Higher STT can make equity derivative trading more expensive, pushing some trading activity away from these markets while commodity markets remain tax-neutral.Higher STT can make equity derivative trading more expensive, pushing some trading activity away from these markets while commodity markets remain tax-neutral.

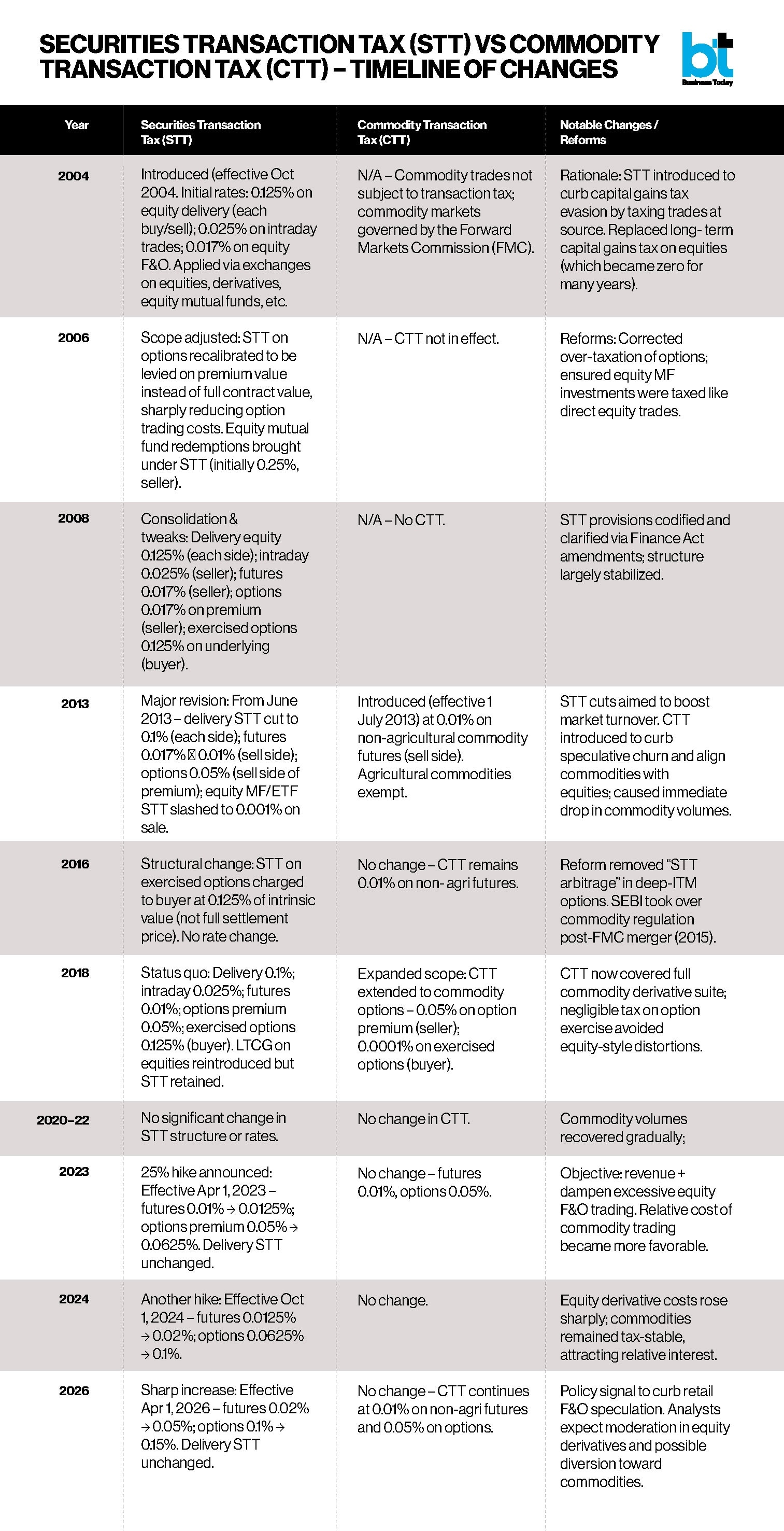

Higher STT can make equity derivative trading more expensive, pushing some trading activity away from these markets while commodity markets remain tax-neutral.Higher STT can make equity derivative trading more expensive, pushing some trading activity away from these markets while commodity markets remain tax-neutral.India’s latest Union Budget took markets by surprise when the government chose to raise Securities Transaction Tax (STT) on equity derivatives while leaving the Commodity Transaction Tax (CTT) untouched, a move that has already sent ripples across trading floors and policy circles. With STT on futures jumping to 0.05 per cent from 0.02 per cent and STT on options premium now 0.15 per cent, the change aims to introduce a “reasonable course correction” in the F&O segment and generate additional revenue. Commodity Transaction Tax (CTT) is applied at 0.01 per cent for futures (on turnover) and 0.05 per cent for options (on premium).

