Experts stress that savings accounts are ideal for emergency funds and day-to-day liquidity, but they may not be the most efficient place for money that is unlikely to be used for several years.

Experts stress that savings accounts are ideal for emergency funds and day-to-day liquidity, but they may not be the most efficient place for money that is unlikely to be used for several years.Leaving money in a bank savings account may feel like the safest choice, but financial planners say excessive caution can come at a price. CA Nitin Kaushik highlighted a recent case involving an investor who parked ₹50 lakh in a savings account for three years illustrates how the pursuit of safety can result in significant opportunity costs.

When 'safe' money loses value

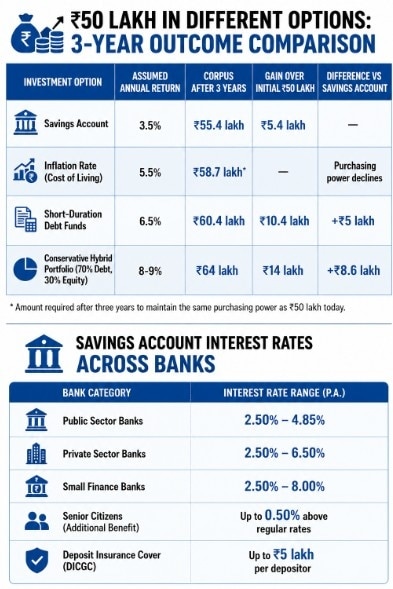

According to the planner, the client kept the money in a standard savings account because it felt risk-free. Assuming an interest rate of around 3.5% per annum, the corpus grew to approximately ₹55.4 lakh over three years, generating gains of about ₹5.4 lakh.

However, with inflation averaging around 5.5% during the period, the real purchasing power of the money declined. In effect, the investor's wealth failed to keep pace with rising costs.

"If your money grows at a slower pace than inflation, you're losing purchasing power even if your account balance is increasing," Kaushik said.

The ₹8.6 lakh opportunity cost

The opportunity cost becomes more evident when compared with alternative investments.

Short-duration debt funds, which are considered relatively low-risk instruments, delivered average returns of around 6.5% during the same period. Had the ₹50 lakh been invested in such products, the corpus could have grown to roughly ₹60.4 lakh.

A conservative portfolio consisting of 70% debt and 30% equity would have delivered annual returns of 8-9%, taking the corpus to around ₹64 lakh. Compared with the ₹55.4 lakh accumulated in the savings account, the difference amounts to nearly ₹8.6 lakh.

The case highlights a common misconception among savers who equate safety with keeping large sums idle in low-yield accounts.

MUST READ: Gold is no longer just a reserve asset; central banks are managing it like a portfolio: Report

Why savings accounts remain popular

Savings accounts continue to be among the most preferred financial products in India because of their high liquidity, easy accessibility and deposit safety.

Interest rates currently range from 2.5% to 8% per annum, depending on the bank and account balance. Senior citizens typically receive an additional 0.5 percentage point over regular rates. Deposits of up to ₹5 lakh are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC).

Savings accounts also offer unrestricted deposits and withdrawals and provide access to UPI, NEFT, RTGS, IMPS, net banking and debit card facilities.

Which banks offer higher rates?

Public sector banks such as State Bank of India, Punjab National Bank and Canara Bank generally offer savings account interest rates ranging from 2.5% to 4.85%.

Private lenders including ICICI Bank, HDFC Bank and Axis Bank offer around 2.5%, while banks such as IDFC First Bank and RBL Bank provide rates of up to 6.5% and 5.64%, respectively.

Among small finance banks, Utkarsh Small Finance Bank and ESAF Small Finance Bank offer up to 8%, while Suryoday Small Finance Bank offers as much as 7.75%.

MUST READ: Fixed deposits: Company FDs offer rates up to 9.1%, outpacing bank deposits but with higher risks

Safety and growth need not be opposites

Experts stress that savings accounts are ideal for emergency funds and day-to-day liquidity, but they may not be the most efficient place for money that is unlikely to be used for several years.

"Risk management is not about avoiding markets altogether. It is about matching your investment horizon with the appropriate asset class," Kaushik said.

While returns from debt funds and hybrid portfolios are not guaranteed, advisers say investors should also account for a less visible threat—the cost of doing nothing. For long-term idle money, opportunity cost can be just as damaging as market risk.

MUST READ: As gold loses lustre, silver and lab-grown diamonds drive new growth

Gautam Adani tops Hurun real estate rich list, overtaking DLF's Rajiv Singh

Gautam Adani tops Hurun real estate rich list, overtaking DLF's Rajiv Singh Rupee falls 57 paise to 96.20 against dollar; further weakness likely, say analysts

Rupee falls 57 paise to 96.20 against dollar; further weakness likely, say analysts SC slaps ₹3 lakh fine on Samay Raina, says taken the court for a ride and has brazenly violated the orders

SC slaps ₹3 lakh fine on Samay Raina, says taken the court for a ride and has brazenly violated the orders Mahadev betting app case: ED arrests EBIX Chairman Vikas Garg

Mahadev betting app case: ED arrests EBIX Chairman Vikas Garg Census 2027 SIR guide: How to register, submit details and get your SE ID

Census 2027 SIR guide: How to register, submit details and get your SE ID Is India Prepared For An Oil Shock? Expert Explains Supply Risks Amid West Asia Conflict

Is India Prepared For An Oil Shock? Expert Explains Supply Risks Amid West Asia Conflict Why Coforge Could Outperform The Market Over The Next 12–24 Months | Rakesh Vyas Explains

Why Coforge Could Outperform The Market Over The Next 12–24 Months | Rakesh Vyas Explains War In West Asia: What It Means For India's Oil Supply, Fuel Prices & Economy

War In West Asia: What It Means For India's Oil Supply, Fuel Prices & Economy “Pakistani Cricket Team Brought Drugs To India”: RVS Mani’s Explosive Claim Sparks Row

“Pakistani Cricket Team Brought Drugs To India”: RVS Mani’s Explosive Claim Sparks Row Indian I.T. Stocks Outlook: Why Midcap And Smallcap I.T. Could Lead The AI Comeback

Indian I.T. Stocks Outlook: Why Midcap And Smallcap I.T. Could Lead The AI Comeback Sensex falls 561 pts as crude oil price boils, rupee sinks; what's next for investors? Rupee falls 57 paise to 96.20 against dollar; further weakness likely, say analysts

Sensex falls 561 pts as crude oil price boils, rupee sinks; what's next for investors? Rupee falls 57 paise to 96.20 against dollar; further weakness likely, say analysts Is Swiggy the next Eternal? Quest PMS' Vyas reveals portfolio view after stock correction

Is Swiggy the next Eternal? Quest PMS' Vyas reveals portfolio view after stock correction Brent crude rally revives pressure on paint, tyre and aviation stocks; should investors be worried?

Brent crude rally revives pressure on paint, tyre and aviation stocks; should investors be worried? Suzlon, BHEL, Adani Power, Waaree, Adani Green, Tata Power: Check fresh ratings & targets

Suzlon, BHEL, Adani Power, Waaree, Adani Green, Tata Power: Check fresh ratings & targets