TDS on salary is governed by Section 192 of the Income Tax Act. Employers are required to deduct tax from salaries and deposit it with the government within prescribed timelines.

TDS on salary is governed by Section 192 of the Income Tax Act. Employers are required to deduct tax from salaries and deposit it with the government within prescribed timelines.A Mumbai bench of the Income Tax Appellate Tribunal (ITAT) has delivered a significant ruling for salaried taxpayers, holding that employees cannot be asked to pay tax a second time merely because their employer deducted Tax Deducted at Source (TDS) but failed to deposit it with the government.

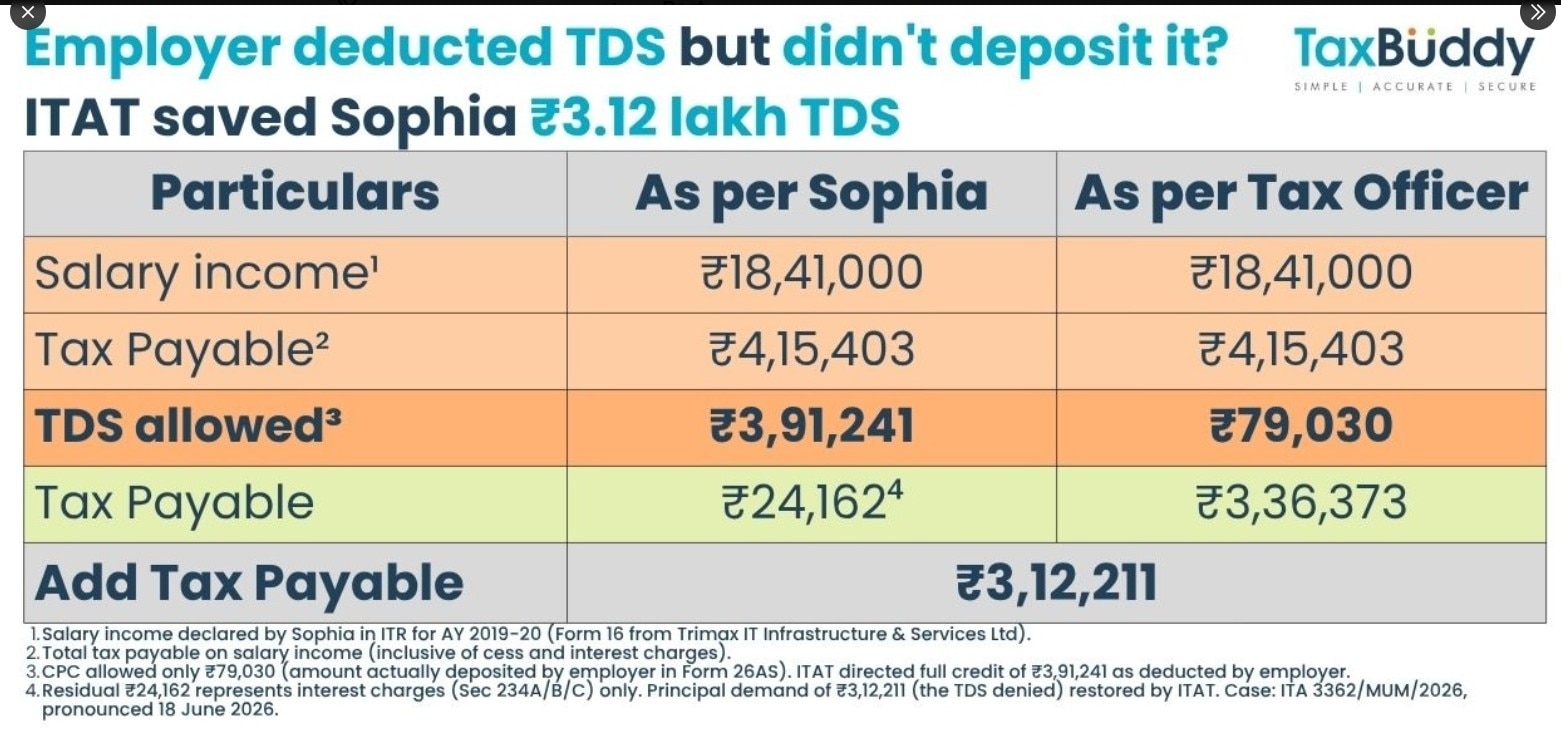

The tribunal granted full credit of ₹3.91 lakh in TDS to an employee and quashed a tax demand of over ₹3.12 lakh, reiterating that the liability to deposit deducted tax rests with the employer, not the employee.

How the dispute arose

The case involved Sophia, a salaried employee whose employer deducted ₹3.91 lakh as TDS from her annual salary of ₹18.41 lakh. Her total tax liability for the assessment year stood at ₹4.15 lakh.

However, the employer deposited only ₹79,030 with the Income Tax Department. Since only the deposited amount appeared in Form 26AS, the Centralised Processing Centre (CPC) allowed credit for ₹79,030 instead of the full TDS deducted from her salary.

This resulted in a fresh tax demand of ₹3.36 lakh, comprising the denied TDS credit of ₹3.12 lakh along with applicable interest.

MUST READ: No Section 80C, no HRA? Here's how salaried employees can save tax under New Tax Regime

Legal battle reached ITAT

Sophia initially sought rectification from the Income Tax Department, but her application was rejected. Her appeal before the Commissioner of Income Tax (Appeals) was also dismissed because of a delay in filing.

She subsequently approached the ITAT Mumbai and personally represented her case. Before the tribunal, she submitted Form 16 issued by her employer, salary slips and bank statements showing that her salary had been credited only after deducting TDS.

The tribunal condoned the delay, observing that she had been continuously pursuing remedies before the tax authorities.

Why the tribunal ruled in her favour

The ITAT relied on Section 205 of the Income Tax Act, which states that where tax is deductible at source, the assessee cannot be called upon to pay that tax again to the extent it has already been deducted.

It also referred to CBDT Instruction No. 275 dated June 1, 2015, which instructs tax officers not to recover tax from employees where the employer has deducted TDS but failed to deposit it. Instead, the recovery should be initiated against the defaulting employer.

The tribunal further relied on judicial precedents, including the Gujarat High Court's ruling in Gayatri Snehal Rao and Supreme Court decisions affirming the same legal principle.

MUST READ: Switched jobs during FY26? Here's how to file ITR with multiple Form 16s and avoid tax notices

Accordingly, ITAT directed the tax department to grant Sophia full TDS credit of ₹3.91 lakh, effectively wiping out the principal tax demand.

What salaried employees should do

TDS on salary is governed by Section 192 of the Income Tax Act. Employers are required to deduct tax from salaries and deposit it with the government within prescribed timelines.

Employees should not assume that deduction from salary alone is sufficient. Experts advise checking Form 26AS and the Annual Information Statement (AIS) regularly to ensure the deducted TDS has actually been deposited.

If the TDS shown in Form 16 does not match Form 26AS, taxpayers should immediately approach their employer for correction and preserve all supporting documents, including salary slips, bank statements and Form 16.

MUST READ: ITR due dates, revised returns and audit penalties: 3 big tax changes from AY 2026-27

If a tax demand is nevertheless raised, employees can seek rectification and, if required, file an appeal while relying on Section 205, CBDT Instruction No. 275 and the latest ITAT ruling. The judgment reinforces an important taxpayer safeguard: an employer's failure to deposit deducted TDS cannot ordinarily become the employee's tax burden.

US Justice Department drops Adani bribery case after intensive legal push

US Justice Department drops Adani bribery case after intensive legal push YES Bank shares fall 4% after Q1 results; brokerages raise target prices by up to 30%

YES Bank shares fall 4% after Q1 results; brokerages raise target prices by up to 30% Paytm bonus shares, Q1 results: 50% jump in profit? Earnings preview; 4 things to watch

Paytm bonus shares, Q1 results: 50% jump in profit? Earnings preview; 4 things to watch Delhi Police imposes 'section 163' ahead of CJP’s 'Chalo Sansad' parliament march

Delhi Police imposes 'section 163' ahead of CJP’s 'Chalo Sansad' parliament march ") Naveen Jindal Group in talks for proposed nuclear projects, in discussion with US, French companies

Naveen Jindal Group in talks for proposed nuclear projects, in discussion with US, French companies U.S.-Iran War’s 3 Phases Explained: From Khamenei’s Killing To Battle For Strait Of Hormuz

U.S.-Iran War’s 3 Phases Explained: From Khamenei’s Killing To Battle For Strait Of Hormuz China’s Helium Export Ban Triggers Global Tech Alarm As Hormuz Crisis Chokes Critical Supply

China’s Helium Export Ban Triggers Global Tech Alarm As Hormuz Crisis Chokes Critical Supply CEAT Stock Impact: Why The Company Took A ₹50 Crore Forex Loss | CFO Breaks It Down

CEAT Stock Impact: Why The Company Took A ₹50 Crore Forex Loss | CFO Breaks It Down Caliber Mining IPO Opens: Should You Subscribe? Price Band, GMP & Key Risks Explained

Caliber Mining IPO Opens: Should You Subscribe? Price Band, GMP & Key Risks Explained Trump Threatens Iran’s “Pickaxe Mountain”: Why This Nuclear-Linked Bunker Is Hard To HitYES Bank shares fall 4% after Q1 results; brokerages raise target prices by up to 30%Paytm bonus shares, Q1 results: 50% jump in profit? Earnings preview; 4 things to watch

Trump Threatens Iran’s “Pickaxe Mountain”: Why This Nuclear-Linked Bunker Is Hard To HitYES Bank shares fall 4% after Q1 results; brokerages raise target prices by up to 30%Paytm bonus shares, Q1 results: 50% jump in profit? Earnings preview; 4 things to watch Va Tech Wabag shares climb 5% on fresh order win; what consensus target hints at

Va Tech Wabag shares climb 5% on fresh order win; what consensus target hints at Indo-MIM IPO opens on July 23; check all key details including price band, lot size & more

Indo-MIM IPO opens on July 23; check all key details including price band, lot size & more Axis Bank shares: Why this stock fell 6% despite 23% jump in Q1 profit? Targets by foreign brokers

Axis Bank shares: Why this stock fell 6% despite 23% jump in Q1 profit? Targets by foreign brokers