Differences between salary disclosed in the ITR and figures reflected in Form 16, employer-filed TDS returns, or AIS records may prompt authorities to seek clarification.

Differences between salary disclosed in the ITR and figures reflected in Form 16, employer-filed TDS returns, or AIS records may prompt authorities to seek clarification. Differences between salary disclosed in the ITR and figures reflected in Form 16, employer-filed TDS returns, or AIS records may prompt authorities to seek clarification.

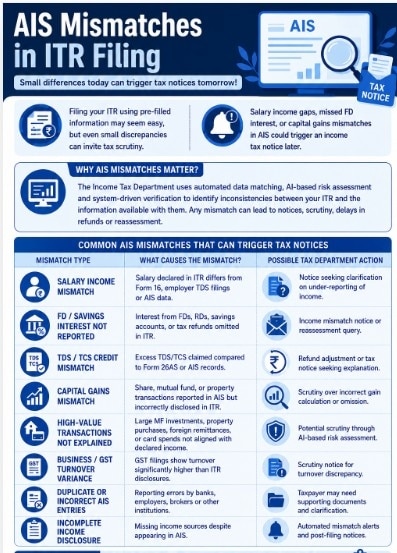

Differences between salary disclosed in the ITR and figures reflected in Form 16, employer-filed TDS returns, or AIS records may prompt authorities to seek clarification.As the Income Tax Return (ITR) filing season for FY 2026–27 gets underway, taxpayers may be tempted to rely heavily on pre-filled return details and quickly complete the filing process. However, tax experts warn that even a seemingly minor mismatch involving salary income, fixed deposit interest, or capital gains could later trigger an income tax notice.

The concern assumes greater significance as the Income Tax Department increasingly uses artificial intelligence-based risk assessment tools, automated data matching systems, and digital verification processes to identify inconsistencies in tax filings. As technology-driven scrutiny becomes more sophisticated, taxpayers are expected to ensure that income reported in their ITR aligns with information already available with the department.

At the center of this process is the Annual Information Statement (AIS), a detailed financial statement that captures a taxpayer's reported transactions and income details. It typically includes salary information, interest income, securities transactions, property dealings, taxes deducted, foreign remittances, and other financial activities.

While AIS has emerged as an important compliance tool, experts caution taxpayers against depending entirely on it while filing returns.

According to CA (Dr.) Suresh Surana, AIS should not be treated as the sole basis for preparing and filing ITRs.

"Taxpayers should not treat the Annual Information Statement (AIS) as the sole basis for filing their Income Tax Return (ITR), as the information reflected therein may at times be incomplete, duplicated, or subject to reporting errors," Surana said.

He added that taxpayers should reconcile AIS details with Form 26AS, Form 16/16A, books of accounts, investment records, bank statements, and other financial documents before submitting returns.

MUST READ: ITR-2 online filing and excel utility enabled for AY 2026-27: Here's what taxpayers should know

The warning comes because AIS is based on data reported by employers, banks, mutual fund houses, stock brokers, registrars and other institutions. Reporting delays, duplication, or errors may sometimes result in discrepancies. If taxpayers fail to identify these differences before filing, automated systems could flag returns for further review.

Salary mismatch

Salary-related mismatches remain among the most common reasons behind tax notices.

Differences between salary disclosed in the ITR and figures reflected in Form 16, employer-filed TDS returns, or AIS records may prompt authorities to seek clarification. Such discrepancies can arise due to bonuses, revised salary structures, employer reporting corrections, or multiple job changes during a financial year.

If salary income appears under-reported compared to records available with the department, taxpayers could receive notices seeking explanations.

MUST READ: Retiring soon? NPS overhaul lets you earn more, withdraw smarter

FD and savings account interest

Interest income is another frequently ignored area.

Income earned from fixed deposits (FDs), recurring deposits (RDs), savings accounts, and even income tax refunds is often reported separately by financial institutions and reflected in AIS.

However, many taxpayers inadvertently omit such earnings while filing returns, particularly when interest amounts are spread across multiple bank accounts.

Partial disclosure or complete omission of interest income can create data mismatches that may later trigger tax department communications.

MUST READ: NPS new rules 2026: PFRDA now allows annuity exit in critical illness cases, eases lock-in norms

Capital gains reporting

Capital gains reporting has become another key area under scrutiny.

Transactions involving shares, mutual funds, property sales, and other capital assets are often independently reported by brokers, registrars, and depositories. As a result, these transactions may already be visible in AIS.

Incorrect capital gains calculations, omission of sale transactions, wrong cost inflation adjustments, or errors in computing taxable gains can trigger scrutiny.

Tax experts note that while transaction values may appear in AIS, taxpayers remain responsible for accurately computing gains and disclosing them in the return.

High-value transactions and TDS mismatches

Apart from salary, FD interest and capital gains, discrepancies involving TDS credits or high-value transactions may also draw attention.

Large mutual fund investments, significant credit card spending, foreign remittances, property purchases, or securities transactions reflected in AIS but not matching declared income sources can create red flags.

Experts say taxpayers should carefully reconcile AIS with supporting financial records before filing returns, as a few additional checks now may help avoid notices and scrutiny later.

'GLP-1 alters...': Kiran Mazumdar-Shaw sounds caution as Nithin Kamath flags weak drug demand

'GLP-1 alters...': Kiran Mazumdar-Shaw sounds caution as Nithin Kamath flags weak drug demand Europe's heatwave far from over: Second heat dome could send temperatures soaring to 46°C in July

Europe's heatwave far from over: Second heat dome could send temperatures soaring to 46°C in July From 175-tonne thrust to future Moon missions: Why ISRO's latest engine test is a game changer

From 175-tonne thrust to future Moon missions: Why ISRO's latest engine test is a game changer  100% tariffs: Trump warns Europe over looming digital services taxes, EU vows swift response

100% tariffs: Trump warns Europe over looming digital services taxes, EU vows swift response June 30 to July 31: ITR scrutiny notice deadline ends June 30; key tax dates to track in July

June 30 to July 31: ITR scrutiny notice deadline ends June 30; key tax dates to track in July Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock Watch

Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock Watch The Man Behind Chandigarh's Cleanliness Mission: Meet Padma Shri Awardee Inderjit Singh Sidhu

The Man Behind Chandigarh's Cleanliness Mission: Meet Padma Shri Awardee Inderjit Singh Sidhu TECH TODAY | Apple Products Suddenly Cost More: What's Behind The ₹1 Lakh Price Jump? FAQ

TECH TODAY | Apple Products Suddenly Cost More: What's Behind The ₹1 Lakh Price Jump? FAQ Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure  JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential

JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet

Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet HDFC Bank, ICICI Bank shares top picks; Axis Bank needs better showing to justify premium, says Kotak

HDFC Bank, ICICI Bank shares top picks; Axis Bank needs better showing to justify premium, says Kotak Rs 33 per share dividend announced; check record date, other details

Rs 33 per share dividend announced; check record date, other details