Experts also emphasise building a dedicated emergency fund covering 6–12 months of expenses, reducing the need to liquidate investments under pressure.

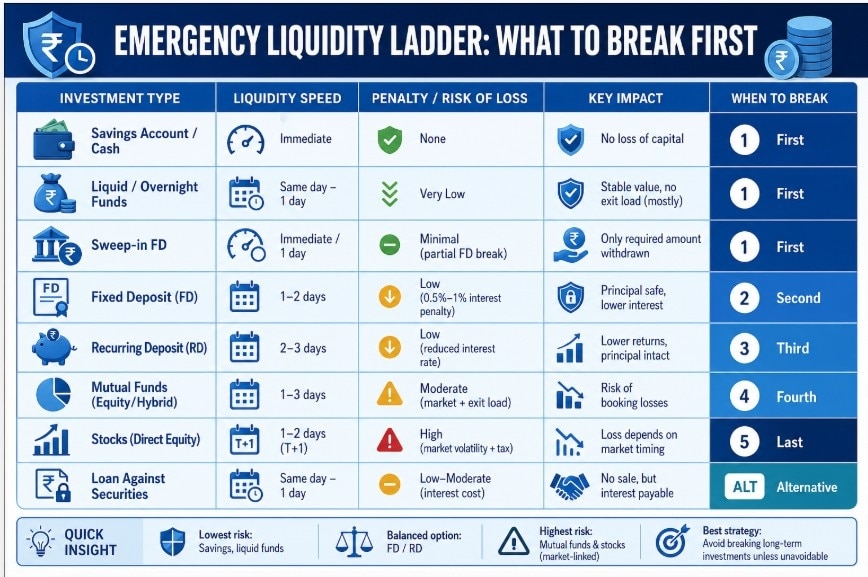

Experts also emphasise building a dedicated emergency fund covering 6–12 months of expenses, reducing the need to liquidate investments under pressure.In a financial emergency, the priority is clear: access funds quickly while minimising losses. Not all investments are equal in this regard. The order in which you liquidate assets — ranging from fixed deposits to equities —can significantly impact your long-term wealth. Financial planners recommend a structured “liquidity ladder,” where investors first tap the most liquid and least risky instruments, and avoid disturbing long-term, market-linked assets unless absolutely necessary.

Start with the safest and quickest options

The first line of defence should always be cash or savings accounts, followed by liquid or overnight mutual funds, which offer near-instant or next-day access with minimal risk. These instruments are specifically designed for emergencies and carry no exit penalties in most cases.

If available, sweep-in fixed deposits also provide flexibility, automatically breaking only the required amount without closing the entire deposit.

FDs and RDs

If liquid funds are insufficient, Fixed Deposits (FDs) should be the next choice. Breaking an FD is relatively simple and typically results in a 0.5%–1% interest penalty, while the principal remains सुरक्षित. Funds are usually credited within 1–2 working days.

Recurring Deposits (RDs) follow a similar structure. Premature withdrawal reduces the interest earned or applies a lower rate for the actual tenure. While slightly less flexible than FDs, RDs are still low-risk and reasonably liquid, making them suitable for emergency access.

MUST READ: Are Indian equities and GIFT City becoming top picks for NRI investors?

Mutual funds

Equity or hybrid mutual funds should be tapped only after exhausting safer options. Redemption is straightforward and funds are credited within 1–3 days, but the key risk lies in market volatility. Selling during a downturn can convert temporary losses into permanent capital erosion.

Additionally, some funds may impose exit loads, and taxation depends on holding period—short-term gains are taxed higher than long-term gains.

Stocks: Last resort

Direct equity should ideally be the last option. While shares can be sold quickly through trading apps, the risk of selling at depressed prices is high, especially during market stress. Even with India’s T+1 settlement cycle, funds may take a day to reflect, and capital gains tax applies.

An alternative is a loan against securities (LAS), where investors can pledge shares and access 45–50% of their portfolio value without selling holdings.

MUST READ: FD rates April 2026: SBI vs Bank of Baroda vs PNB — Which public sector bank offers better returns?

Strategic takeaway

The optimal order in an emergency is:

Savings / Liquid funds

Fixed Deposits

Recurring Deposits

Mutual Funds

Stocks

The underlying principle is simple — protect long-term growth assets and minimise losses.

Experts also emphasise building a dedicated emergency fund covering 6–12 months of expenses, reducing the need to liquidate investments under pressure. In addition, options like credit cards or loans against FDs can provide temporary liquidity without disrupting core investments. In volatile markets, disciplined liquidation, not panic selling, can make the difference between a temporary setback and long-term financial damage.

MUST READ NOW: Where are FD rates highest now? Comparing small finance banks with private, public sector banks

Vikram-1 launch today: What the mission is about, launch date, time, objectives, its significance for India

Vikram-1 launch today: What the mission is about, launch date, time, objectives, its significance for India 'Vikram-1 will prove our commercial product': Skyroot Aerospace CEO Pawan Kumar Chandana as start-up gears up for lift-off

'Vikram-1 will prove our commercial product': Skyroot Aerospace CEO Pawan Kumar Chandana as start-up gears up for lift-off Old Pension Scheme comeback? Why more employees are getting another chance to opt for OPS

Old Pension Scheme comeback? Why more employees are getting another chance to opt for OPS RIL Q1 net sales up 25%; what Mukesh Ambani says on Jio Platforms IPO

RIL Q1 net sales up 25%; what Mukesh Ambani says on Jio Platforms IPO deposit interest is exempt from income tax in India, provided the applicable eligibility conditions are met.") Top FCNR(B) deposit rates: Banks raise returns on USD, GBP, EUR, CAD and AUD FDs

Top FCNR(B) deposit rates: Banks raise returns on USD, GBP, EUR, CAD and AUD FDs Faith Conclave 2026: Tourism Leaders Chart India’s Seamless Global Growth Roadmap

Faith Conclave 2026: Tourism Leaders Chart India’s Seamless Global Growth Roadmap No Diesel, No Emissions: PM Modi Launches India's First Hydrogen Train

No Diesel, No Emissions: PM Modi Launches India's First Hydrogen Train Mercedes CEO: Cars Are E25 Ready, India Among Top 5 Maybach Markets | Santosh Iyer Exclusive

Mercedes CEO: Cars Are E25 Ready, India Among Top 5 Maybach Markets | Santosh Iyer Exclusive Tech Gear Show EP 11 | Tech News, JBL Live 780NC Review, Motorola Edge 70 MAX Unboxing

Tech Gear Show EP 11 | Tech News, JBL Live 780NC Review, Motorola Edge 70 MAX Unboxing Faith Conclave 2026: VFS Global’s Yummi Talwar On Building Resilient Global Tourism Organisations

Faith Conclave 2026: VFS Global’s Yummi Talwar On Building Resilient Global Tourism Organisations Jio Platforms Q1 earnings: IPO-bound firm logs Rs 45,961 crore revenue, profit up 9%

Jio Platforms Q1 earnings: IPO-bound firm logs Rs 45,961 crore revenue, profit up 9%  Reliance Retail Q1 results: Net profit at Rs 2,805 crore, revenue rises 7% RIL Q1 net sales up 25%; what Mukesh Ambani says on Jio Platforms IPO

Reliance Retail Q1 results: Net profit at Rs 2,805 crore, revenue rises 7% RIL Q1 net sales up 25%; what Mukesh Ambani says on Jio Platforms IPO Foreign investors may rotate to India as AI trade froth fades, says Gaurang Shah

Foreign investors may rotate to India as AI trade froth fades, says Gaurang Shah Gaurang Shah picks Indian Bank, SBI, ICICI Bank, Federal Bank as preferred banking bets

Gaurang Shah picks Indian Bank, SBI, ICICI Bank, Federal Bank as preferred banking bets