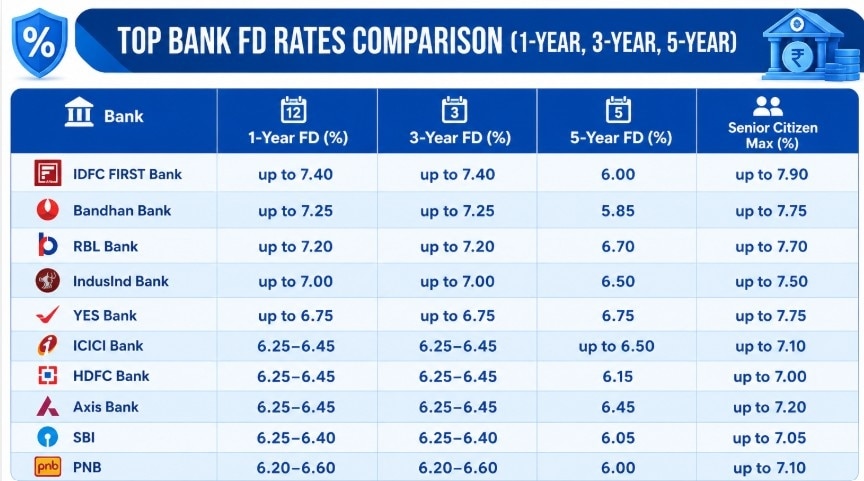

For short-term investors prioritising liquidity, 1-year FDs offer a balance between accessibility and returns. Among leading banks, interest rates for the general public largely range between 6.20% and 7.40%.For short-term investors prioritising liquidity, 1-year FDs offer a balance between accessibility and returns. Among leading banks, interest rates for the general public largely range between 6.20% and 7.40%.

For short-term investors prioritising liquidity, 1-year FDs offer a balance between accessibility and returns. Among leading banks, interest rates for the general public largely range between 6.20% and 7.40%.For short-term investors prioritising liquidity, 1-year FDs offer a balance between accessibility and returns. Among leading banks, interest rates for the general public largely range between 6.20% and 7.40%.Fixed deposits (FDs) continue to remain a cornerstone of conservative investment strategies, particularly for investors seeking predictable returns and capital protection. In the current interest rate environment, banks — especially private sector and small finance banks — are offering competitive rates across tenures, with the most attractive bands typically seen in the 1-year to 3-year segment. A tenure-wise evaluation provides better clarity on where investors can optimise returns.

1-year tenure

For short-term investors prioritising liquidity, 1-year FDs offer a balance between accessibility and returns. Among leading banks, interest rates for the general public largely range between 6.20% and 7.40%, while senior citizens can earn between 6.70% and 7.90%.

Banks such as IDFC FIRST Bank (up to 7.40%), Bandhan Bank (up to 7.25%), and RBL Bank (up to 7.20%) are offering the highest yields in this segment. Large private banks like HDFC Bank, ICICI Bank, and Axis Bank are offering slightly lower but stable returns in the 6.25%–6.45% range. Public sector banks such as SBI and Bank of Baroda remain in the 6.10%–6.40% band, reflecting a more conservative rate structure.

This tenure is suitable for investors parking surplus funds temporarily or those expecting interest rate changes in the near term.

MUST READ: FD rates: Senior Citizens turn to fixed deposits in May 2026 amid market volatility

3-year tenure

The 3-year FD segment is currently one of the most attractive in terms of risk-reward balance. Interest rates here are broadly aligned with 1-year deposits but often offer slightly better compounding benefits.

Top-performing banks include IDFC FIRST Bank (up to 7.40%), IndusInd Bank (up to 7.00%), RBL Bank (up to 7.20%), and Bandhan Bank (up to 7.25%). Senior citizens can earn close to 7.50%–7.90% in select banks.

Large banks continue to offer rates in the 6.25%–6.70% range, while PSU banks remain clustered around 6.20%–6.60%.

