Among midcap firms, Equirus forecasts robust organic quarter-on-quarter sales growth for Persistent Systems Ltd, Coforge Ltd, Mphasis Ltd and KPIT Technologies.

Among midcap firms, Equirus forecasts robust organic quarter-on-quarter sales growth for Persistent Systems Ltd, Coforge Ltd, Mphasis Ltd and KPIT Technologies.According to the brokerage firms, the Indian IT sector is projected to report a quarter of soft sales growth due to volatile macroeconomic conditions, rising geopolitical tensions, and seasonal softness. Demand for AI-driven scale-up among enterprise clients continues, with funding largely coming from cost savings through outsourcing and vendor consolidation.

Equirus Securities expects the top six large IT companies to report quarter-on-quarter constant currency US dollar sales changes ranging from a dip of 1.9 per cent to growth of 1.6 per cent in the fourth quarter. Companies such as LTIMindTree Ltd and Tata Consultancy Services Ltd (TCS) are anticipated to perform near the upper end, while Infosys Ltd and HCL Technologies Ltd may experience seasonal softness.

Among midcap firms, Equirus forecasts robust organic quarter-on-quarter sales growth for Persistent Systems Ltd, Coforge Ltd, Mphasis Ltd and KPIT Technologies. Currency tailwinds, with an average depreciation of around 3 per cent of the Indian rupee, easing supply-side issues and cost optimization efforts, are expected to support earnings before interest and tax margins.

Indian IT services companies are expected to report resilient results in Q4FY26E, supported by the reversal of furloughs, stable deal ramp-ups, and a robust AI-driven project pipeline, according to Choice Institutional Equities. Despite macroeconomic challenges and concerns over generative AI disruptions, the sector is positioned for steady performance.

Choice Institutional Equities highlights that a 2.5 per cent quarter-on-quarter (QoQ) depreciation of the Indian rupee against the US dollar will provide a meaningful translation benefit to reported revenues and margins. Cross-currency movements are also anticipated to contribute up to a 0.5% sequential uplift in dollar revenues.

Despite recent corrections in sector valuations and high free cash flow yields, Equirus Securities notes that valuations may remain cautious in the near term. Concerns over geopolitical risks, including the Iran conflict, supply chain disruptions, inflationary pressures, and fears of AI-driven deflation in IT spending, contribute to this cautious outlook.

Sales growth among the top six IT firms is expected to be mixed, with cross-currency tailwinds providing a positive impact ranging from 12 to 72 basis points. Midcap companies such as Persistent Systems and Mphasis are expected to be at the higher end of sales growth estimates, while KPIT Technologies Ltd is forecast at the lower end, said Equirus.

Revenue growth across covered IT companies is projected to range between 0.5-9 per cent in rupee terms. Choice has revised target prices to reflect updated US rates and recent developments such as large deal wins and mergers and acquisitions. Margins are expected to improve slightly, with some companies delivering sequential expansions between 0-1.9 per cent.

Choice Institutional Equities maintains a preference for mid-cap IT companies, citing their stronger organic sequential performance compared to Tier-1 peers. Mid-cap firms benefit from better demand traction, execution resilience, and favourable growth profiles, supported further by currency tailwinds.

Equirus Securities anticipates Infosys will provide guidance for 1.5-4.5 per cent constant currency dollar sales growth for FY27, with EBIT margin guidance of 20-22 per cent. HCL Tech is expected to forecast 3-5 per cent sales growth in services, with EBIT margins of 17.5-18.5 per cent. Wipro may guide for a slight sales dip to modest growth in the first quarter of fiscal 2027.

Overall, the Indian IT sector appears poised for steady growth in Q4FY26E, with currency movements and AI-led efficiencies playing key roles, notes Choice. The sector’s ability to navigate macro headwinds and maintain deal momentum will be critical. Its outlook underscores confidence in the sector’s execution capabilities and growth potential.

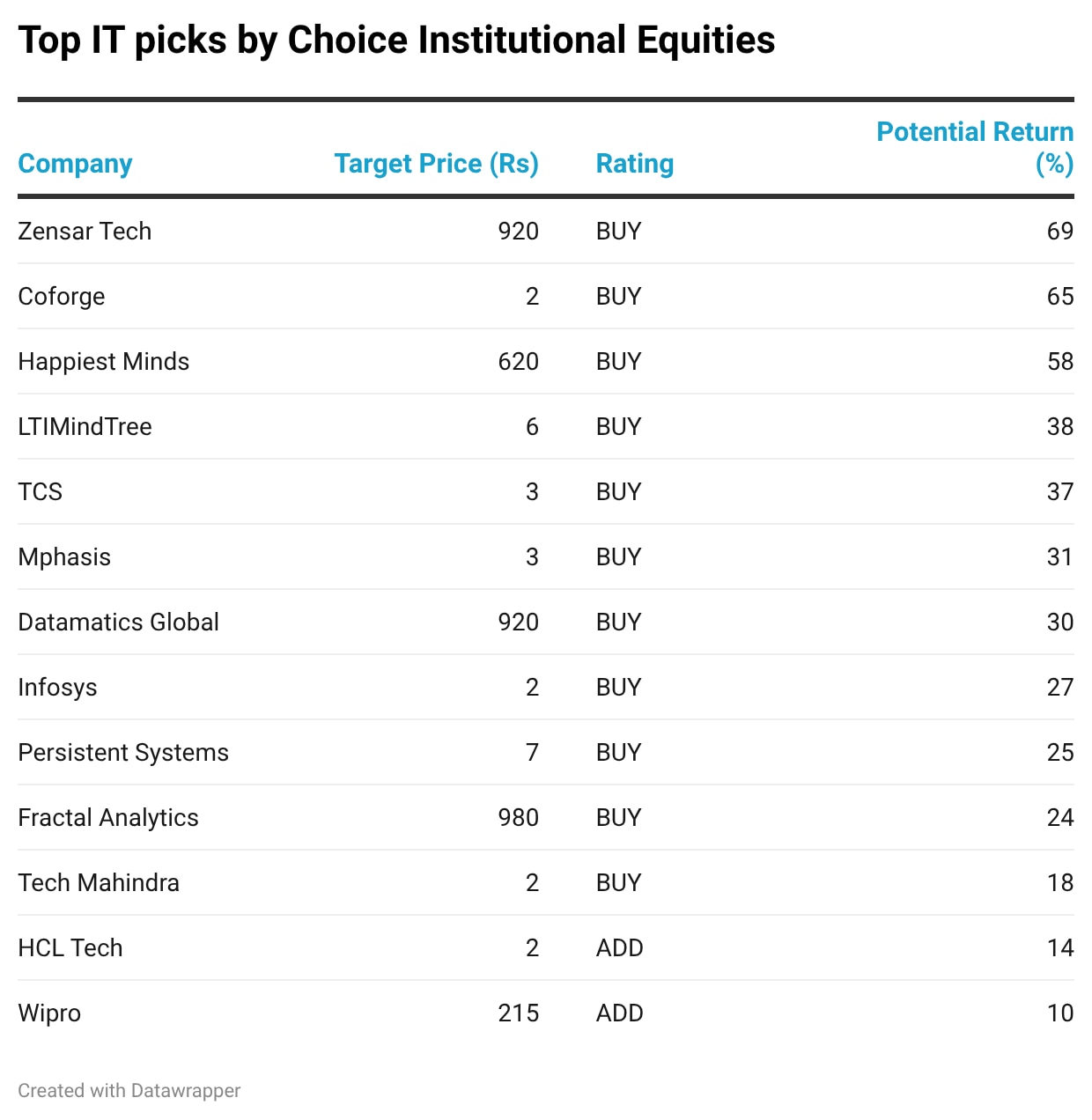

Choice identifies Coforge (Target Price: Rs 2,000), Persistent (Target Price: Rs 6,515), Happiest Minds (Target Price: Rs 620) and Fractal Analytics (Target Price: Rs 980) as preferred long-term investment ideas within the sector. These companies are expected to sustain relative outperformance in the current quarter.

