-ago period.") Why Tata Sons got ₹28,291 cr from TCS in FY26, down from ₹32,184 cr in FY25

Why Tata Sons got ₹28,291 cr from TCS in FY26, down from ₹32,184 cr in FY25 What a new report says about India's digital banking frauds

What a new report says about India's digital banking frauds ‘Extremely disturbing occurrence ’: MeitY reacts to removal of PM Modi video, seeks explanation from Meta

‘Extremely disturbing occurrence ’: MeitY reacts to removal of PM Modi video, seeks explanation from Meta HUL to further raise prices. Here’s how much

HUL to further raise prices. Here’s how much 7.1 Quake Shakes Southern Japan: Roads Split, Buildings Burn, Hundreds Of Thousands Evacuated

7.1 Quake Shakes Southern Japan: Roads Split, Buildings Burn, Hundreds Of Thousands Evacuated How Mohammad Irfan Went From Street Hawker To India's Most Viral Protest Voice

How Mohammad Irfan Went From Street Hawker To India's Most Viral Protest Voice Congress Vs BJP Clash In Lok Sabha Over Anti-Paper Leak Bill 2026 As Opposition Questions Police

Congress Vs BJP Clash In Lok Sabha Over Anti-Paper Leak Bill 2026 As Opposition Questions Police "Justice Delayed Is Justice Denied": Bansuri Swaraj Hails Anti-Paper Leak Bill Strict Penalties

"Justice Delayed Is Justice Denied": Bansuri Swaraj Hails Anti-Paper Leak Bill Strict Penalties CM Rekha Gupta Approves ‘Delhi Lakshmi Yojana’; Women To Get ₹2,500 Monthly Financial Assistance

CM Rekha Gupta Approves ‘Delhi Lakshmi Yojana’; Women To Get ₹2,500 Monthly Financial Assistance Moschip Technologies, Tamilnad Mercantile Bank shares: Here's what charts indicate

Moschip Technologies, Tamilnad Mercantile Bank shares: Here's what charts indicate Sensex, Nifty end lower as FMCG, energy weigh; IT stocks outperform

Sensex, Nifty end lower as FMCG, energy weigh; IT stocks outperform L&T Q1 results: PAT rises 14% to Rs 4,123 crore; revenue up 7%

L&T Q1 results: PAT rises 14% to Rs 4,123 crore; revenue up 7% Tata Capital Q1 results: PAT jumps 56% YoY to Rs 1,547 crore; AUM rises 22%

Tata Capital Q1 results: PAT jumps 56% YoY to Rs 1,547 crore; AUM rises 22% KPIT Tech, Firstsource: What to do with these two battered IT stocks?

KPIT Tech, Firstsource: What to do with these two battered IT stocks? No browser, no extra app: You can now invest in UTI mutual funds on WhatsApp

No browser, no extra app: You can now invest in UTI mutual funds on WhatsApp Big milestone for India's hydrogen train: Delhi trials next? Here's why it matters to every traveller

Big milestone for India's hydrogen train: Delhi trials next? Here's why it matters to every traveller India's homebuyers are going premium as residential launches hit record high in Q1 2026: Report

India's homebuyers are going premium as residential launches hit record high in Q1 2026: Report Planning an Uttarakhand trip? Prayagraj may soon get a direct train to Kathgodam; here's why it matters

Planning an Uttarakhand trip? Prayagraj may soon get a direct train to Kathgodam; here's why it matters Booking Tatkal tickets from Aug 1? This new Railway rule could make or break your reservation

Booking Tatkal tickets from Aug 1? This new Railway rule could make or break your reservation