CA Kaushik claimed that if the same Rs 80 lakh had been invested in a Nifty 50 index fund in 2015, it could have grown to over Rs 2.2 crore by 2026, outperforming the apartment investment.CA Kaushik claimed that if the same Rs 80 lakh had been invested in a Nifty 50 index fund in 2015, it could have grown to over Rs 2.2 crore by 2026, outperforming the apartment investment.

CA Kaushik claimed that if the same Rs 80 lakh had been invested in a Nifty 50 index fund in 2015, it could have grown to over Rs 2.2 crore by 2026, outperforming the apartment investment.CA Kaushik claimed that if the same Rs 80 lakh had been invested in a Nifty 50 index fund in 2015, it could have grown to over Rs 2.2 crore by 2026, outperforming the apartment investment.A social media thread by CA Nitin Kaushik has reignited the debate around whether buying a home in India is truly a wealth-creating investment or simply an emotional purchase disguised as an asset.

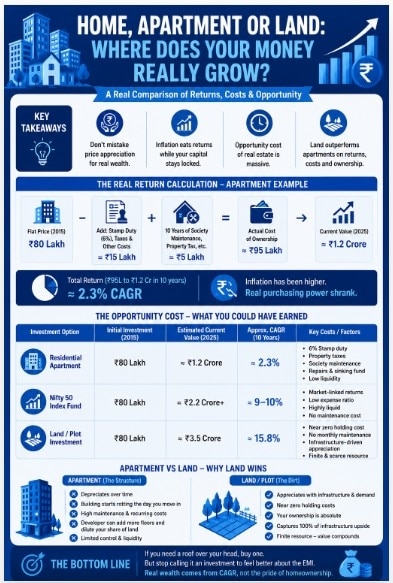

In a detailed post on X, Kaushik argued that many homeowners overestimate the actual returns generated from residential apartments after accounting for hidden costs such as stamp duty, maintenance charges, property taxes and inflation.

“Your home is a liquidity trap disguised as an asset,” Kaushik wrote, adding that many people mistake nominal price appreciation for real wealth creation.

The real return calculation

Kaushik explained the concept using a hypothetical example of a flat purchased for Rs 80 lakh in 2015 that is currently valued at around Rs 1.2 crore.

According to him, once additional costs such as 6% stamp duty, society maintenance expenses and annual property taxes are included, the effective acquisition and holding cost rises closer to Rs 95 lakh.

He argued that the increase from Rs 95 lakh to Rs 1.2 crore over a decade translates into an annualised return of only around 2.3%, which is lower than long-term inflation in India.

“In real terms, your purchasing power actually shrank,” he noted, suggesting that homeowners may feel wealthier on paper while failing to generate meaningful inflation-adjusted returns.

MUST READ: Should you take a home loan in a high-interest economy?

MUST READ: New tax rules 2026: What it means for your house buying plans, portfolio allocation

Equity markets

The thread also compared residential property returns with equity market performance over the same period.

Kaushik claimed that if the same Rs 80 lakh had been invested in a Nifty 50 index fund in 2015, the investment could have grown to over Rs 2.2 crore by 2026, significantly outperforming the apartment investment.

He described the difference as the “opportunity cost” of locking capital into residential real estate with limited liquidity and recurring expenses.

The comments have resonated strongly online, particularly among younger investors increasingly favouring equity mutual funds, index investing and financial assets over traditional property ownership.

Apartments vs land

Kaushik further argued that apartments behave like depreciating assets because buildings deteriorate over time and require continuous spending on repairs, maintenance and upgrades.

“The building starts rotting the day you move in,” he wrote, claiming that investors are effectively paying for “dead square footage” that steadily loses value.

Instead, he advocated investing in land parcels located in emerging growth corridors, citing lower holding costs and stronger long-term appreciation potential.

According to his example, a plot bought for Rs 80 lakh and later valued at Rs 3.5 crore would generate a compounded annual growth rate (CAGR) of around 15.8%.

He also pointed out that land ownership remains finite and cannot be diluted, unlike apartment projects where developers may add additional floors or towers over time.

MUST READ: Buying a house with your spouse? Here’s how it can reduce your tax bill

Emotional value

Despite his criticism of residential apartments as investments, Kaushik clarified that buying a home for self-use is entirely valid.

“If you need a roof over your head, buy one,” he said, while cautioning people against justifying large EMIs by assuming automatic wealth creation.

The viral discussion has once again highlighted the changing mindset among urban Indian investors, many of whom are increasingly evaluating assets based on liquidity, inflation-adjusted returns and long-term CAGR rather than traditional notions of homeownership.

MUST READ: Are you hurting your credit score despite paying EMIs on time?

Meta, Oracle layoffs: Indian H-1B workers in US have 60 days to find a job or leave; Here's why

Meta, Oracle layoffs: Indian H-1B workers in US have 60 days to find a job or leave; Here's why ‘Deal can happen in 5 seconds if…’: Jefferies on what it will take for Trump to end Iran war

‘Deal can happen in 5 seconds if…’: Jefferies on what it will take for Trump to end Iran war BT Exclusive: We are providing infra to people coming to work from the beach, says Goa CM Pramod Sawant

BT Exclusive: We are providing infra to people coming to work from the beach, says Goa CM Pramod Sawant This country is India’s third largest crude oil supplier, ahead of Saudi Arabia, US

This country is India’s third largest crude oil supplier, ahead of Saudi Arabia, US L&T CMD S N Subrahmanyan, who vouched for 90-hour work week, enters ₹100 crore club

L&T CMD S N Subrahmanyan, who vouched for 90-hour work week, enters ₹100 crore club Pakistan’s China-Made JF-17 Faces Scrutiny After Crash During Routine Training Mission

Pakistan’s China-Made JF-17 Faces Scrutiny After Crash During Routine Training Mission Europe Blinked First? Putin Gains Big As UK, EU Quietly Return To Russian Oil Dependence

Europe Blinked First? Putin Gains Big As UK, EU Quietly Return To Russian Oil Dependence Rubio’s India Visit Revives Big Questions Over Quad’s Momentum And Strategic Future

Rubio’s India Visit Revives Big Questions Over Quad’s Momentum And Strategic Future Walmart Warns On U.S. Economy As Fuel Prices Hurt Consumer Spending | Rising Fuel Costs Impact

Walmart Warns On U.S. Economy As Fuel Prices Hurt Consumer Spending | Rising Fuel Costs Impact Trump Vs Netanyahu: Tense Leak Reveals Massive Fight Over Iran War Ceasefire Deal!

Trump Vs Netanyahu: Tense Leak Reveals Massive Fight Over Iran War Ceasefire Deal! 'Unchecked FX depreciation...': What Radhika Rao says on rupee, RBI intervention

'Unchecked FX depreciation...': What Radhika Rao says on rupee, RBI intervention Dixon, Elecon, JSW Infra, Kaynes Technology shares rise up to 7% amid market rally today

Dixon, Elecon, JSW Infra, Kaynes Technology shares rise up to 7% amid market rally today MTAR Technologies shares hit record high; multibagger stock up 57% in a month; check latest trigger‘Deal can happen in 5 seconds if…’: Jefferies on what it will take for Trump to end Iran war

MTAR Technologies shares hit record high; multibagger stock up 57% in a month; check latest trigger‘Deal can happen in 5 seconds if…’: Jefferies on what it will take for Trump to end Iran war This Ashish Kacholia stock tanked 36% in two weeks; what is behind this correction?

This Ashish Kacholia stock tanked 36% in two weeks; what is behind this correction?