Over the past year, the RBI has followed an easing trajectory, cutting the repo rate by a cumulative 125 basis points.Over the past year, the RBI has followed an easing trajectory, cutting the repo rate by a cumulative 125 basis points.

Over the past year, the RBI has followed an easing trajectory, cutting the repo rate by a cumulative 125 basis points.Over the past year, the RBI has followed an easing trajectory, cutting the repo rate by a cumulative 125 basis points.RBI repo rate 2026: As the Reserve Bank of India (RBI) prepares to announce its latest monetary policy decision, fixed deposit (FD) investors are closely watching the interplay between interest rates, inflation, and rising geopolitical risks -- particularly escalating tensions involving Iran.

The macroeconomic environment has shifted meaningfully in recent months. Heightened tensions in West Asia have triggered a rise in crude oil prices and raised concerns over supply disruptions. For India, a major oil importer, this has direct inflationary implications. Higher fuel and commodity costs tend to push up input prices across sectors, eventually feeding into retail inflation.

This evolving inflation trajectory is critical because it directly influences the RBI’s policy stance—and by extension, FD returns. While global conflicts may appear distant, their economic impact is transmitted through inflation and interest rate cycles, affecting domestic savings instruments like fixed deposits.

RBI rate cycle and FDs

Over the past year, the RBI has followed an easing trajectory, cutting the repo rate by a cumulative 125 basis points—from 6.25% in February 2025 to 5.25% by December 2025. The central bank has since maintained the rate at 5.25% in its latest policy reviews, signalling a pause after aggressive easing.

This rate-cut cycle led banks to gradually reduce FD interest rates, aligning deposit pricing with lower borrowing costs, easing inflation, and softer government bond yields. However, the current global backdrop complicates this trend.

If geopolitical tensions—such as the Iran-linked conflict—continue to push inflation higher, the RBI may be forced to reassess its accommodative stance. Any shift towards tightening or even a prolonged pause could stabilise or push FD rates higher in the coming quarters.

ALSO READ: Is lab-grown gold the future or just a costly experiment?

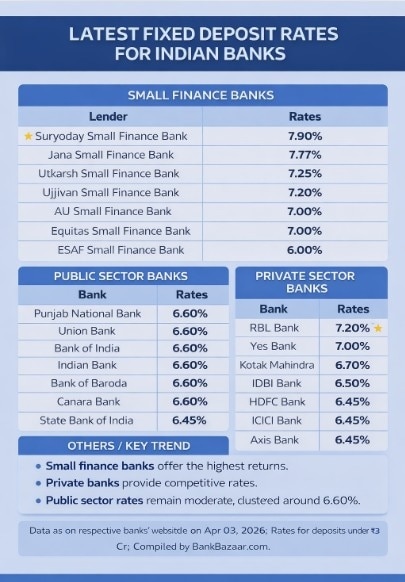

Where FD rates stand today

Fixed deposit (FD) rates across bank categories show a clear hierarchy, balancing return, safety, and risk. Public sector banks (PSBs) continue to offer relatively stable and clustered rates, with most large lenders such as Punjab National Bank, Bank of Baroda, Union Bank, and Canara Bank offering around 6.60%, while SBI remains slightly lower at 6.45%. This segment appeals to conservative investors prioritising capital safety and predictable returns.

Private sector banks offer moderately higher and more competitive rates. RBL Bank leads at 7.20%, followed by Yes Bank at 7.00%, while Kotak Mahindra Bank offers 6.70%. Large players like HDFC Bank, ICICI Bank, and Axis Bank remain in the 6.45%–6.50% range, providing a balance between returns and credibility.

Small finance banks offer the highest yields, led by Suryoday at 7.90%, Jana at 7.77%, and Ujjivan at 7.20%. However, these higher returns come with relatively higher perceived risk.

Outlook

Despite global uncertainties, FD rates are expected to remain broadly stable in the near term. Tight liquidity conditions and strong credit demand are supporting deposit rates, even as the RBI maintains a wait-and-watch approach.

ALSO READ: Investment 2026: Gold’s low correlation With equities makes it a strong diversifier: Report

However, the trajectory from here hinges on inflation. If crude oil prices remain elevated due to prolonged geopolitical tensions, upward pressure on inflation could emerge. This would increase the probability of a policy shift, potentially leading to higher FD rates.

For investors, the current phase presents a tactical opportunity -- locking in FD rates now could be beneficial, especially if rates stabilise before any future adjustments. At the same time, monitoring RBI signals and global developments remains essential, as the interest rate cycle appears to be entering a more uncertain and data-dependent phase.

RBI Gov Sanjay Malhotra has a few tricks up his sleeve to attract foreign capital

RBI Gov Sanjay Malhotra has a few tricks up his sleeve to attract foreign capital  Groww share price jumps 4% as Goldman Sachs buys shares; key details

Groww share price jumps 4% as Goldman Sachs buys shares; key details ‘Views don’t align on Tamil Nadu’: Annamalai says it's time to step out of BJP; full text of letter

‘Views don’t align on Tamil Nadu’: Annamalai says it's time to step out of BJP; full text of letter, Go Digit's profit after tax (PAT) increased 28.4 per cent year-on-year (YoY) to Rs 149 crore.") Go Digit shares jump over 10% in early trade; here's what happened

Go Digit shares jump over 10% in early trade; here's what happened BT Explainer: Centre exempts foreign investors from taxes on G-Sec investments via Ordinance -- What it means for India’s bond market

BT Explainer: Centre exempts foreign investors from taxes on G-Sec investments via Ordinance -- What it means for India’s bond market Citi Sees Massive Upside In Power Stocks! ₹9.7 Lakh Crore Opportunity Ahead

Citi Sees Massive Upside In Power Stocks! ₹9.7 Lakh Crore Opportunity Ahead Midcap Winners Ahead? Siddhartha Khemka Reveals Top Themes For FY27

Midcap Winners Ahead? Siddhartha Khemka Reveals Top Themes For FY27 Govt's Big Move To Save The Rupee! Will Foreign Money Return To India?

Govt's Big Move To Save The Rupee! Will Foreign Money Return To India? Q4 Earnings Surprise! BFSI, Metals Shine As FY28 Recovery Takes Shape | Siddhartha Khemka

Q4 Earnings Surprise! BFSI, Metals Shine As FY28 Recovery Takes Shape | Siddhartha Khemka Reliance Down 17%: Is This the Best Time to Buy Before Jio Listing?

Reliance Down 17%: Is This the Best Time to Buy Before Jio Listing? Refex Industries' arm enters Rs 100-crore revenue club; FY26 total income rises 2.5 times

Refex Industries' arm enters Rs 100-crore revenue club; FY26 total income rises 2.5 times TCS, Infosys shares on hold? Time to buy midcap IT stocks, says Antique | Target prices

TCS, Infosys shares on hold? Time to buy midcap IT stocks, says Antique | Target prices Adani Ports shares near record high: What brokerage says on crossing the Rs 2,100 mark

Adani Ports shares near record high: What brokerage says on crossing the Rs 2,100 mark Maruti Suzuki shares down 22% in 2026 so far; can India's first flex-fuel car aid recovery?Groww share price jumps 4% as Goldman Sachs buys shares; key details

Maruti Suzuki shares down 22% in 2026 so far; can India's first flex-fuel car aid recovery?Groww share price jumps 4% as Goldman Sachs buys shares; key details