Tax professionals recommend that taxpayers should carefully review AIS before filing returns, identify mismatches, and either correct their ITR or document valid reasons for differences. Tax professionals recommend that taxpayers should carefully review AIS before filing returns, identify mismatches, and either correct their ITR or document valid reasons for differences.

Tax professionals recommend that taxpayers should carefully review AIS before filing returns, identify mismatches, and either correct their ITR or document valid reasons for differences. Tax professionals recommend that taxpayers should carefully review AIS before filing returns, identify mismatches, and either correct their ITR or document valid reasons for differences.As the Income Tax Department sharpens its data analytics capabilities, a new compliance risk is emerging for taxpayers —a mismatch between the Annual Information Statement (AIS) and Income Tax Returns (ITR). Experts warn that what was once a routine filing exercise has now evolved into a data-matching process, where even minor discrepancies can trigger automated notices.

Chartered accountants highlight that many taxpayers still operate under the outdated assumption that filing an ITR is only about declaring income correctly. However, with AIS becoming a central verification tool, that approach is increasingly risky.

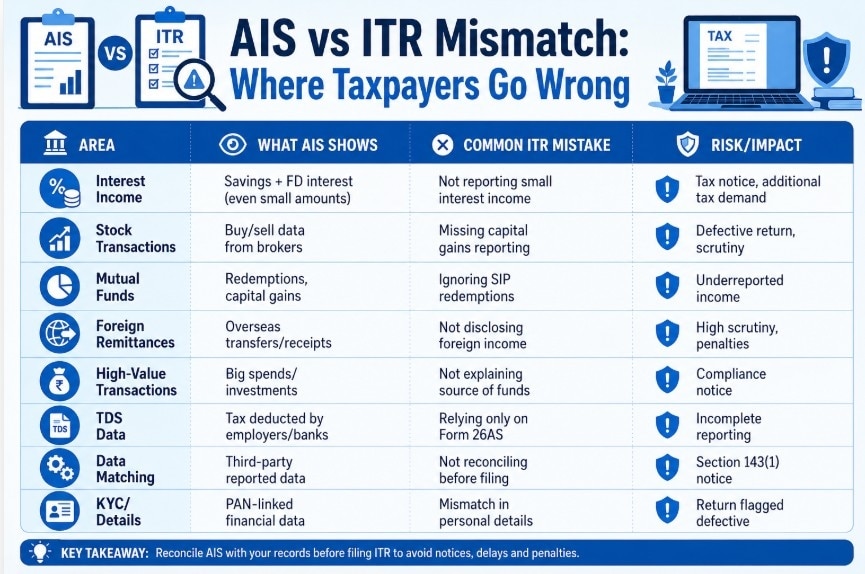

AIS is the key

The AIS now provides a comprehensive snapshot of a taxpayer’s financial activity. It captures not just salary and TDS data, but also interest income from savings accounts and fixed deposits, stock market transactions, mutual fund redemptions, foreign remittances, and even high-value spending patterns.

This expanded scope means the tax department has a near-complete digital trail of financial behaviour. As a result, any inconsistency between AIS data and what is reported in the ITR is quickly flagged by automated systems.

MUST READ: Car lease in salary can cut your tax to zero on ₹20 lakh CTC: Here’s how

What's going wrong

Despite this shift, a large number of taxpayers continue to ignore AIS while filing returns. Many rely solely on Form 26AS, assuming it captures all relevant data. Others fail to reconcile AIS entries with their actual financial records.

“This is where the biggest trap lies,” CA Sonam Chhabra said. “Ignoring AIS or assuming it will match automatically can lead to notices under Section 143(1) or defective return flags.”

Common issues include underreporting of interest income, missing capital gains from equities or mutual funds, and discrepancies in high-value transactions. Even small mismatches can invite scrutiny.

Notices are now automated

The Income Tax Department’s systems are increasingly automated, reducing manual intervention. This means discrepancies are identified faster and at scale.

Taxpayers may receive intimation notices, demands for additional tax, or requests for clarification if mismatches are detected. In some cases, returns may be marked defective, delaying refunds and increasing compliance burden.

Do not ignore

While AIS is not always perfectly accurate—errors or duplication of entries can occur—experts stress that ignoring it is far riskier than addressing discrepancies. Tax professionals recommend that taxpayers carefully review AIS before filing returns, identify mismatches, and either correct their ITR or document valid reasons for differences.

Chhabra said AIS reconciliation is no longer optional; it is a mandatory step in tax filing.

What taxpayers should do

To avoid falling into this trap, taxpayers should adopt a more structured approach:

Reconcile AIS with bank statements, broker reports, and financial records

Report all income streams, including small interest and capital gains

Maintain documentation to justify any differences

Avoid blindly matching AIS—verify accuracy before reporting

Data-Driven compliance

The broader trend is clear: tax compliance in India is moving from self-reporting to data validation. The focus is no longer just on calculating tax liability, but on ensuring that reported data aligns with third-party information available to the tax department. As this transition accelerates, taxpayers who fail to adapt risk increased scrutiny, penalties, and delays.

In FY26, the biggest income tax trap isn’t underreporting alone — it’s failing to match AIS with ITR. In a system driven by data, accuracy and reconciliation are now as important as disclosure.

Income tax return filing gathers pace: Deadline extension unlikely as filings cross 14 mn for AY27

Income tax return filing gathers pace: Deadline extension unlikely as filings cross 14 mn for AY27 Amid E20 debate, Centre evaluating phased rollout of E25 petrol by 2029

Amid E20 debate, Centre evaluating phased rollout of E25 petrol by 2029 DOJ defends dropping criminal charges against Gautam Adani

DOJ defends dropping criminal charges against Gautam Adani BrahMos for Indonesia: PM Modi's Jakarta visit delivers major defence breakthrough

BrahMos for Indonesia: PM Modi's Jakarta visit delivers major defence breakthrough Mumbai rains: 'Allow work from home, otherwise...,' says Maharashtra CM Devendra Fadnavis amid IMD's red alert

Mumbai rains: 'Allow work from home, otherwise...,' says Maharashtra CM Devendra Fadnavis amid IMD's red alert Wrong ITR Filed? Tax Expert Explains How To Revise Your Tax Return Before The Deadline

Wrong ITR Filed? Tax Expert Explains How To Revise Your Tax Return Before The Deadline Before Filing ITR, Tax Expert Gauri Chadha Reveals 4 Documents Every Taxpayer Must Verify To Avoid Notices

Before Filing ITR, Tax Expert Gauri Chadha Reveals 4 Documents Every Taxpayer Must Verify To Avoid Notices The Next Big Winners In The Stock Market | Aparna Shanker's Investment Playbook

The Next Big Winners In The Stock Market | Aparna Shanker's Investment Playbook PM Modi In Jakarta: BrahMos Deal In Focus As India Indonesia Defence Ties Enter Big Phase

PM Modi In Jakarta: BrahMos Deal In Focus As India Indonesia Defence Ties Enter Big Phase India Vs Global Markets: Devina Mehra Explains Rupee Risk, PMS Strategy And Diversification

India Vs Global Markets: Devina Mehra Explains Rupee Risk, PMS Strategy And Diversification Info Edge shares gain 13% on Q1 business updates; breakdown of key businesses

Info Edge shares gain 13% on Q1 business updates; breakdown of key businesses  Trent shares slump over 12% after Q1 FY27 business update; should you wait or buy the dip?

Trent shares slump over 12% after Q1 FY27 business update; should you wait or buy the dip? BEL, BDL, HAL, SOIL Industries: Target prices for 4 defence stocks

BEL, BDL, HAL, SOIL Industries: Target prices for 4 defence stocks HZL share price: Vedanta group stock down 15% in 6 months; should you buy Hindustan Zinc?

HZL share price: Vedanta group stock down 15% in 6 months; should you buy Hindustan Zinc? Varun Beverages gives up Rs 500 mark, clocks negative returns for 2026; price targets & more

Varun Beverages gives up Rs 500 mark, clocks negative returns for 2026; price targets & more