Income of the working population needs to be raised through significant increase in urban and rural wages to revive consumer demands.Income of the working population needs to be raised through significant increase in urban and rural wages to revive consumer demands.

Income of the working population needs to be raised through significant increase in urban and rural wages to revive consumer demands.Income of the working population needs to be raised through significant increase in urban and rural wages to revive consumer demands.Last week, the Britannia Industries' managing director sent shockwaves, so to speak, by remarking that people were thinking twice before buying even a packet of biscuit for Rs 5. Another leading biscuit maker, Parle Products, joined in earlier this week to say that it might have to lay off 10,000 workers. All this is because consumer demand has collapsed.

This phenomenon is not limited to the FMCG segment by any stretch of the imagination. The auto industry has been in turmoil for quite some time with some of the leading players screaming aloud about inventory pile-ups, suspension of production and job cuts by the thousands.

None of this, however, should come as a surprise. The telltale signs have always been there but little attention was paid.

Low industrial production and capacity utilisation

Take the industrial production. The index of industrial production (IIP) - which measures production in the areas of mining and quarrying, manufacturing and electricity - has remained very low. Growth in manufacturing IIP, which accounts for 77.63% of the IIP (base year 2011-12), has remained confined to a far lower band of 2.8% to 4.8% (an annual average of 4%) in the past seven years between 2011-12 and 2018-19.

This is not only way below the GDP growth for all these years but it is substantially lower than that of the manufacturing IIP for the previous six years between 2004-05 and 2010-11 (base year of 2004-05). Then it averaged 10% annual growth.

Not just that, the capacity utilisation of the manufacturing units, an indicator of demand which shows productive capacity being used for generating goods and services, has also remained low, reflecting low demand for manufacturing goods.

The RBI's quarterly surveys (OBICUS) show capacity utilisation has remained confined, more or less, to 70-75% in the past 11 years. The last time it touched 80% was way back in 2009-10 and 2010-11.

What these three graphs demonstrate is that both manufacturing production and demand for it have been severely hit.

Therefore, there is little reason for the manufacturing industry to expand capacity.

This is also reflected in the growth of capital goods.

Little capacity expansion activities

The IIP for capital goods (base 2011-12) has moved only by an index value of 8.4 (from 100 to 108.4) between the base year of 2011-12 and 2018-19. Worse, it was in the negative zone for two of these years. The following graph shows growth of the IIP for capital goods in percentage.

Import of capital goods does not reflect a rosy picture either, further establishing that little capacity expansion activity is going on in the economy.

In fact, the RBI's Index Number of Imports (Quantum) of machinery and transport equipment (as a proxy of capital goods) shows that the quantum of import has fallen drastically from an index value (base year 1999-2000) of 549 in 2009-10 to less than half, 264, in 2017-18 - the last year for which data is available.

The quantum import index has stagnated for the past seven years as graph 5 shows.

Falling bank credit and capital formation

This state of the Indian industry is further reflected in the growth of bank credits to industry and capital formations.

The following graph traces the growth in bank credits to the non-food sector and its industry component for the past decade (the non-food sector comprises of industry, agriculture and allied activities, services and personal loans), showing a drastic fall, after peaking in 2010.

The growth in bank credit for the industry peaked at 24.4% in 2010, entered the negative zone in 2017 and has shown signs of recovery to click 6.9% in 2019.

For the non-food sector as a whole, the growth peaked at 16.8% in 2009 and registered 12.3% in 2019. Detailed analysis shows that the services and personal loans segments are playing a bigger role in keeping the picture a lot healthier - rather than the industry.

The level of investment in the economy, reflected in the gross fixed capital formation (GFCF), also shows a similar trend.

The GFCF as a percentage of GDP fell from a peak level of 34.3% in 2011-12 to 30.3% in 2015-16. It is going up (32.3% in 2018-19) but not reached the 2011-12 level yet.

What all the data presented through seven graphs show is that there is just no demand for manufacturing products in the economy.

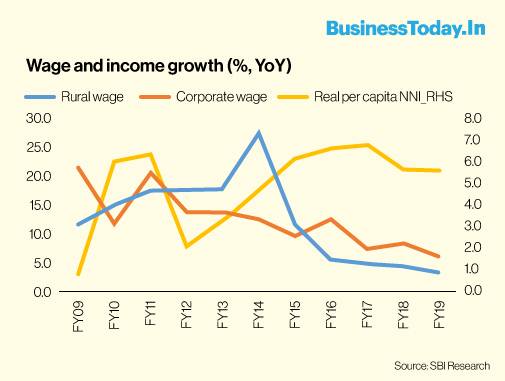

Drastic fall in wages growth, pulling down consumption demand

And this fall in consumer demand can be attributed to a drastic fall in the wages of the working population. The SBI's research shows that both urban and rural wages, which were growing in high double digits until a few years ago, have fallen to single digit, pulling down the real per capita net national income (NNI).

The implications are very clear: Income of the working population needs to be raised through significant increase in urban and rural wages to revive consumer demands - not only for the FMCG goods like biscuits but also consumer durables like autos.

Also Read: FATF Asia-Pacific Group blacklists Pakistan over non-compliance in terror financing

Also Read: Current economic slowdown 'unprecedented', says Niti Aayog's Rajiv Kumar

Also Read: Ravi Shankar Prasad urges FM to cut licence fee, GST for the stressed telecom sector

How much will superstar Vijay’s poll promises cost Tamil Nadu?

How much will superstar Vijay’s poll promises cost Tamil Nadu? Will go with Vijay in Tamil Nadu: Congress makes it clear, says THIS on DMK

Will go with Vijay in Tamil Nadu: Congress makes it clear, says THIS on DMK") KPI Green Energy shares zoom over 11% today — Here is why

KPI Green Energy shares zoom over 11% today — Here is why Election results impact on stock market, focus stocks, rally leader- SMC's Ajay Garg decodes

Election results impact on stock market, focus stocks, rally leader- SMC's Ajay Garg decodes Cognizant to reduce 15,000 jobs; India to face maximum impact

Cognizant to reduce 15,000 jobs; India to face maximum impact China’s Night Tourism Boom: Cultural Shows, Drone Displays Draw Massive Crowds During Holiday

China’s Night Tourism Boom: Cultural Shows, Drone Displays Draw Massive Crowds During Holiday Met Gala 2026: Karan Johar Debuts, Isha Ambani Shines & Ananya Birla’s Mask 'Steels' The Show!

Met Gala 2026: Karan Johar Debuts, Isha Ambani Shines & Ananya Birla’s Mask 'Steels' The Show! Bulldozer At Hogg Market: TMC Office Demolished In Kolkata Amid Post-Poll Violence Tension!

Bulldozer At Hogg Market: TMC Office Demolished In Kolkata Amid Post-Poll Violence Tension! Thalapathy Vijay’s Historic Win: The Fall Of DMK & AIADMK After 50 Years Of Dravidian Rule!

Thalapathy Vijay’s Historic Win: The Fall Of DMK & AIADMK After 50 Years Of Dravidian Rule! Amit Shah’s Bengal Blueprint: How The ‘Modern Chanakya’ Cracked India’s Toughest Political Code!

Amit Shah’s Bengal Blueprint: How The ‘Modern Chanakya’ Cracked India’s Toughest Political Code! Bajaj Finance: Eight days of rally amid Q4 earnings; price targets signal record high breach?

Bajaj Finance: Eight days of rally amid Q4 earnings; price targets signal record high breach? YES Bank shares rise 6% amid heavy volumes; should you buy, sell or hold

YES Bank shares rise 6% amid heavy volumes; should you buy, sell or hold CAMS shares up 20% in a month — 'Buy' call after strong Q4 show, dividend | Target priceKPI Green Energy shares zoom over 11% today — Here is whyElection results impact on stock market, focus stocks, rally leader- SMC's Ajay Garg decodes

CAMS shares up 20% in a month — 'Buy' call after strong Q4 show, dividend | Target priceKPI Green Energy shares zoom over 11% today — Here is whyElection results impact on stock market, focus stocks, rally leader- SMC's Ajay Garg decodes