Home loans continue to offer the most significant tax benefits, but largely under the old tax regime.Home loans continue to offer the most significant tax benefits, but largely under the old tax regime.

Home loans continue to offer the most significant tax benefits, but largely under the old tax regime.Home loans continue to offer the most significant tax benefits, but largely under the old tax regime.Tax deductions: Not all loans offer tax benefits; check which all can allow you exemptions under Old Tax Regime. Deductions depend on the loan purpose and the tax regime you choose. A loan is a form of credit where a specific amount of money is given to someone with the agreement that it will be paid back later. In many cases, the lender also adds interest or finance charges to the principal value, which the borrower must repay in addition to the principal balance. Loans may be for a specific, one-time amount, or they may be available as an open-ended line of credit up to a specified limit. Loans come in many different forms, including secured, unsecured, commercial, and personal loans.

Tax advisory platform Tax Buddy decodes how deductions differ across home, education, personal and vehicle loans—and where taxpayers often get caught off guard.

Home loan

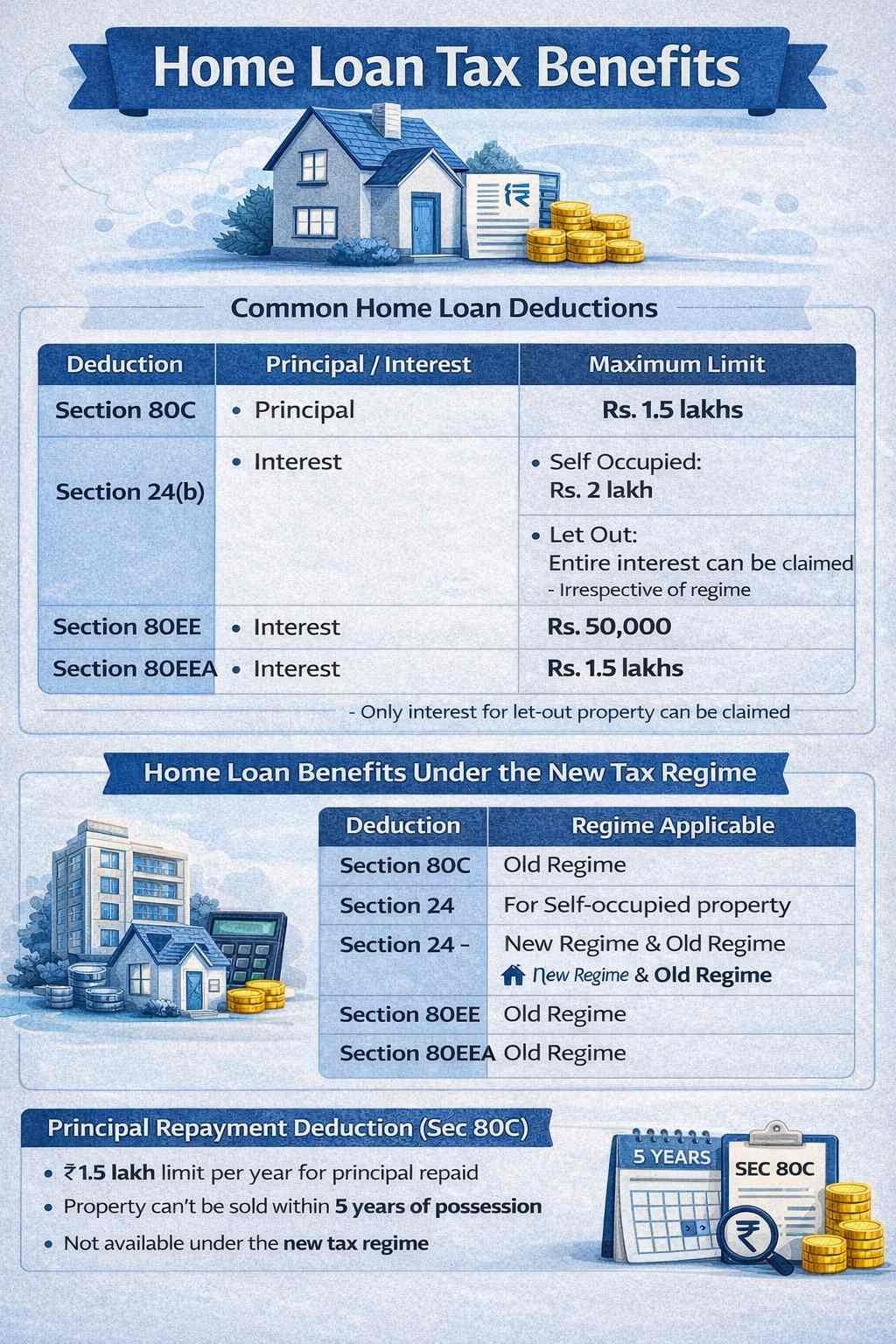

Home loans continue to offer the most significant tax benefits, but largely under the old tax regime. For self-occupied properties, interest paid on a home loan qualifies for a deduction of up to Rs 2 lakh per year under Section 24(b) in the old regime. This benefit is not available under the new tax regime. For let-out properties, there is no upper limit on interest deduction under the old regime, though loss set-off against salary income is capped at Rs 2 lakh. Under the new regime, interest can only be set off against rental income, not salary.

