India’s LNG infrastructure faces uneven Hormuz exposure, with Petronet LNG’s Dahej terminal most vulnerable at ~76%.

India’s LNG infrastructure faces uneven Hormuz exposure, with Petronet LNG’s Dahej terminal most vulnerable at ~76%. India’s LNG infrastructure faces uneven Hormuz exposure, with Petronet LNG’s Dahej terminal most vulnerable at ~76%.

India’s LNG infrastructure faces uneven Hormuz exposure, with Petronet LNG’s Dahej terminal most vulnerable at ~76%.India’s natural gas supply chain faces growing vulnerability due to its heavy reliance on liquefied natural gas (LNG) shipments routed through the Strait of Hormuz, a key global energy chokepoint. Multiple research reports by Elara Securities, Crisil Ratings and CareEdge Global highlight that any prolonged disruption in the region could ripple across India’s LNG infrastructure, pipeline networks and energy-intensive industries.

According to a recent note by Elara Securities titled “LNG: Steering through the Hormuz bottleneck”, nearly 69 percent of India’s LNG imports, about 17.5 million tonnes or 63 million metric standard cubic metres per day, originate from Qatar, the UAE and Oman, meaning most shipments transit through or near the Strait of Hormuz. Even after accounting for GAIL’s LNG swap arrangements with the US, the effective exposure of India’s gas system remains around 66 percent, underscoring the structural dependence on Middle Eastern supply routes.

The report notes that disruptions could affect the gas ecosystem sequentially—first impacting LNG terminal utilisation, then pipeline transmission volumes, and eventually industrial margins for downstream users.

Import terminals face high exposure

India’s LNG import infrastructure shows varying levels of exposure to Hormuz-linked supply routes. The Dahej terminal in Gujarat, operated by Petronet LNG, handles the country’s largest LNG import volumes and has roughly 76 percent exposure to supplies passing through the strait, making it one of the most vulnerable assets in the network.

Other terminals also carry elevated exposure. Mundra terminal has about 88 percent dependency, while Dhamra stands at roughly 65 percent and Ennore around 62 percent, according to the Elara report. In contrast, Hazira terminal has only about 25 percent exposure due to diversified sourcing from regions such as the US, Russia and Australia.

Smaller terminals like Kochi and Chhara depend entirely on Middle Eastern LNG, although their absolute volumes remain smaller compared with Dahej.

Companies face uneven risk

Among listed gas companies, Petronet LNG and Gujarat State Petronet Ltd (GSPL) appear most exposed. Petronet LNG has roughly 77 percent dependency on Hormuz-linked cargo, while GSPL’s transmission volumes are estimated to have around 62 percent exposure to LNG routed through the strait.

The report notes that Petronet LNG has already issued force majeure notices to companies including GAIL, Indian Oil Corporation and BPCL, citing shipping disruptions affecting LNG cargo loadings at Qatar’s Ras Laffan facility.

Downstream distributors could also face pressure. Gujarat Gas, for instance, derives about 73 percent of its supply from LNG, much of which caters to the price-sensitive Morbi ceramics cluster. Rising LNG prices could make gas less competitive against alternative fuels such as propane, potentially affecting industrial demand.

Global reports flag supply shock risks

Other research agencies also warn that geopolitical disruptions could tighten LNG supply chains.

A Crisil Ratings credit alert titled “Middle East uncertainties: Direct trade, LNG-dependent and crude-linked sectors could bear brunt of prolonged disruption” highlights that India imports roughly half of its LNG requirement, with 50–60 percent of these shipments routed through the Strait of Hormuz. Any prolonged disruption could affect global LNG availability and drive prices sharply higher.

Crisil Middle East uncertainties

Crisil notes that Asian spot LNG prices have already surged from around $10 per MMBtu to $24–25 per MMBtu, raising the risk of higher inflation, a widening current account deficit and margin pressure for energy-intensive sectors such as fertilisers and ceramics.

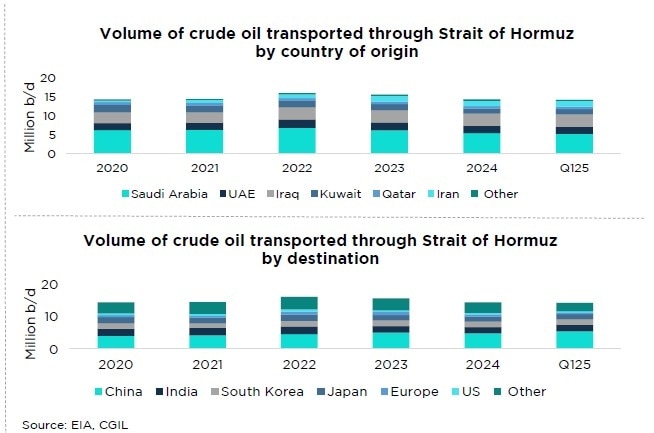

Similarly, the CareEdge Global report “Global Economy Update: All Eyes on the Middle East” emphasises the strategic importance of the waterway, noting that the Strait of Hormuz accounts for about one-fifth of global oil and LNG supply. The report adds that Asia is the most exposed region, with around 83 percent of LNG passing through the strait destined for Asian markets, including India, China, Japan and South Korea.

Defensive players offer some stability

Despite the risks, not all players in India’s gas sector face the same level of exposure. GAIL’s marketing segment remains relatively resilient, with only around 16 percent dependency on LNG sourced via the Strait of Hormuz due to diversified contracts from the US, Russia and Australia.

City gas distributors such as Indraprastha Gas (IGL) and Mahanagar Gas (MGL) are also considered relatively defensive, as a large share of their supply comes from domestic gas allocated to priority sectors like CNG and household cooking fuel.

Together, the reports suggest that while India has significantly expanded its LNG infrastructure in recent years, the country’s continued reliance on Middle Eastern supply routes leaves its gas ecosystem vulnerable to geopolitical shocks in one of the world’s most critical energy corridors.

Centre to launch new series WPI, producer price indices on June 15

Centre to launch new series WPI, producer price indices on June 15 Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation

Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation Mother Dairy expects 5% growth in FY27; eyes expansion beyond Delhi-NCR

Mother Dairy expects 5% growth in FY27; eyes expansion beyond Delhi-NCR, Wipro and Tech Mahindra have seen renewed buying interest.") IT stocks stage a comeback: Five factors supporting the strong upmove

IT stocks stage a comeback: Five factors supporting the strong upmove ‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’

‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’ From Global Uncertainty To India's Opportunity: The Big Economic Outlook

From Global Uncertainty To India's Opportunity: The Big Economic Outlook Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services

Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early?

SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early? Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today

Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom

Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom Tata Tech, Bharti Airtel, PFC, BLS International shares: Should you enter at current levels?Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation

Tata Tech, Bharti Airtel, PFC, BLS International shares: Should you enter at current levels?Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove

Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?

CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?