Premature redemption refers to exiting a Sovereign Gold Bond before its full 8-year maturity period, as permitted under RBI rules.Premature redemption refers to exiting a Sovereign Gold Bond before its full 8-year maturity period, as permitted under RBI rules.

Premature redemption refers to exiting a Sovereign Gold Bond before its full 8-year maturity period, as permitted under RBI rules.Premature redemption refers to exiting a Sovereign Gold Bond before its full 8-year maturity period, as permitted under RBI rules.Investors in Sovereign Gold Bond (SGB) 2019–20 Series V are sitting on exceptional gains, with the Reserve Bank of India (RBI) announcing a premature redemption price that translates into nearly 302% absolute returns over about 6.5 years.

The tranche, originally issued on October 15, 2019, has now become eligible for early exit, offering a lucrative opportunity for investors to book profits amid elevated gold prices.

302% returns

The RBI has fixed the premature redemption price at ₹15,009 per unit, based on the average closing price of 999 purity gold for three working days—April 9, April 10, and April 13, 2026.

At the time of issuance, the bond was priced at:

> ₹3,738 per gram for online investors

> ₹3,788 per gram for offline investors

This implies:

> Absolute gain: ₹11,271 per unit

> Return: ~301.5% (≈302%), excluding interest income

But the bigger question remains: should you redeem now or hold till maturity?

Premature redemption vs final maturity

While the ~302% return makes early exit attractive, the decision hinges on taxation, future return potential, and investment horizon.

Premature redemption (after 5 years)

Allowed on interest payment dates via RBI

Current redemption price: ₹15,009 per gram

Gains are taxable (post April 1, 2026)

Suitable for:

Profit booking after sharp rallies

Liquidity needs

Portfolio rebalancing

Final redemption (after 8 years)

Redemption linked to prevailing gold prices

Capital gains are fully tax-free

Investors continue earning 2.5% annual interest

Ideal for:

Long-term investors

Tax-efficient wealth creation

Strategic gold allocation

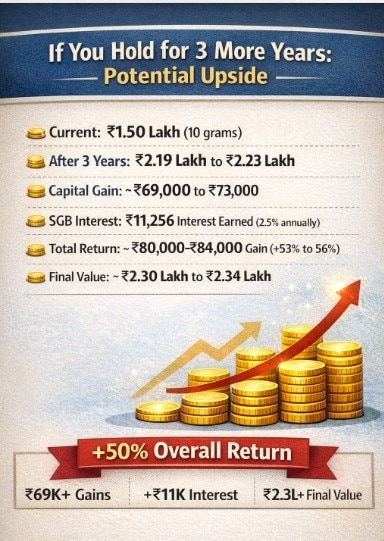

If you hold for 3 more years: Potential upside

If investors choose to stay invested till maturity, the return profile remains compelling.

Assuming gold delivers its historical 13.5%–14.1% CAGR in INR:

Base value (10 grams)

Current value: ~₹1.50 lakh

After 3 years

Expected value: ₹2.19 lakh to ₹2.23 lakh

Capital gains: ₹69,000 to ₹73,000

Return: ~46% to 49%

Add SGB interest (2.5% annually)

Total interest earned: ~₹11,256

Total return outlook (including interest)

Total gain: ₹80,000 to ₹84,000

Final value: ₹2.30 lakh to ₹2.34 lakh

Total return: ~53% to 56%

The trade-off

Exit now: Lock in ~302% gains, but pay tax

Hold till maturity: Potential upside + tax-free gains + steady interest

For disciplined investors, this becomes a tax vs timing decision, not just a return decision.

ALSO READ: ‘Secondary market for SGBs is no longer a tax haven’: CA flags important rule shift from April 1

What is premature redemption in SGBs?

Premature redemption allows investors to exit before the 8-year maturity, under RBI guidelines.

Eligible after 5 years from issue date

Allowed only on semi-annual interest payment dates

Requires submission of a redemption request form

For this tranche, April 15, 2026, is the designated redemption date.

Alternative exit: Secondary market

Investors can also exit earlier via exchanges:

Sell on NSE/BSE (demat form)

Exit possible anytime

Prices may vary due to liquidity and demand

This route offers flexibility but may not always reflect true gold value.

Iranian crude re-enters global markets as US grants 60-day waiver; WTI slips below $74

Iranian crude re-enters global markets as US grants 60-day waiver; WTI slips below $74 WhatsApp gets a new boss: Kunal Shah to lead platform as Meta bets $900 million on CRED

WhatsApp gets a new boss: Kunal Shah to lead platform as Meta bets $900 million on CRED India wants to make more at home. So why are imports still surging?

India wants to make more at home. So why are imports still surging? From BrahMos to Akashteer: UAE explores buying India's frontline defence systems

From BrahMos to Akashteer: UAE explores buying India's frontline defence systems No rank on CV? IITs' new placement rule asks students to drop JEE, GATE scores. Here's why

No rank on CV? IITs' new placement rule asks students to drop JEE, GATE scores. Here's why Snap Specs Smart Glasses, Redmi Turbo 5 & OnePlus N Series Launch | Tech Gear EP 7 | Business Today

Snap Specs Smart Glasses, Redmi Turbo 5 & OnePlus N Series Launch | Tech Gear EP 7 | Business Today US Visa Rules Set For Major Overhaul | What It Means For 3.5 Lakh Indian Students

US Visa Rules Set For Major Overhaul | What It Means For 3.5 Lakh Indian Students Market Rally Resumes! Nifty Gains, Crude Falls | What's Next For Investors?

Market Rally Resumes! Nifty Gains, Crude Falls | What's Next For Investors? UAE In Talks To Buy BrahMos Missiles? | Big Boost For India's Defence Exports

UAE In Talks To Buy BrahMos Missiles? | Big Boost For India's Defence Exports CEO-Style Governance & Direct Action: CM Vijay’s First Month Decodes The Shift From Stalin’s Era!

CEO-Style Governance & Direct Action: CM Vijay’s First Month Decodes The Shift From Stalin’s Era! Sensex, Nifty trim gains but settle higher; what's ahead for investors?

Sensex, Nifty trim gains but settle higher; what's ahead for investors? Nearly 121x profit! HFCL promoter's Rs 10 Jio Platforms bet may yield a Rs 5,800 crore holding

Nearly 121x profit! HFCL promoter's Rs 10 Jio Platforms bet may yield a Rs 5,800 crore holding Explained: Open market share buybacks are back, what this means for Indian investors

Explained: Open market share buybacks are back, what this means for Indian investors Kirloskar Brothers shares jump 7%; key technical levels to watch out for

Kirloskar Brothers shares jump 7%; key technical levels to watch out for CONCOR shares set for 27% upside despite weak Q1 expectations, says Jefferies

CONCOR shares set for 27% upside despite weak Q1 expectations, says Jefferies