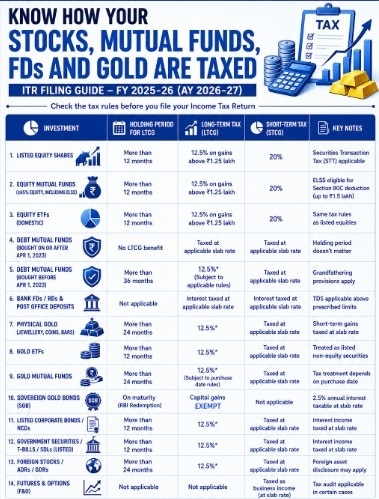

Financial planners say investors should focus on post-tax returns, not just headline yields, as taxes, exemptions and TDS can significantly affect actual gains.

Financial planners say investors should focus on post-tax returns, not just headline yields, as taxes, exemptions and TDS can significantly affect actual gains.Choosing the right investment is no longer just about earning higher returns. Taxation has become an equally important factor, as different financial products—from stocks and mutual funds to fixed deposits, gold and government securities—are subject to different tax rules depending on the holding period and nature of income.

A tax reckoner for FY2025-26 (Assessment Year 2026-27) outlines the latest tax treatment across popular investment options, helping investors understand how capital gains and income from various asset classes are taxed.

and Gujarat (₹6,352.38 crore)") ₹8,862 crore in tolls! This state emerged as India's biggest highway toll revenue generator

₹8,862 crore in tolls! This state emerged as India's biggest highway toll revenue generator Could India witness a Korea-style market meltdown? Nithin Kamath explains the biggest risk

Could India witness a Korea-style market meltdown? Nithin Kamath explains the biggest risk How Indian investment overseas is gathering momentum

How Indian investment overseas is gathering momentum Semicon 2.0, space, hydrogen trains: How manufacturing push is gaining pace, shows July's economic review

Semicon 2.0, space, hydrogen trains: How manufacturing push is gaining pace, shows July's economic review To stay ahead, Indian manufacturers are embracing AI

To stay ahead, Indian manufacturers are embracing AI Why Ajay Bagga Is Bullish On EMS Stocks | PLI, Semiconductors & India's Growth Story

Why Ajay Bagga Is Bullish On EMS Stocks | PLI, Semiconductors & India's Growth Story Why Term Insurance Is Better For Family Protection Than Traditional Life Insurance

Why Term Insurance Is Better For Family Protection Than Traditional Life Insurance "RSS Controls Education, Dharmendra Pradhan Is Just A Symbol!": Rahul Gandhi’s Scathing Attack

"RSS Controls Education, Dharmendra Pradhan Is Just A Symbol!": Rahul Gandhi’s Scathing Attack KOSPI Crash Explained | ₹152 Lakh Crore Gone, AI Stocks Under Massive Pressure

KOSPI Crash Explained | ₹152 Lakh Crore Gone, AI Stocks Under Massive Pressure PSU Stocks Outlook: Can Defence, Power & Industrial PSUs Deliver Strong Returns Ahead?

PSU Stocks Outlook: Can Defence, Power & Industrial PSUs Deliver Strong Returns Ahead? Waaree, Kalyan Jewellers, Welspun Corp: Stocks to trade— Price targets, stop loss & more

Waaree, Kalyan Jewellers, Welspun Corp: Stocks to trade— Price targets, stop loss & more Top stocks in news: Indo-MIM, Eicher Motors, Xtranet, PNB, Dabur, MTAR, Waaree, Lohia Corp

Top stocks in news: Indo-MIM, Eicher Motors, Xtranet, PNB, Dabur, MTAR, Waaree, Lohia Corp Indo-MIM, Lohia Corp, Xtranet Tech IPO listings today: Latest GMP, expectations & moreCould India witness a Korea-style market meltdown? Nithin Kamath explains the biggest risk

Indo-MIM, Lohia Corp, Xtranet Tech IPO listings today: Latest GMP, expectations & moreCould India witness a Korea-style market meltdown? Nithin Kamath explains the biggest risk Dabur India Q1 results: Profit up 15% at Rs 591 crore YoY; revenue climbs 11%

Dabur India Q1 results: Profit up 15% at Rs 591 crore YoY; revenue climbs 11% Iran wants to bulk up its defence amid war with the US, Israel. China lends a helping hand

Iran wants to bulk up its defence amid war with the US, Israel. China lends a helping hand Petrol, diesel prices today, July 30: Check latest rates in Delhi, Mumbai, Chennai, Kolkata & moreWhy Ajay Bagga Is Bullish On EMS Stocks | PLI, Semiconductors & India's Growth Story

Petrol, diesel prices today, July 30: Check latest rates in Delhi, Mumbai, Chennai, Kolkata & moreWhy Ajay Bagga Is Bullish On EMS Stocks | PLI, Semiconductors & India's Growth Story These two countries consume 70% of the world’s coal…and it’s who you think it isWaaree, Kalyan Jewellers, Welspun Corp: Stocks to trade— Price targets, stop loss & more

These two countries consume 70% of the world’s coal…and it’s who you think it isWaaree, Kalyan Jewellers, Welspun Corp: Stocks to trade— Price targets, stop loss & more