The Income Tax Department has revised return forms to ensure clearer reporting under Schedule OS (Income from Other Sources), reducing ambiguity and improving compliance.The Income Tax Department has revised return forms to ensure clearer reporting under Schedule OS (Income from Other Sources), reducing ambiguity and improving compliance.

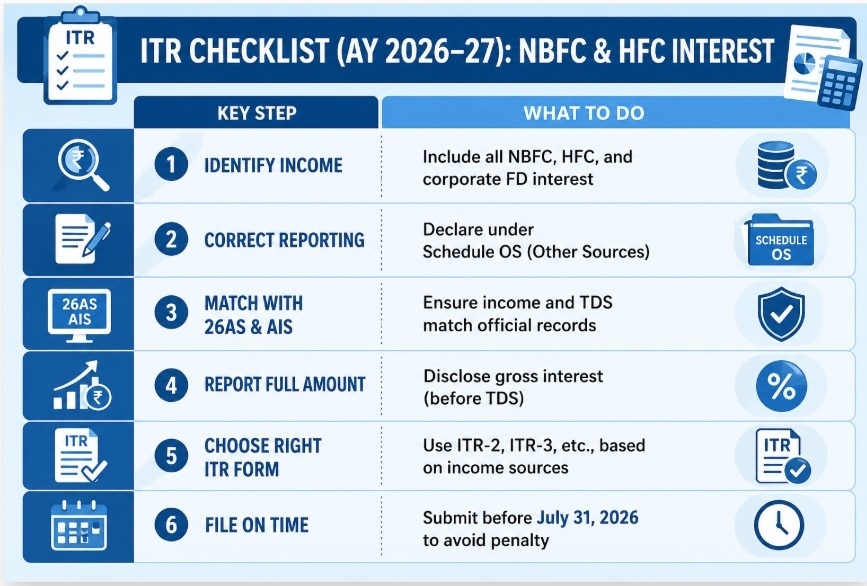

The Income Tax Department has revised return forms to ensure clearer reporting under Schedule OS (Income from Other Sources), reducing ambiguity and improving compliance.The Income Tax Department has revised return forms to ensure clearer reporting under Schedule OS (Income from Other Sources), reducing ambiguity and improving compliance.Taxpayers earning interest income from Non-Banking Financial Companies (NBFCs), Housing Finance Companies (HFCs), and corporate fixed deposits will face tighter disclosure requirements while filing Income Tax Returns (ITR) for Assessment Year (AY) 2026–27. The Income Tax Department has revised return forms to ensure clearer reporting under Schedule OS (Income from Other Sources), reducing ambiguity and improving compliance.

Clearer categorisation

Under the updated ITR structure, interest earned from companies, NBFCs, and HFCs must now be explicitly reported under Schedule OS. Earlier, such income was not distinctly categorised, often leading to confusion among taxpayers while classifying it under “other income.” The revised format removes this ambiguity by clearly identifying these income streams.

Siddharth Maurya, Founder and Managing Director of Vibhvangal Anukulakara Private Limited, said taxpayers must now pay closer attention while reporting such income. “Taxpayers who earn fixed deposit interest from NBFCs and HFCs must report this income through Schedule OS under the new ITR filing requirements for AY 2026–27. Earlier, taxpayers reported FD interest as a combined figure, but this new requirement improves transparency and allows the Income Tax Department to match reported income with TDS data in Form 26AS and the Annual Information Statement (AIS),” he said.

What falls under Schedule OS

Schedule OS includes income that does not fall under salary, house property, capital gains, or business income. This covers interest from savings accounts, bank and post office deposits, dividend income, interest on tax refunds, family pension, and now explicitly, interest from NBFCs, HFCs, and corporate instruments such as debentures.

Maurya added that this change increases reporting precision. “Investors must accurately report interest earned from institutions such as Bajaj Finance or LIC Housing Finance. Any missing or incorrectly disclosed income could trigger scrutiny and delay refund processing,” he said.

