Experts said keep gold and silver as portfolio stabilisers (hedge allocation), not aggressive return drivers. Rebalance rather than overweight.

Experts said keep gold and silver as portfolio stabilisers (hedge allocation), not aggressive return drivers. Rebalance rather than overweight. Experts said keep gold and silver as portfolio stabilisers (hedge allocation), not aggressive return drivers. Rebalance rather than overweight.

Experts said keep gold and silver as portfolio stabilisers (hedge allocation), not aggressive return drivers. Rebalance rather than overweight.After a year when gold rallied 72% in INR terms, silver surged 122%, and the Nifty 500 delivered a modest 7% return, investors face a markedly different landscape in 2026. According to 1 Finance’s Global Economic Outlook 2026, last year’s winners may not automatically lead this year.

The report argues that 2025 was defined by powerful narratives — falling real yields, aggressive central bank gold buying, supply deficits in silver and geopolitical stress. But 2026, it cautions, will be shaped by slower rate cuts, shifting global capital flows and India’s transition from slowdown to recovery. “2025 rewarded people who chased narratives. 2026 is a different game,” said Animesh Hardia, SVP, Quantitative Research at 1 Finance. “Rate cuts are slowing, geopolitical risks are recurring rather than one-off, and India is at an inflexion point.”

1. Don’t chase the winners blindly

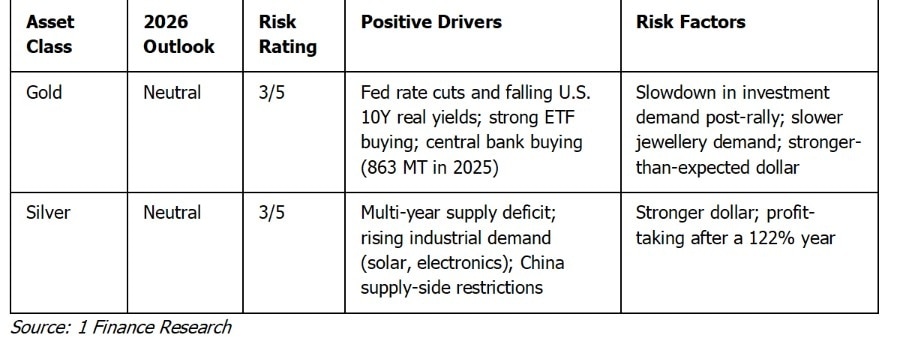

Gold and silver were the standout performers of 2025. Gold benefited from 863 metric tonnes of central bank buying and falling U.S. real yields. Silver rallied on multi-year supply deficits and accelerating demand from solar and electronics.

But the report assigns a neutral outlook to both metals in 2026.

That doesn’t mean exit — it means reset expectations.

Gold still has structural support from central bank accumulation and potential Fed easing. Silver retains industrial demand tailwinds. However, risks include:

Stronger dollar

Post-rally profit-taking

Moderation in jewellery demand

Slower global liquidity expansion

Guidebook takeaway: Keep gold and silver as portfolio stabilisers (hedge allocation), not aggressive return drivers. Rebalance rather than overweight.

2. Focus on India’s recovery cycle

The bigger shift may lie in equities — particularly India.

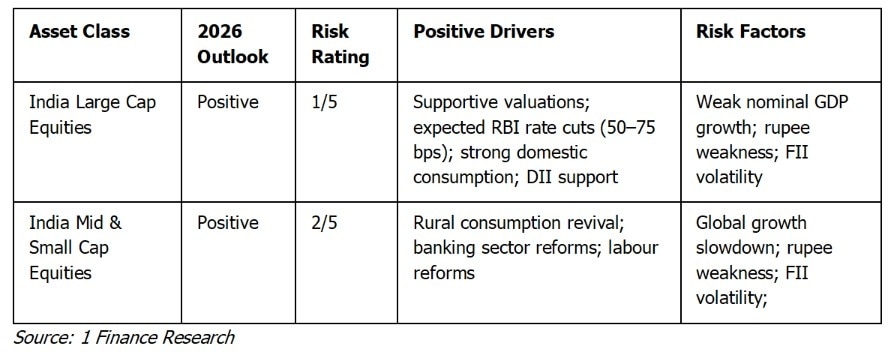

The report projects India’s GDP growth at 6.7% in CY26, with inflation averaging 3.9%, creating room for a 50–75 basis point repo rate cut. Its proprietary Macroeconomic Index shows India transitioning from a transitory slowdown in 2025 to a recovery phase in early 2026.