Principal repayment benefits under Section 80C, up to Rs 1.5 lakh annually, are also available only in the old regime. Additionally, pre-construction interest can be claimed in five equal instalments after possession under the old regime, but not for self-occupied homes under the new regime. Joint home loan borrowers can split deductions in proportion to ownership, allowing each co-owner to claim up to Rs 2 lakh on interest and Rs 1.5 lakh on principal under the old regime.

Home loan tax benefits

Home loan tax benefits allow borrowers to reduce their taxable income by claiming deductions on both principal repayment and interest paid, subject to specified limits and conditions. Under the old tax regime, the principal component of home loan EMIs qualifies for deduction under Section 80C, capped at Rs 1.5 lakh annually. This benefit is available only if the property is retained for at least five years from possession; an early sale results in a reversal of earlier claims. Stamp duty and registration charges can also be claimed within the same Rs 1.5 lakh limit.

Interest paid on home loans is eligible for deduction under Section 24(b). For self-occupied properties, the maximum deduction is Rs 2 lakh per year, while for let-out properties, the entire interest paid can be claimed. Additional interest benefits are available under Section 80EE (up to Rs 50,000) and Section 80EEA (up to Rs 1.5 lakh), subject to eligibility conditions.

Under the new tax regime (Section 115BAC), most home loan deductions are withdrawn. Only interest on loans for let-out properties can be claimed, making the choice of tax regime crucial for homeowners.

Education loans

Education loans remain one of the few areas where tax benefits are consistent across both regimes. Interest paid on an education loan qualifies for deduction under Section 80E with no upper limit, for up to eight years. The benefit applies to loans taken for self, spouse or children, including overseas education. However, there is no deduction for principal repayment under either regime.

Personal loans

Personal loans are not tax-deductible by default. Their tax treatment depends entirely on usage. If the loan is used for business purposes or education, interest may qualify for deduction under the relevant sections in both regimes. However, interest on personal loans used for self-occupied house purchase is not allowed under the new regime, and loans used for lifestyle or consumption purposes do not qualify for deductions under either regime.

Vehicle loans

Vehicle loans offer no tax benefits for personal use under either regime. However, when used for business or professional purposes, interest and depreciation can be claimed as expenses, proportionate to business use, regardless of the chosen tax regime.

The broader takeaway is that tax benefits depend more on the purpose of the loan than the loan itself. Deductions apply only to interest, not EMIs, and proper documentation—such as ownership proof and usage evidence—is critical. Incorrect classification or usage can result in deductions being disallowed during scrutiny, making regime selection and loan planning crucial for taxpayers.

Auto, wines, apples: India-EU FTA gives a gradual tariff reduction with import quota

Auto, wines, apples: India-EU FTA gives a gradual tariff reduction with import quota Ajit Pawar plane crash: Visibility, bird hit or technical glitch? Aviation expert breaks down tragic incident

Ajit Pawar plane crash: Visibility, bird hit or technical glitch? Aviation expert breaks down tragic incident US govt on brink of partial shutdown? Here's what we know so far

US govt on brink of partial shutdown? Here's what we know so far India-US BTA: Discussions continue in a cordial atmosphere

India-US BTA: Discussions continue in a cordial atmosphere Economic Survey 2025-26: Growth outlook, inflation, capex, jobs -- what to expect amid global headwinds

Economic Survey 2025-26: Growth outlook, inflation, capex, jobs -- what to expect amid global headwinds India–EU FTA Sealed: Ireland’s Envoy Says Deal Will Cut Tariffs, Boost Trade And Benefit Consumers

India–EU FTA Sealed: Ireland’s Envoy Says Deal Will Cut Tariffs, Boost Trade And Benefit Consumers ONGC, Reliance Ink Offshore Resource-Sharing Pact; Oil & Gas Stocks Surge

ONGC, Reliance Ink Offshore Resource-Sharing Pact; Oil & Gas Stocks Surge Four-Lane Flyover Turns Two-Lane Suddenly, Sparks Safety Fears In Mira-Bhayander

Four-Lane Flyover Turns Two-Lane Suddenly, Sparks Safety Fears In Mira-Bhayander Defence Stocks Rally Ahead Of Budget; BEL, Data Patterns, BEML Lead Surge

Defence Stocks Rally Ahead Of Budget; BEL, Data Patterns, BEML Lead Surge EXCLUSIVE: EU VP Kaja Kallas On India-EU Deal, US Tariffs, Russia War And Global Uncertainty

EXCLUSIVE: EU VP Kaja Kallas On India-EU Deal, US Tariffs, Russia War And Global Uncertainty Budget 2026: No change expected in capital gains tax; capex push, fiscal discipline to anchor markets, says MOFSL's Nandish Shah

Budget 2026: No change expected in capital gains tax; capex push, fiscal discipline to anchor markets, says MOFSL's Nandish Shah Budget 2026, metals & mining stocks: Why Tata Steel, Hindustan Copper, Vedanta & Hind Zinc are in focus

Budget 2026, metals & mining stocks: Why Tata Steel, Hindustan Copper, Vedanta & Hind Zinc are in focus Budget 2026 stock pick: Buy NTPC for up to 15% upside, says Choice’s Sumeet Bagadia

Budget 2026 stock pick: Buy NTPC for up to 15% upside, says Choice’s Sumeet Bagadia  How much have Adani group stocks corrected from their 52-week highs?

How much have Adani group stocks corrected from their 52-week highs? BEL shares hit record high after Q3 results; PAT rises 21%, revenue up 24%

BEL shares hit record high after Q3 results; PAT rises 21%, revenue up 24%