No change in taxation, only reporting

Importantly, there is no change in how such income is taxed. Interest earned from NBFC or HFC deposits continues to be added to total income and taxed as per the individual’s applicable slab rate. A taxpayer in the 30% bracket will continue to pay tax at 30% on this income, similar to bank fixed deposits.

The revision is focused entirely on improving reporting clarity rather than altering tax liability.

MUST READ: ₹200 per meal rule explained: How you can maximise tax savings under new, old tax regimes

Reconciliation is now critical

With stricter disclosure norms, taxpayers must ensure that income declared in ITR matches details available in Form 26AS and AIS. TDS deducted on such interest will already be reflected in these statements and must be reconciled carefully before filing.

“This change reinforces the government’s push toward tighter compliance, making it essential for taxpayers to reconcile all FD interest entries before filing returns,” Maurya noted.

Deadline and compliance impact

The due date for filing ITR for AY 2026–27 is July 31, 2026 for non-audit taxpayers. Missing the deadline can attract a penalty of up to ₹5,000 under Section 234F, along with applicable interest under Sections 234A, 234B, and 234C.

New ITR framework

The revised ITR framework marks a shift toward greater transparency and data matching in tax reporting. While the tax outgo remains unchanged, accurate disclosure has become critical. For investors in NBFC and HFC deposits, precise reporting under Schedule OS will be key to avoiding notices and ensuring smooth return processing.

BPCL, HPCL and IOC: OMCs still not out of the woods? Share price targets

BPCL, HPCL and IOC: OMCs still not out of the woods? Share price targets Now, Trump is talking of Hormuz tolls if US-Iran deal collapses. What's his proposal?

Now, Trump is talking of Hormuz tolls if US-Iran deal collapses. What's his proposal? Transfers, promotions to go digital? Centre plans major HR overhaul at PSU banks

Transfers, promotions to go digital? Centre plans major HR overhaul at PSU banks") Jammers, 1.38 lakh CCTV cameras: How NTA is gearing up for big NEET re-test today

Jammers, 1.38 lakh CCTV cameras: How NTA is gearing up for big NEET re-test today Explained: Why Rajasthan is getting more rain than Maharashtra this June

Explained: Why Rajasthan is getting more rain than Maharashtra this June Why Do AI Data Centres Use So Much Water ? | Explained

Why Do AI Data Centres Use So Much Water ? | Explained Why Is India’s Cruise Market Just Getting Started?

Why Is India’s Cruise Market Just Getting Started? Versailles Peace Deal Explained: How U.S.-Iran War Moved From Missiles To MoU

Versailles Peace Deal Explained: How U.S.-Iran War Moved From Missiles To MoU Power Bags ₹5,000 Crore Karnataka Project, Unveils Big Mumbai Expansion Plan

Power Bags ₹5,000 Crore Karnataka Project, Unveils Big Mumbai Expansion Plan U.S.-Iran War Explained: From Operation Epic Fury To Strait Of Hormuz Crisis And Peace Deal

U.S.-Iran War Explained: From Operation Epic Fury To Strait Of Hormuz Crisis And Peace Deal Defence stocks to buy: Brokerage firms go bullish on this multibagger for strong gainsBPCL, HPCL and IOC: OMCs still not out of the woods? Share price targets

Defence stocks to buy: Brokerage firms go bullish on this multibagger for strong gainsBPCL, HPCL and IOC: OMCs still not out of the woods? Share price targets BSE, Hyundai, Pine Labs, Ather & others: Top 12 fresh brokerage picks with upto 64% upside

BSE, Hyundai, Pine Labs, Ather & others: Top 12 fresh brokerage picks with upto 64% upside Are mid- and small-caps poised to lead the next leg of the market rally? Experts explain why

Are mid- and small-caps poised to lead the next leg of the market rally? Experts explain why India's average digital investor holds ₹10 lakh, adds ₹3 lakh a year: Report

India's average digital investor holds ₹10 lakh, adds ₹3 lakh a year: Report