Yet the rebound is expected to be uneven.

Indian equities underperformed most global peers in 2025, weighed down by FPI outflows, a 6% rupee depreciation against the dollar and weak urban consumption. For 2026, large caps are viewed more favourably than mid and small caps, given stronger earnings visibility and potential FII re-entry.

The report projects:

GDP growth at 6.7% in CY26

Inflation at 3.9%

Potential 50–75 bps RBI rate cuts

Its proprietary macro index indicates India has transitioned from a transitory slowdown in 2025 to the early stages of recovery in 2026.

But recovery will not be uniform.

Large caps are better positioned than mid and small caps due to:

Stronger earnings visibility

More resilient balance sheets

Higher probability of FII re-entry

Attractive relative valuations

Hardia put it bluntly: “The year 2025 rewarded people who chased narratives. 2026 is a different game.”

He added: “The investors who do well this year will be the ones who understand which macro phase we're in and position accordingly.”

Guidebook takeaway: Tilt toward Indian large caps in the early recovery phase. Be selective in mid and small caps — focus on earnings durability, not theme-based rallies.

3. Be cautious on US equities

Globally, the outlook is fragmented. U.S. equities face headwinds from expensive valuations — the S&P 500 trades near 29 times earnings — alongside tariff-driven inflation risks and elevated public debt. In contrast, markets such as the U.K., China and Japan offer relatively better setups, supported by fiscal stimulus, AI-driven productivity gains and corporate reforms.

The report flags concerns in US markets:

S&P 500 P/E around 29x

Tariff-driven inflation risks

U.S. debt near $38 trillion

Slowing labour market signals

Meanwhile, selective opportunities may exist in the U.K., China and Japan, supported by stimulus and governance reforms.

Guidebook takeaway: Avoid blanket global exposure. Be valuation-sensitive. Geographic diversification matters more in 2026.

4. Understanding the new rate cycle

In 2025, markets priced aggressive rate cuts. In 2026:

The Fed is expected to deliver only limited cuts

The ECB may pause

The Bank of Japan could hike

Liquidity tailwinds are slowing. That changes asset behaviour.

Guidebook takeaway: Expect lower beta returns. Position for stability and earnings quality rather than multiple expansion.

5. Build allocation

The core message of the report is strategic: “The asset allocation needs to reflect that shift before it becomes obvious.”

The report noted 2026 is unlikely to be a crash year — but it is also unlikely to repeat 2025’s outsized commodity gains.

The 2026 Portfolio Blueprint

The investment playbook for 2026 calls for discipline, selectivity and macro awareness.

Core allocation: Indian large caps should form the backbone of portfolios, given improving domestic growth dynamics, potential RBI rate cuts and stronger earnings visibility relative to mid and small caps.

Stability layer: Gold deserves a measured allocation as a hedge against geopolitical and currency risks. After a sharp rally in 2025, expectations should be moderated, but its structural role as a portfolio stabiliser remains intact.

Tactical exposure: Silver can be considered a higher-volatility satellite position. While industrial demand and supply tightness support the long-term case, price swings are likely, making position sizing critical.

Selective global bets: Instead of broad exposure to expensive U.S. equities, investors may look at relatively better-valued markets such as the U.K., China and Japan, where policy support and structural reforms offer differentiated opportunities.

Risk control: Above all, portfolios should emphasise earnings quality, balance sheet strength and valuation discipline. Liquidity-driven multiple expansion is unlikely to be the dominant driver in 2026.

If 2025 was defined by momentum and macro stress, 2026 is likely to reward investors who recognise economic transitions early, rebalance with intent and avoid overexposure to last year’s narratives.

This year’s winners may not be the most dramatic performers — but the assets positioned correctly for the next phase of the cycle.

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls Same 43°C temperature, different reality: Why Europe's heatwave is more deadly than India's

Same 43°C temperature, different reality: Why Europe's heatwave is more deadly than India's 'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means

'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore

From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery

Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure