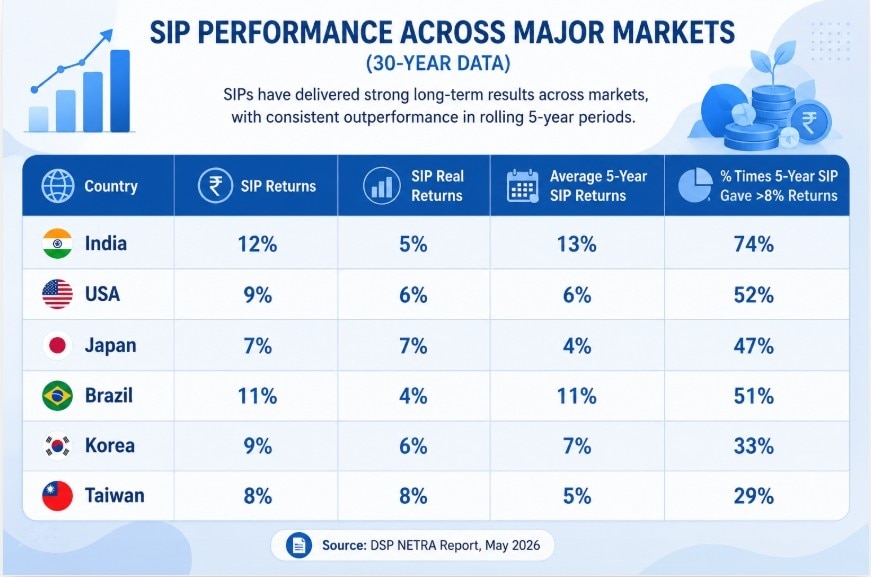

According to DSP, SIP investing has historically delivered positive real returns across most global markets over long periods, including India, the US, Japan, and several emerging economies.

According to DSP, SIP investing has historically delivered positive real returns across most global markets over long periods, including India, the US, Japan, and several emerging economies.Systematic Investment Plan (SIP) investors tend to outperform many market participants not because SIPs guarantee superior returns, but because they reduce behavioural mistakes and enforce disciplined investing, according to DSP Mutual Fund’s latest “NETRA – Early Signals Through Charts” report for May 2026.

The report argues that the gap between market returns and actual investor returns is often driven less by lack of knowledge and more by emotional decision-making. Fear during corrections, greed during rallies, panic selling, and recency bias frequently lead investors to mistime entries and exits, ultimately hurting long-term wealth creation.

Vinod Aggarwal, Vice Chairman of Eicher Motors; Sanjeev Arora, President, Motion Business at ABB India; Palash Srivastava, Deputy Managing Director at IIFCL and Nilesh Tribhuvan, Managing Partner, White & Brief Advocates & Solicitors") BT Infra Summit 2026: What will power India's next growth spurt?

BT Infra Summit 2026: What will power India's next growth spurt? BT Infra Summit 2026: How Sagarmala 2.0 is going to steer India's maritime growth

BT Infra Summit 2026: How Sagarmala 2.0 is going to steer India's maritime growth Why Bloomberg isn't ready to add Indian bonds yet despite sweeping market reforms

Why Bloomberg isn't ready to add Indian bonds yet despite sweeping market reforms BT Infra Summit 2026: India's energy security needs a new playbook as clean power, storage and grid modernisation take centre stage

BT Infra Summit 2026: India's energy security needs a new playbook as clean power, storage and grid modernisation take centre stage ITR filing 2026: WazirX launches free crypto tax reporting platform ahead of ITR deadline

ITR filing 2026: WazirX launches free crypto tax reporting platform ahead of ITR deadline Data Centres, Space & A Stable Rupee: India's Blueprint For The Next Growth Cycle

Data Centres, Space & A Stable Rupee: India's Blueprint For The Next Growth Cycle Red Sea Crisis: How Global Shipping Lines Are Navigating Another Major Disruption

Red Sea Crisis: How Global Shipping Lines Are Navigating Another Major Disruption Why EV Trucks Are Still Missing From India's Highways | BT Infrastructure Summit 2026

Why EV Trucks Are Still Missing From India's Highways | BT Infrastructure Summit 2026 #BTInfrastructureSummit: Powering India's New Growth Spurt With Infra, Investment & Innovation

#BTInfrastructureSummit: Powering India's New Growth Spurt With Infra, Investment & Innovation Why Indians Feel Foreign Infrastructure Is Better: Hitachi India CEO Breaks It Down

Why Indians Feel Foreign Infrastructure Is Better: Hitachi India CEO Breaks It Down Maruti Suzuki Q1 results: Profit slips 9% YoY to Rs 3,447 crore; revenue climbs 36%

Maruti Suzuki Q1 results: Profit slips 9% YoY to Rs 3,447 crore; revenue climbs 36% ITC Q1 results: Profit slips 16% to Rs 4,394 crore YoY; revenue climbs 28%

ITC Q1 results: Profit slips 16% to Rs 4,394 crore YoY; revenue climbs 28% BTTV Exclusive: M&M CEO Rajesh Jejurikar on Q1 earnings, business outlook, order book and more

BTTV Exclusive: M&M CEO Rajesh Jejurikar on Q1 earnings, business outlook, order book and more  Nifty IT stocks rebound in July as semiconductor shares falter; reverse AI trade at play?

Nifty IT stocks rebound in July as semiconductor shares falter; reverse AI trade at play? Dixon Technologies Q1 earnings: Net profit at Rs 718 crore, revenue rises 21%

Dixon Technologies Q1 earnings: Net profit at Rs 718 crore, revenue rises 21% Can AI Create Wealth For Everyone? DSCI CEO Explains The FutureData Centres, Space & A Stable Rupee: India's Blueprint For The Next Growth CycleRed Sea Crisis: How Global Shipping Lines Are Navigating Another Major DisruptionWhy EV Trucks Are Still Missing From India's Highways | BT Infrastructure Summit 2026#BTInfrastructureSummit: Powering India's New Growth Spurt With Infra, Investment & Innovation

Can AI Create Wealth For Everyone? DSCI CEO Explains The FutureData Centres, Space & A Stable Rupee: India's Blueprint For The Next Growth CycleRed Sea Crisis: How Global Shipping Lines Are Navigating Another Major DisruptionWhy EV Trucks Are Still Missing From India's Highways | BT Infrastructure Summit 2026#BTInfrastructureSummit: Powering India's New Growth Spurt With Infra, Investment & Innovation