A ₹10 lakh loan with FD arbitrage may look attractive, but it significantly increases your EMI burden and risk.

A ₹10 lakh loan with FD arbitrage may look attractive, but it significantly increases your EMI burden and risk. A ₹10 lakh loan with FD arbitrage may look attractive, but it significantly increases your EMI burden and risk.

A ₹10 lakh loan with FD arbitrage may look attractive, but it significantly increases your EMI burden and risk.I’m planning to buy a car priced around ₹14 lakh and need advice on the most sensible loan structure. My in-hand salary is ₹64,000 per month, with an additional ₹30,000 invested monthly through an ESPP. I currently have ₹10 lakh available—₹6 lakh in fixed deposits and ₹4 lakh in savings. My CIBIL score is 780, and Union Bank has offered a car loan at 7.70%.

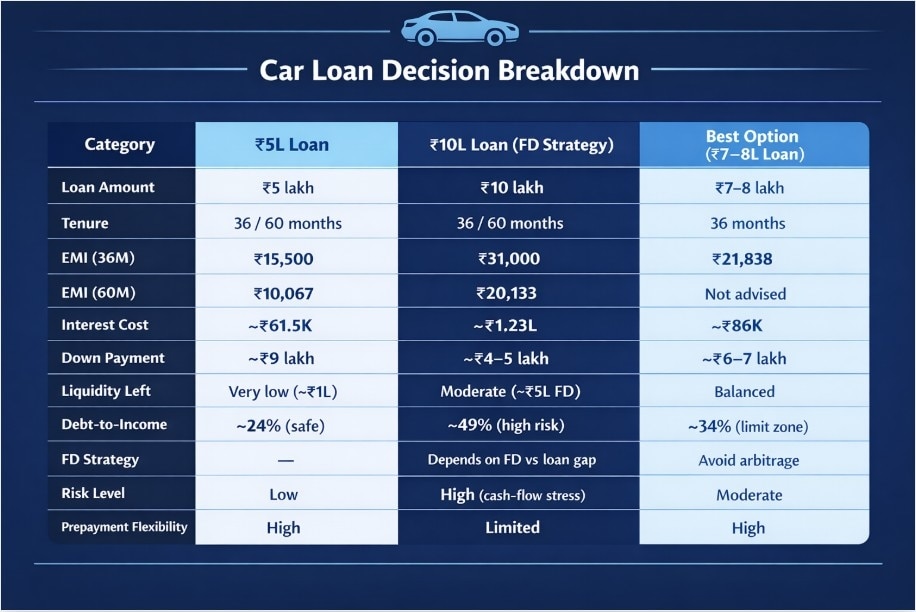

Initially, I planned to take a ₹5 lakh loan and pay the rest as down payment. However, the bank manager suggested taking a ₹10 lakh loan, keeping ₹5 lakh in FD, and using the FD interest to offset loan costs. For a ₹10 lakh loan, the EMI is ₹31,000 (36 months) or ₹20,133 (60 months). For a ₹5 lakh loan, the EMI is ₹15,500 (36 months) or ₹10,067 (60 months).

I intend to close the loan within 2–3 years. Which approach makes more sense: a lower loan with higher down payment, or a higher loan with FD arbitrage? Are partial prepayments a better alternative?

Advice by Dev Patel, Quantitative Research Analyst at 1 Finance

The bank manager's advice looks like a sales tactic. While the arbitrage idea draws well on paper, it ignores risk and taxes. The FD earns on the full ₹5 lakh for 3 years, while the loan charges interest on a reduced balance. But to earn a minimal amount of net interest, you are doubling your EMI from ₹15,500 to ₹31,200. With your ₹64,000 in-hand salary, this pushes your Debt-to-Income ratio from a comfortable 24% to a completely unsustainable 49%. One bad month or unexpected expense, and that EMI becomes a cash-flow crisis. Meanwhile, the bank collects ₹1.23 lakh in interest instead of ₹61,500. The manager's incentive is clear. Furthermore, your post-tax FD return is much lower than the 7.70% loan cost.

MUST READ: How much home loan EMI you are saving now since RBI's last rate cut

However, the ₹5 lakh loan approach has flaws too. Making a ₹9 lakh down payment from your ₹10 lakh corpus leaves you with just ₹1 lakh for emergencies, which is dangerously low. A middle way is to borrow ₹7-8 lakh for a 36-month tenure. For a ₹7 lakh loan, your EMI will be ₹21,838.

This ensures the debt is cleared in exactly three years while capping your total interest at roughly ₹86,000. Keep in mind that a Debt-to-Income ratio of 34% is right at the edge of the recommended limit; borrowing anything more than this will result in an unsustainable EMI. Please consult a qualified financial advisor to look at the full picture to make an informed decision.

MUST READ: PPF investment rule FY27: How depositing funds before the 5th every month can maximise your returns

What investors should note

A ₹10 lakh loan with FD arbitrage may look attractive, but it significantly increases your EMI burden and risk. With a ₹64,000 salary, doubling EMI pushes your debt-to-income ratio to unsafe levels, while post-tax FD returns are unlikely to beat the 7.70% loan cost. On the other hand, a ₹5 lakh loan preserves affordability but leaves you with very low emergency savings. A balanced approach—borrowing ₹7–8 lakh for 3 years—offers the best mix of manageable EMI, adequate liquidity, and controlled interest outgo. You can further optimize by making partial prepayments using bonuses or ESPP gains.

Kotak Bank shares: MD and CEO Ashok Vaswani to step down; Saha looks best placed, says Nomura; target price

Kotak Bank shares: MD and CEO Ashok Vaswani to step down; Saha looks best placed, says Nomura; target price Aastha Spintex IPO opens today: Should you apply? Check price band, GMP, reviews & more

Aastha Spintex IPO opens today: Should you apply? Check price band, GMP, reviews & more 'Come forward and help us': Ketan's father appeals to witnesses present at Lohagad on day of murder

'Come forward and help us': Ketan's father appeals to witnesses present at Lohagad on day of murder YRF's next big drama could be mobile-only: Why the film company is betting on a new format

YRF's next big drama could be mobile-only: Why the film company is betting on a new format HDFC Bank likely to reappoint Sashidhar Jagdishan as CEO for a third term: Report

HDFC Bank likely to reappoint Sashidhar Jagdishan as CEO for a third term: Report HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Netweb Technologies shares crash 8% despite fundraising plan

Netweb Technologies shares crash 8% despite fundraising plan  Hexaware Technologies shares gain 8% in early deals; here's why

Hexaware Technologies shares gain 8% in early deals; here's why  Persistent Systems–Nagarro deal: Key questions answered

Persistent Systems–Nagarro deal: Key questions answered Turtlemint Fintech Solutions make a weak stock market debut; shares lists at 11% discount

Turtlemint Fintech Solutions make a weak stock market debut; shares lists at 11% discount Persistent Systems shares dive 9% to hit 52-week low; here's why

Persistent Systems shares dive 9% to hit 52-week low; here's why