Among public sector banks (PSBs), State Bank of India (SBI), Bank of Baroda (BoB), and Punjab National Bank (PNB) remain the top choices for conservative investors.Among public sector banks (PSBs), State Bank of India (SBI), Bank of Baroda (BoB), and Punjab National Bank (PNB) remain the top choices for conservative investors.

Among public sector banks (PSBs), State Bank of India (SBI), Bank of Baroda (BoB), and Punjab National Bank (PNB) remain the top choices for conservative investors.Among public sector banks (PSBs), State Bank of India (SBI), Bank of Baroda (BoB), and Punjab National Bank (PNB) remain the top choices for conservative investors.Fixed deposits (FDs) are increasingly being viewed as a tactical allocation tool rather than just a safety net, especially in a stabilising interest rate environment. With the Reserve Bank of India (RBI) holding the repo rate steady at 5.25% for the second consecutive meeting, FD rates across banks appear to have plateaued — making this a crucial window for investors to lock in yields.

Among public sector banks (PSBs), State Bank of India (SBI), Bank of Baroda (BoB), and Punjab National Bank (PNB) remain the top choices for conservative investors. While all three offer relatively similar returns in the 6%–6.6% range, a closer comparison reveals meaningful differences across tenures.

SBI vs BoB vs PNB

Short-term deposits (1 year): SBI offers around 6.25% for 1-year deposits, slightly ahead of PNB at 6.25% and Bank of Baroda at 6.10%. For short-duration investors, SBI and PNB are marginally more attractive.

Medium-term deposits (2–3 years): This is where competition intensifies.

PNB offers around 6.30% for both 2 and 3 years

BoB provides 6.25% for 2–3 years

SBI remains slightly lower at around 6.25%–6.30%

The differences are narrow, but PNB edges ahead in the 2–3 year segment.

Special tenure schemes:

Bank of Baroda’s 444-day “Square Drive Deposit Scheme” stands out with rates up to 6.45%, making it one of the highest among PSU banks.

Similarly, SBI’s “Amrit Vrishti” (444 days) offers around 6.45%, slightly revised from earlier levels.

These special schemes are currently the sweet spot for investors looking to maximise returns within PSU banks.

Long-term deposits (5 years):

All three banks converge in this segment:

SBI: ~6.00%

PNB: ~6.10%

BoB: ~6.30%

Bank of Baroda offers a slight premium for long-term investors, although the overall return remains moderate.

MUST READ: April 2026 FD rates: Where public, private banks, small finance banks, NBFCs stand

Senior citizen advantage

All three banks provide an additional 50–75 basis points for senior citizens.

SBI and PNB offer rates up to ~7%+ for select tenures

BoB also reaches around 7%+, especially in special schemes

This makes PSU bank FDs particularly attractive for retirees seeking stable income.

Safety vs returns

Despite small finance banks offering rates above 8%, PSU banks continue to attract a large share of deposits. The reason is simple: trust and perceived sovereign backing.

For risk-averse investors, especially retirees and those parking large sums, SBI, BoB, and PNB offer:

High credibility

Strong balance sheets

Lower perceived default risk

However, this safety comes at the cost of slightly lower returns.

MUST READ: Where does your investment money actually go? A breakdown across 17 asset classes in India

Strategic takeaway: Where should you invest?

Best short-term (1 year): SBI / PNB (marginal edge)

Best medium-term (2–3 years): PNB

Best special tenure: SBI & BoB (444-day schemes)

Best long-term (5 years): Bank of Baroda

In the current rate cycle, investors should focus less on marginal rate differences and more on tenure strategy and liquidity needs. Laddering FDs across 1–3 years, while allocating a portion to special schemes like 444 days, can help optimise returns.

Other FD rates

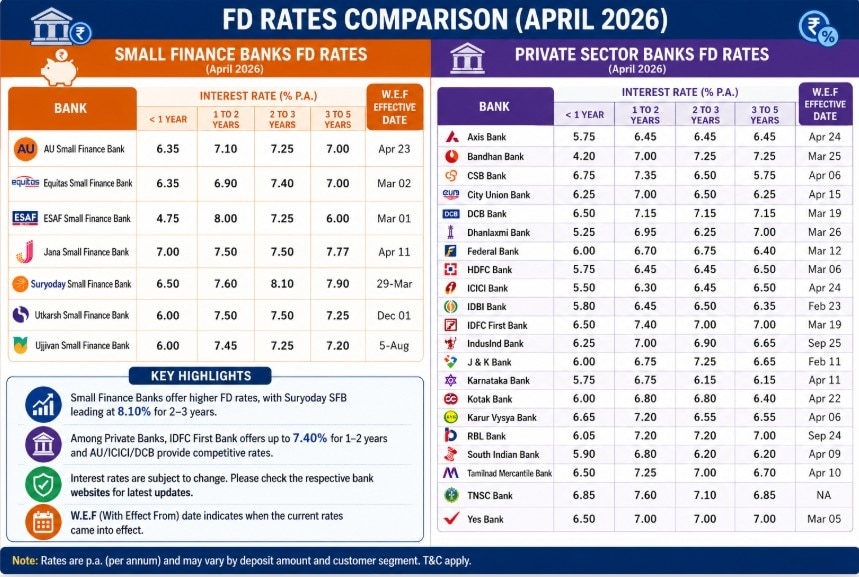

Small Finance Banks

Small finance banks continue to dominate the high-yield segment. Suryoday Small Finance Bank is offering up to 8.1%, while ESAF and Jana Small Finance Banks are in the 7.5%–8% range across key tenures.

These rates are significantly higher than the broader market, but they come with trade-offs. Investors need to consider deposit insurance limits (₹5 lakh per bank) and the relatively lower balance sheet strength compared to larger institutions.

For yield-seeking investors, a diversified allocation across multiple banks—rather than concentrating funds in one—can help balance risk.

Private Banks

Private sector banks are positioning themselves as a middle ground. IDFC First Bank offers up to 7.4%, while DCB, RBL, and Bandhan Bank are in the 7%+ range for select tenures.

Meanwhile, large private lenders such as HDFC Bank, ICICI Bank, and Axis Bank offer lower but more stable returns in the 6.3%–6.5% band. These banks appeal to investors who prioritise credibility, liquidity, and convenience over marginal yield gains.

SpaceX IPO scripts history: Elon Musk becomes world’s first trillionaire

SpaceX IPO scripts history: Elon Musk becomes world’s first trillionaire Sensex, Nifty: Why stock market is rising today after Trump's Iran deal comment

Sensex, Nifty: Why stock market is rising today after Trump's Iran deal comment  ‘No Indian weapon ever used to attack Europe…’: Jaishankar’s sharp rebuttal on Russia ties

‘No Indian weapon ever used to attack Europe…’: Jaishankar’s sharp rebuttal on Russia ties Govt wants smarter, safer roads and connected vehicles. It has now set a plan in motion

Govt wants smarter, safer roads and connected vehicles. It has now set a plan in motion Vedanta demerger: Listing date out for Oil & Gas, Power, Aluminium and Iron & Steel firms

Vedanta demerger: Listing date out for Oil & Gas, Power, Aluminium and Iron & Steel firms Power Stocks Too Expensive? Ashish Chaturmohta Explains Wire And T&D Stocks

Power Stocks Too Expensive? Ashish Chaturmohta Explains Wire And T&D Stocks Ashish Chaturmohta Talks About The Top 2 Themes That Could Boost Your Portfolio

Ashish Chaturmohta Talks About The Top 2 Themes That Could Boost Your Portfolio Ram Mandir, Mathura & Bhojshala: Minister Gajendra Shekhawat Outlines Modi Govt's Cultural Roadmap!

Ram Mandir, Mathura & Bhojshala: Minister Gajendra Shekhawat Outlines Modi Govt's Cultural Roadmap! Chandrababu Naidu Praises Modi's Leadership, Says Viksit Bharat Goal Is Achievable

Chandrababu Naidu Praises Modi's Leadership, Says Viksit Bharat Goal Is Achievable Indian I.T. Stocks Crash Again: AI Disruption Sparks Fresh Sell-Off In Nifty I.T.

Indian I.T. Stocks Crash Again: AI Disruption Sparks Fresh Sell-Off In Nifty I.T. Hexagon Nutrition shares list at 7% premium: Should you exit or hold for long-term?Vedanta demerger: Listing date out for Oil & Gas, Power, Aluminium and Iron & Steel firmsSensex, Nifty: Why stock market is rising today after Trump's Iran deal comment

Hexagon Nutrition shares list at 7% premium: Should you exit or hold for long-term?Vedanta demerger: Listing date out for Oil & Gas, Power, Aluminium and Iron & Steel firmsSensex, Nifty: Why stock market is rising today after Trump's Iran deal comment  Premier Energies a buy; Tata Motors PV, VBL, HDFC Bank, BHEL, Tata Power among insurers' top sells SpaceX IPO scripts history: Elon Musk becomes world’s first trillionaire

Premier Energies a buy; Tata Motors PV, VBL, HDFC Bank, BHEL, Tata Power among insurers' top sells SpaceX IPO scripts history: Elon Musk becomes world’s first trillionaire