Choice has a 'buy' ratings on Zensar Tech (Target Price: Rs 920), LTIMindTree (Target Price: Rs 5,920), TCS (Target Price: Rs 3,350), Mphasis (Target Price: Rs 2,888), Datamatics (Target Price: Rs 920), Infosys (Target Price: Rs 1,650) and Tech (Target Price: Rs 1,700) as well. HCL Technologies (Target Price: Rs 1,600) and Wipro (Target Price: Rs 215) have an 'add' rating from Choice.

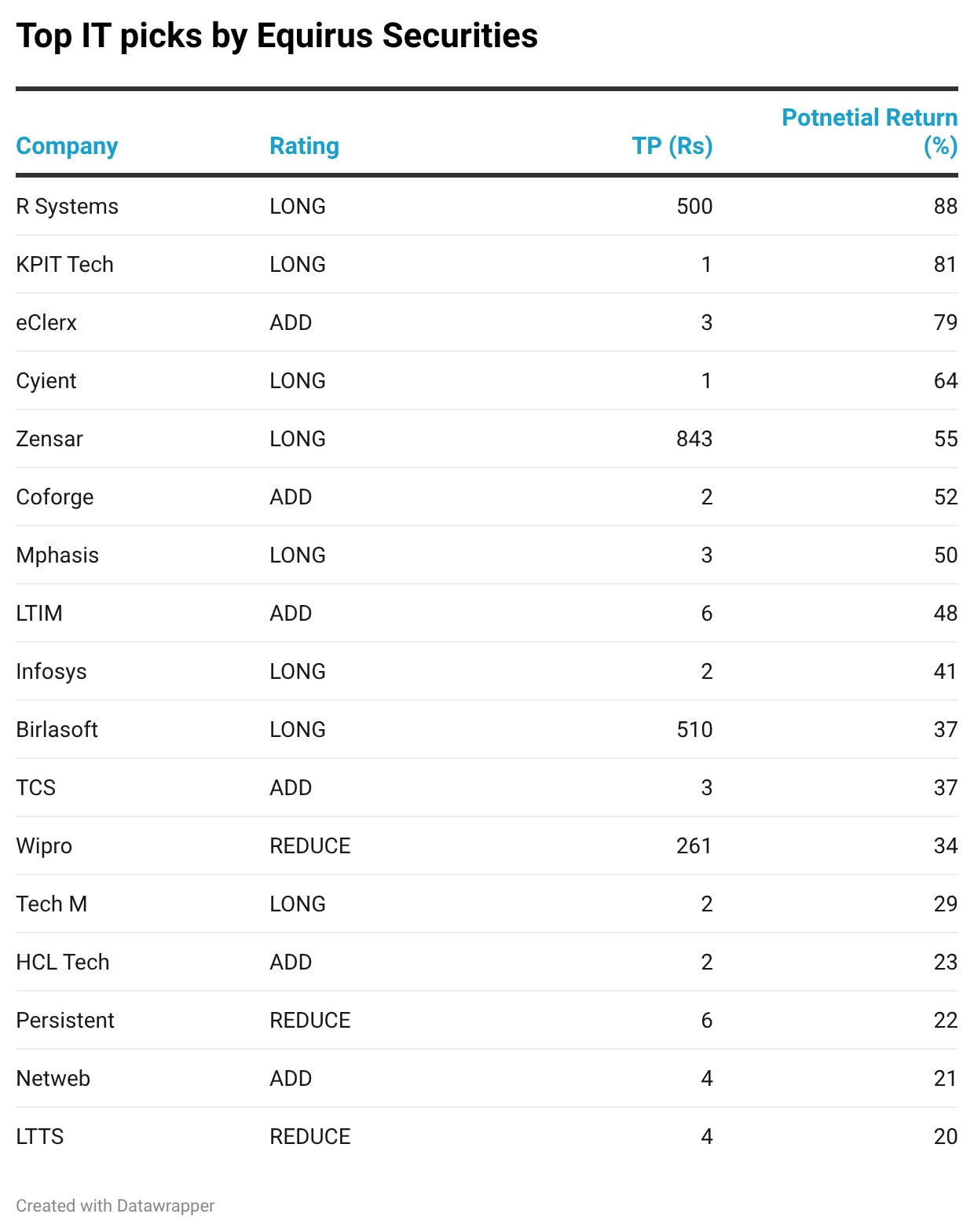

Among large caps, Infosys (Target Price: Rs 1,835) and Tech Mahindra (Target Price: Rs 1,855) are preferred by Equirus, while Mphasis (Target Price: Rs 3,315), Zensar (Target Price: Rs 843), KPIT Technologies (Target Price: Rs 1,265) and Birlasoft Ltd (Target Price: Rs 510) are favoured among midcaps, giving them 'long' rating. It sees up to 90 per cent upside in select IT stocks.

It also has a 'long' rating on Cyient (Target Price: Rs 1,320), R Systems (Target Price: Rs 500), while Eclerx (Target Price: Rs 2,585), Coforge (Target Price: Rs 1,838), LTIMindTree (Target Price: Rs 6,375), TCS (Target Price: Rs 3,355) and HCL Tech (Target Price: Rs 1,720) have an 'add' rating. Equirus has a 'reduce' rating on Wipro (Target Price: Rs 261), Persistent (Target Price: Rs 6,400) and LTTS (Target Price: Rs 4,020).

Resignation of part-time chairman a challenging event; raised questions on lender's governance standards: HDFC Bank MD and CEO Jagdishan

Resignation of part-time chairman a challenging event; raised questions on lender's governance standards: HDFC Bank MD and CEO Jagdishan '1,000 missiles are locked, loaded': Trump's latest threat to Iran could hit fuel prices worldwide

'1,000 missiles are locked, loaded': Trump's latest threat to Iran could hit fuel prices worldwide HDFC Bank FY26 report: AI ambitions, wealth growth, ESG focus, ₹60,000 crore fundraise

HDFC Bank FY26 report: AI ambitions, wealth growth, ESG focus, ₹60,000 crore fundraise Akasa Air pauses Noida–Navi Mumbai route weeks after launch amid network review: Report

Akasa Air pauses Noida–Navi Mumbai route weeks after launch amid network review: Report Apple sues OpenAI over alleged trade secret theft: What happened and why it matters

Apple sues OpenAI over alleged trade secret theft: What happened and why it matters FM Sitharaman Targets 5,000 GCCs By 2030 As Global Giants Like Air Liquide Expand Into India!

FM Sitharaman Targets 5,000 GCCs By 2030 As Global Giants Like Air Liquide Expand Into India!, Noise Rep Hands-on") The Tech Gear Show #10 | Tech News, ALT Buds Open Review, Nothing Phone (4b), Noise Rep Hands-on

The Tech Gear Show #10 | Tech News, ALT Buds Open Review, Nothing Phone (4b), Noise Rep Hands-on #Podcast Ep15: BMW India President Hardeep Singh Brar On EVs, Luxury Cars, Ethanol & Mobility Future

#Podcast Ep15: BMW India President Hardeep Singh Brar On EVs, Luxury Cars, Ethanol & Mobility Future Banks, Techs Rally On Dalal Street As Nifty Jumps

Banks, Techs Rally On Dalal Street As Nifty Jumps PM Modi Arrives in Auckland For First State Visit To New Zealand In 40 Years; Focus On Trade & Ties

PM Modi Arrives in Auckland For First State Visit To New Zealand In 40 Years; Focus On Trade & Ties Is India's IPO pipeline creating a new generation of investor-ready startups?

Is India's IPO pipeline creating a new generation of investor-ready startups? 4 Nifty FMCG stocks to buy after 32% selloff: What past 4 big falls since 2004 hint at

4 Nifty FMCG stocks to buy after 32% selloff: What past 4 big falls since 2004 hint at Persistent Systems fixes record date for Rs 18 final dividend; check details

Persistent Systems fixes record date for Rs 18 final dividend; check details DMart Q1 earnings preview: Net profit, EBITDA may grow in double digits; demand outlook among key things to track

DMart Q1 earnings preview: Net profit, EBITDA may grow in double digits; demand outlook among key things to track  Sensex, Nifty extend gains; Rs 5.8 lakh crore investor wealth added; what's ahead?

Sensex, Nifty extend gains; Rs 5.8 lakh crore investor wealth added; what's ahead?