A 3-year tenure is often preferred by investors seeking moderate-term stability without locking funds for very long durations. It also helps in capturing relatively higher rates before any potential rate cycle reversal.

MUST READ: Tax-Saving FDs vs regular FDs: Where should you invest in May 2026?

5-year tenure

Long-term FDs (5 years and above) are typically chosen for stability and tax-saving purposes (in specific schemes). However, interest rates in this segment are slightly lower compared to shorter tenures, reflecting the current yield curve.

For general investors, rates range between 5.85% and 6.75%, while senior citizens can earn between 6.50% and 7.50%.

Among banks, YES Bank (up to 6.75%), RBL Bank (up to 6.70%), and ICICI Bank (up to 6.50%) offer relatively better returns. Public sector banks such as SBI (6.05%) and PNB (6.00%) remain on the lower end, while Bandhan Bank (5.85%) reflects a softer long-term rate structure.

Despite slightly lower rates, 5-year FDs appeal to investors seeking long-term certainty, especially those aligning investments with financial goals or tax-saving needs.

DON'T MISS: Fixed deposits vs equity: Where should investors park money during oil shock?

Key takeaways for investors

Overall, while FD rates remain stable, the optimal strategy lies in laddering investments across tenures to balance liquidity, returns, and interest rate risk.

Asia takes lead: Hong Kong overtakes Switzerland as world’s largest wealth hub

Asia takes lead: Hong Kong overtakes Switzerland as world’s largest wealth hub What is IndiGo’s five-step strategy to manage operational losses?

What is IndiGo’s five-step strategy to manage operational losses? ") ITC shares: A risk or reward for investors? Stock at 52-week low

ITC shares: A risk or reward for investors? Stock at 52-week low") PM Modi's appeal working? Gold demand drops 70% after duty hike, rising costs

PM Modi's appeal working? Gold demand drops 70% after duty hike, rising costs Student flagged flaws. Now CBSE says experts from govt and IITs are securing its systems

Student flagged flaws. Now CBSE says experts from govt and IITs are securing its systems EPFO Interest Credit Delay Explained: When Will PF Interest Be Credited? Full Update 2026

EPFO Interest Credit Delay Explained: When Will PF Interest Be Credited? Full Update 2026 Cummins India Reveals Biggest Growth Drivers Behind Its Strong Rally

Cummins India Reveals Biggest Growth Drivers Behind Its Strong Rally AI, Chips & Global Chaos: Why Foreign Investors Are Selling India? Amit Goel Explains

AI, Chips & Global Chaos: Why Foreign Investors Are Selling India? Amit Goel Explains “Whole Of Govt Approach!” Dharmendra Pradhan Details Foolproof Re-NEET Prep With Sweta Singh

“Whole Of Govt Approach!” Dharmendra Pradhan Details Foolproof Re-NEET Prep With Sweta Singh Unboxing Apple AirPods Max 2: New H2 Chip, Enhanced ANC, Best Over-The-Ear Headphones?ITC shares: A risk or reward for investors? Stock at 52-week low

Unboxing Apple AirPods Max 2: New H2 Chip, Enhanced ANC, Best Over-The-Ear Headphones?ITC shares: A risk or reward for investors? Stock at 52-week low Suzlon shares: From Rs 1.58 to Rs 58 — A must-have energy stock for your portfolio? Experts decode

Suzlon shares: From Rs 1.58 to Rs 58 — A must-have energy stock for your portfolio? Experts decode Auto stocks to buy with up to 47% potential upside, ahead of May auto sales data

Auto stocks to buy with up to 47% potential upside, ahead of May auto sales data Vedanta shares post-demerger uptrend still intact? Will stock outperform again?

Vedanta shares post-demerger uptrend still intact? Will stock outperform again? Sensex, Nifty outlook for Monday, June 1: What to expect from stock market? Key levels, strategy

Sensex, Nifty outlook for Monday, June 1: What to expect from stock market? Key levels, strategy