According to AMFI data, monthly SIP contributions have consistently crossed ₹32,087 crore in March 2026 and ₹29,845 crore in February 2026.According to AMFI data, monthly SIP contributions have consistently crossed ₹32,087 crore in March 2026 and ₹29,845 crore in February 2026.

According to AMFI data, monthly SIP contributions have consistently crossed ₹32,087 crore in March 2026 and ₹29,845 crore in February 2026.According to AMFI data, monthly SIP contributions have consistently crossed ₹32,087 crore in March 2026 and ₹29,845 crore in February 2026.A growing number of fintech platforms are turning to behavioural finance tools to nudge savings, and the latest example is a “Latte Factor Calculator” that quantifies how small daily expenses can compound into significant long-term wealth.

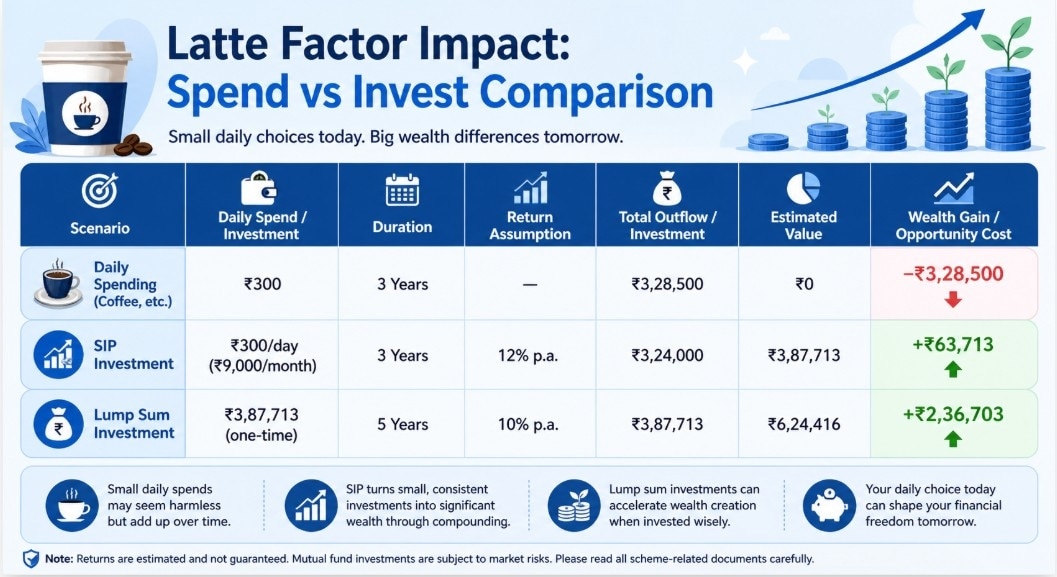

The concept, popularised in personal finance literature, refers to routine discretionary spending—such as daily coffee — that often goes unnoticed but adds up over time. The calculator allows users to input variables such as daily spend, investment duration, and expected returns to estimate both total expenditure and potential investment gains forgone.

In a sample scenario, a daily spend of ₹300 over three years translates to an outflow of ₹3.28 lakh in three years. However, if the same amount were systematically invested through a monthly SIP at an assumed annual return of 12%, the corpus could grow to approximately ₹3.87 lakh in three years. The nearly ₹60,000 difference highlights the opportunity cost of habitual consumption.

If invested in lumpsum, it can give you Rs 3,99,300 in 3 years at an annual return of 10%.

CALCULATE YOUR DAILY EXPENDITURE HERE

Financial planners say such tools are effective in illustrating the power of compounding, particularly for younger investors. Wealth advisors emphasise that the goal is not to completely eliminate discretionary spending, but to build awareness around the trade-offs involved. He noted that small behavioural changes, when consistently maintained over long periods, can have a meaningful impact on overall portfolio outcomes and long-term wealth creation.

The rise of such calculators comes at a time when retail participation in mutual funds and SIPs in India is at record highs. According to AMFI data, monthly SIP contributions have consistently crossed ₹32,087 crore in March 2026 and ₹29,845 crore in February 2026, driven largely by first-time investors in their 20s and 30s.

However, experts caution against oversimplification. Returns are market-linked and not guaranteed, and inflation can erode real gains. Additionally, financial well-being depends on a balanced approach that includes budgeting, emergency savings, and risk management.

Even so, the Latte Factor framework is gaining traction as a practical entry point into financial planning—turning everyday spending habits into a starting conversation about long-term wealth creation.

MUST READ: Is a dip-based SIP top-up strategy better than a regular SIP approach?

Investing in Mutual Funds

Building on this behavioural insight, lump sum investment projections further reinforce the long-term impact of disciplined financial decisions. Using the same example, if the accumulated ₹3.87 lakh — equivalent to the saved daily expense — is deployed as a one-time investment, the compounding effect becomes more pronounced over a longer horizon.

At an assumed annual return of 10% over five years, the investment could grow to approximately ₹6.24 lakh. Of this, nearly ₹2.36 lakh represents estimated returns, significantly exceeding the original principal. This highlights a critical distinction: while SIPs demonstrate the power of consistent investing, lump sum deployments can accelerate wealth creation when capital is available upfront and market conditions are favourable.

The visual breakdown between invested amount and estimated returns also underscores how compounding gains begin to contribute a larger share of the portfolio over time. In this case, returns account for over one-third of the final corpus, illustrating how time in the market remains a key driver of outcomes.

MUST READ: Can ₹14,000 monthly SIP build ₹1 crore for child's education? Expert breaks it down

Advisors note that the choice between SIP and lump sum should be aligned with cash flow patterns and market cycles. While SIPs help mitigate timing risk through rupee cost averaging, lump sum investments are often more effective during market corrections or when valuations are attractive.

Taken together, both scenarios strengthen the core message: reallocating small, habitual expenses into investments—whether periodically or as accumulated capital—can meaningfully alter long-term financial trajectories.

MUST READ: Small-cap funds jump up to 20% in April; should investors expect more gains?

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls Same 43°C temperature, different reality: Why Europe's heatwave is more deadly than India's

Same 43°C temperature, different reality: Why Europe's heatwave is more deadly than India's 'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means

'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore

From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery

Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure