The cumulative 125 bps reduction significantly lowered borrowing costs across the banking system, particularly for floating-rate loans linked to external benchmarks like the repo rate.

The cumulative 125 bps reduction significantly lowered borrowing costs across the banking system, particularly for floating-rate loans linked to external benchmarks like the repo rate. The cumulative 125 bps reduction significantly lowered borrowing costs across the banking system, particularly for floating-rate loans linked to external benchmarks like the repo rate.

The cumulative 125 bps reduction significantly lowered borrowing costs across the banking system, particularly for floating-rate loans linked to external benchmarks like the repo rate.The upcoming RBI Monetary Policy Committee (MPC) meeting, scheduled for April 6–8, 2026, comes at a delicate juncture for the Indian economy. In its February meeting, the MPC retained the policy repo rate at 5.25 percent and maintained a neutral stance, even as inflation remained broadly aligned with the medium-term target and growth indicators stayed resilient.

The central bank in February 2026 decided to leave the repo rate unchanged at 5.25%, signalling a pause after an aggressive rate-cut cycle in 2025. For borrowers with floating-rate home loans, the message is clear: EMIs are unlikely to fall further for now but the good thing is that the risk of a sudden increase also looks limited.

How RBI cut rates through 2025

Between February and December 2025, the RBI cut the repo rate by a cumulative 125 basis points, bringing it down from 6.50% to 5.25% to support economic growth.

The easing cycle unfolded as follows:

February 2025: Repo rate cut by 25 bps to 6.25%

April 2025: Another 25 bps cut to 6.00%

June 2025: A sharper 50 bps cut to 5.50%

August and October 2025: Rates held steady

December 2025: Final 25 bps cut to 5.25%

February 2026: Rates held steady at 5.25%

ALSO READ: Govt retains inflation target at 4% with 2–6% band for next five years

Real EMI impact

Data from the table highlights the tangible savings borrowers have already seen due to this rate cycle.

For a ₹50 lakh home loan (20-year tenure):

At 8.5% interest: EMI ~₹43,391

At 7.25% interest: EMI ~₹39,519

Monthly savings: ~₹3,000–₹3,800

Total interest saved: ~₹7.3 lakh over the loan tenure

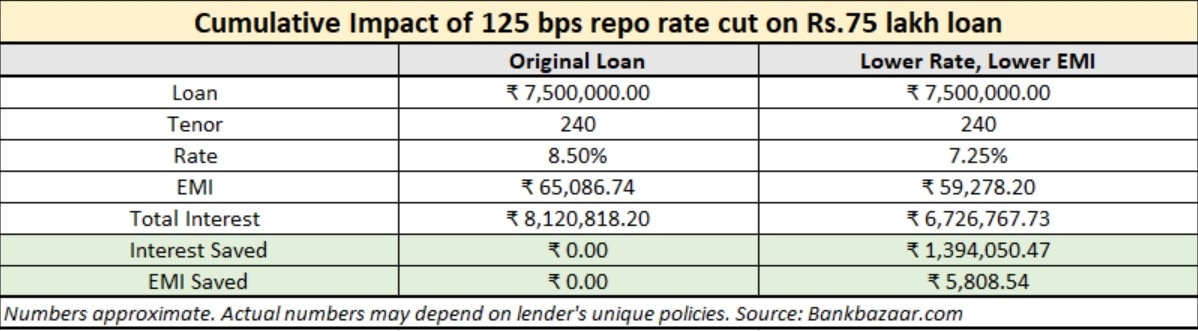

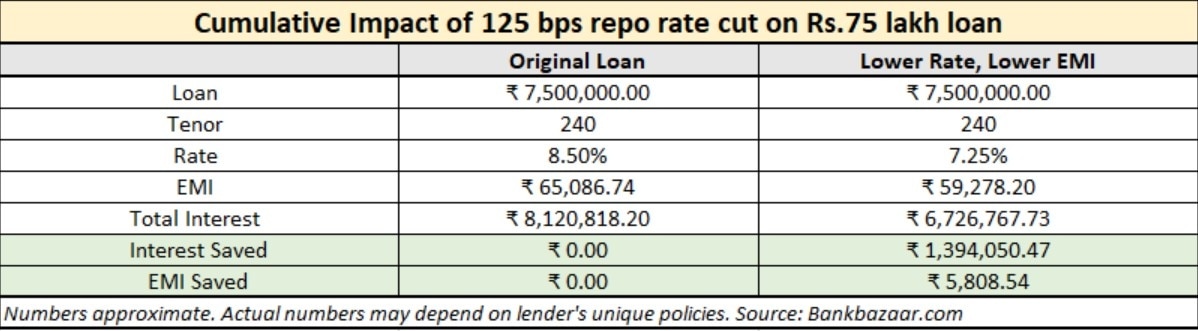

For a ₹75 lakh home loan (20-year tenure):

At 8.5% interest: EMI ~₹65,087

At 7.25% interest: EMI ~₹59,278

Monthly savings: ~₹5,800

Total interest saved: ~₹13.9 lakh

These figures illustrate a critical point: even a 100–125 bps reduction in interest rates has a disproportionately large impact on long-tenure loans like home financing. Borrowers benefit not just through lower EMIs, but also through a substantial reduction in lifetime interest outgo.

ALSO READ: Relying only on bank fixed deposits? You may be missing safer options with higher returns

Why borrowers felt the benefit quickly

Most home loans today are linked to external benchmarks such as EBLR or MCLR, which ensured faster transmission of RBI’s rate cuts. As lending rates fell, borrowers benefited in two key ways—lower monthly EMIs or shorter loan tenures, both of which reduced the total interest paid over time.

For many households, the savings helped cushion the impact of high living costs and inflation.

Where rates stand now

As of early 2026, lending rates have broadly stabilised:

Public sector banks: ~7.15%–7.30%

Private banks: ~7.75%–9.00%

Public sector lenders remain more competitive, while private banks continue to price in a premium based on credit profiles and margins.

What to expect from the April MPC meeting

With inflation largely aligned with the RBI’s 4% target and growth holding steady, the central bank has shifted to a “pause” mode. The February 2026 policy signalled a neutral stance, indicating that the aggressive easing phase may be over for now.

For borrowers, this translates into:

Limited scope for further EMI reduction in the near term

Stability in borrowing costs

Lower risk of sharp rate hikes unless inflation resurfaces

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls Same 43°C temperature, different reality: Why Europe's heatwave is more deadly than India's

Same 43°C temperature, different reality: Why Europe's heatwave is more deadly than India's 'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means

'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore

From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery

Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure