Fitch stated that the current surge in oil prices is primarily a logistical supply shock rather than a permanent loss of production capacity.. (Image: India Today)

Fitch stated that the current surge in oil prices is primarily a logistical supply shock rather than a permanent loss of production capacity.. (Image: India Today) Fitch stated that the current surge in oil prices is primarily a logistical supply shock rather than a permanent loss of production capacity.. (Image: India Today)

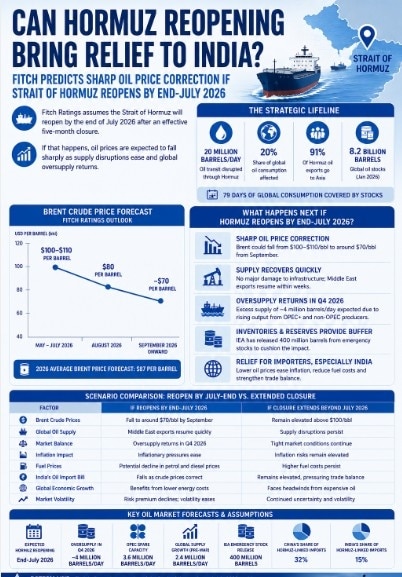

Fitch stated that the current surge in oil prices is primarily a logistical supply shock rather than a permanent loss of production capacity.. (Image: India Today)The future direction of global oil prices may hinge on a single question: Will the Strait of Hormuz reopen by the end of July 2026? According to a new report by Fitch Ratings, the answer is likely yes.

The ratings agency's base-case scenario assumes the strategic waterway, which handles about one-fifth of global oil consumption, will reopen around the end of July after an effective five-month closure. If that happens, Fitch expects the current oil price spike to reverse sharply, with Brent crude potentially falling to around $70 per barrel from September.

The Strait of Hormuz is one of the world's most critical energy chokepoints. Before the disruption, roughly 20 million barrels of oil equivalent per day, including crude and petroleum products, moved through the route connecting the Persian Gulf to global markets. The closure disrupted exports from Saudi Arabia, the UAE, Iraq, Kuwait and Iran, while major buyers such as India and China faced supply risks.

Surge in oil prices

However, Fitch argues that the current surge in oil prices is primarily a logistical supply shock rather than a permanent loss of production capacity. The agency believes there has been no material damage to regional oil infrastructure, allowing Middle Eastern production to recover quickly once shipping routes normalize.

Under its base-case forecast, Brent crude is expected to average $100-$110 per barrel during May-July, decline to around $80 per barrel in August, and fall further to approximately $70 per barrel from September onward. Fitch's overall 2026 Brent forecast stands at $87 per barrel.

Global oil market

The agency expects the global oil market to return to oversupply in the fourth quarter of 2026. Rapid recovery in Middle East production, strong non-OPEC supply growth and the possibility of higher OPEC output could create an excess supply of roughly 4 million barrels per day, putting downward pressure on prices.

Fitch also highlights several factors supporting its reopening assumption. These include the peak U.S. summer driving season, upcoming U.S. economic data releases, political considerations ahead of mid-term elections, and China's need to preserve oil inventories. The report notes that China could face growing pressure on reserves if the disruption persists for several more months.

Global consumption

Another key reason behind Fitch's relatively bearish outlook is the availability of substantial global oil inventories. Worldwide oil stocks stood at 8.2 billion barrels in January 2026, equivalent to about 79 days of global consumption. The International Energy Agency has already announced the release of 400 million barrels from emergency reserves, helping offset supply disruptions.

Meanwhile, structural changes in the global energy market are also reducing the impact of geopolitical shocks. OPEC's share of global oil production has fallen significantly over the past five decades, while U.S. production has grown substantially. At the same time, slowing oil demand growth, rising electric vehicle adoption and increasing energy efficiency have contributed to a structurally oversupplied market.

Still uncertainty high

Still, Fitch cautions that uncertainty remains high. If Hormuz reopens earlier than expected, oil prices could fall faster. Conversely, a prolonged disruption could keep crude above $100 per barrel for longer, intensifying inflationary pressures and raising energy costs for major importers such as India, China, Japan and South Korea.

For now, global oil markets remain focused on one event: the reopening of Hormuz. If Fitch's forecast proves correct, today's supply shock could quickly give way to a renewed era of abundant oil supply and lower prices.

Netanyahu names India as key ally after Vance says Israel has 'only one powerful friend' left

Netanyahu names India as key ally after Vance says Israel has 'only one powerful friend' left Maya Tata, daughter of Noel Tata, set to take charge of Westside’s digital expansion: Report

Maya Tata, daughter of Noel Tata, set to take charge of Westside’s digital expansion: Report.") Suzlon, Waaree Energies, ACME Solar, NTPC Green: Share price targets, Q1 results preview

Suzlon, Waaree Energies, ACME Solar, NTPC Green: Share price targets, Q1 results preview Best small finance bank FD? Unity vs Utkarsh interest rates compared for 2026

Best small finance bank FD? Unity vs Utkarsh interest rates compared for 2026 Retirement after 60: Can annuities help you avoid outliving your retirement savings? Here's how

Retirement after 60: Can annuities help you avoid outliving your retirement savings? Here's how ITR Filing 2026: Common Mistakes To Avoid, New Deadlines Explained & Tips To Prevent Tax Notices

ITR Filing 2026: Common Mistakes To Avoid, New Deadlines Explained & Tips To Prevent Tax Notices Market Expert Flags Sectors To Avoid Now And Reveals A High-Risk Opportunity For Investors

Market Expert Flags Sectors To Avoid Now And Reveals A High-Risk Opportunity For Investors TVS Capital Funds’ ₹4,000 Crore Investment Plan

TVS Capital Funds’ ₹4,000 Crore Investment Plan Mega IPOs To Shake Indian Stock Market? SBI AMC, NSE, Jio Platforms And Liquidity Impact Explained

Mega IPOs To Shake Indian Stock Market? SBI AMC, NSE, Jio Platforms And Liquidity Impact Explained Power Demand Is Booming: Market Expert Reveals Why Energy Stocks Could Be The Next Winners

Power Demand Is Booming: Market Expert Reveals Why Energy Stocks Could Be The Next Winners BEL, HAL, BDL, Mazagon Dock: Target prices, defence stocks to buy after Rs 52,000 cr DAC approvals

BEL, HAL, BDL, Mazagon Dock: Target prices, defence stocks to buy after Rs 52,000 cr DAC approvals Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty down 30 pts; key levels to watch

Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty down 30 pts; key levels to watch Top stocks in news: HDFC Bank, NBCC, YES Bank, Aastha, Dabur, RBL Bank, PTC India, IndusIndSuzlon, Waaree Energies, ACME Solar, NTPC Green: Share price targets, Q1 results preview

Top stocks in news: HDFC Bank, NBCC, YES Bank, Aastha, Dabur, RBL Bank, PTC India, IndusIndSuzlon, Waaree Energies, ACME Solar, NTPC Green: Share price targets, Q1 results preview Zomato, Swiggy shares: How to play the quick commerce theme ahead of a potential Zepto IPO

Zomato, Swiggy shares: How to play the quick commerce theme ahead of a potential Zepto IPO