The tax is only applicable to the seller, and on exercised option contracts, the rate is 0.0001 per cent. Hence, CTT is now half of STT. Wherein Commodities derivatives volumes have gone up 1000 per cent plus in less than 3 years on account of low CTT vis-à-vis equity. Does the government want more speculation in commodities?

The apparent reason for this action is the report on the derivative segment by the regulator, which observed that 90–93 per cent of individual F&O traders incur losses, which prompted a correction to create a deterrent effect on “gambling-style" high-frequency trading. This is likely to generate tax revenue of ₹73,700 crore for the next fiscal year.

Yet, by not re-examining CTT alongside STT, the Budget has created an uneven playing field that risks distorting incentives in the markets that serve overlapping risk-management functions. The jump in STT rates, futures up 150 per cent and options up 50 per cent will increase transaction costs for traders using derivatives to hedge or speculate.

Futures traders, for instance, will now pay more than double the previous STT on each transaction, while options traders face a significant increase in levy on premiums and exercised contracts. Commodity markets, by contrast, continue to operate under the existing CTT regime with no changes. That tax symmetry, or lack of it, matters because both equity and commodity derivatives contribute to price discovery and risk transfer, and are increasingly used by institutional participants who straddle both arenas.

This high cost per trade discourages frequent traders, especially retail investors who dominate options trading. An immediate sell-off was observed with indices going southwards after the announcement. Mid-cap and small-cap indices dropped 4 per cent in two days, reflecting investor caution and liquidity concerns. What is being ignored is consequentially it will reduce genuine hedging and participation.

An emerging trend is already visible in recent bouts of sharp price swings in gold and silver, where heightened global uncertainty and speculative positioning have driven elevated short- term volatility. In such an environment, any tax asymmetry that nudges speculative flows into commodity derivatives risks due to no increase in CTT magnifying speculative activity in commodity markets meant primarily for hedging.

Foreign Portfolio Investors (FPIs) will find the Indian derivative market less attractive compared to global markets with lower transaction costs, which may lead to migration of liquidity to offshore markets. The most vital issue is the reduction of hedging efficiency, resulting in higher costs to Corporates and institutions to manage risk.

The policy inconsistency becomes clearer against the backdrop of how these two markets function. Commodity derivatives are deeply tied to real-economy needs like hedging against price risk in agricultural commodities, metals and energy. They serve exporters, importers, processors and producers whose businesses depend on predictable costs. CTT, in its stable form, allows these actors to manage exposure without sudden tax frictions.

Equity derivatives, on the other hand, are more heavily traded by financial institutions and retail participants, often in strategies that seek short-term gains. The government’s decision to leave CTT untouched suggests a disconnect in how it views the economic role of each market, despite its structural importance.

Moreover, liquidity dynamics risk being distorted. Higher STT can make equity derivative trading more expensive, pushing some trading activity away from these markets while commodity markets remain tax-neutral. Over time, this may reduce cross-market arbitrage, weaken price discovery and shrink overall derivatives participation outcomes that do not align with broader goals of deep, resilient financial markets. Apart from that it will impact brokers and exchanges dependent on high turnover.

From a policy perspective, aligning STT and CTT reforms would have signalled coherence. If the objective is to curb excessive speculation, reduce systemic risk, and ensure sustainable participation, then a coordinated review of transaction taxes across asset classes is essential. Looking in isolation may not fully reflect the intended approach and could skew capital flows in ways that neither aid retail protection nor support efficient hedging.

This is not simply about levying more or less tax in isolation. It is about designing a tax framework that recognizes how markets interact, and how cost signals shape participant behaviour. A Budget that targets only one leg of the derivatives ecosystem while ignoring the other is a missed opportunity.

A post-Budget review that places STT and CTT on the same analytical footing, examining the economic roles of each market and calibrating transaction costs accordingly, would make for better policy. It would uphold market parity, encourage genuine hedging, and support deeper, more consistent risk-pricing across India’s financial markets.

(Uday Tardalkar is Guest Faculty at National Institute of Securities Markets (NISM). Views are personal)

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K crore 'You're in the wrong chair': When Gita Gopinath faced bias as IMF chief economist

'You're in the wrong chair': When Gita Gopinath faced bias as IMF chief economist Can India monetise microdramas as the market booms but profitability remains elusive?

Can India monetise microdramas as the market booms but profitability remains elusive? India needs its own DeepSeek to avoid AI dependence, warns Bernstein

India needs its own DeepSeek to avoid AI dependence, warns Bernstein.") Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock WatchInfosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K croreLast chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock WatchInfosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K croreLast chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure  JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential

JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet

Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet