One should prioritise a stable core portfolio, disciplined equity–debt allocation, limited gold exposure, and a 9–12 month emergency fund in liquid assets.

One should prioritise a stable core portfolio, disciplined equity–debt allocation, limited gold exposure, and a 9–12 month emergency fund in liquid assets. One should prioritise a stable core portfolio, disciplined equity–debt allocation, limited gold exposure, and a 9–12 month emergency fund in liquid assets.

One should prioritise a stable core portfolio, disciplined equity–debt allocation, limited gold exposure, and a 9–12 month emergency fund in liquid assets.I am a 24-year-old salaried professional and have been investing in mutual funds for about three years. After switching to a new company six months ago, I’m now able to invest around ₹1 lakh per month in mutual funds. In addition, I invest ₹15,000 monthly in a gold accumulation scheme, where after 11 months I can purchase gold from a specific jeweller with zero making charges (GST applicable).

I began with a simple portfolio — one index fund, one large-cap fund and one small-cap fund — but over time I rotated funds and may have over-diversified. Currently, I’m running 10 active SIPs across small-cap, mid-cap, large & mid-cap, flexi-cap, sectoral, commodity and multi-asset funds. My risk appetite is medium-high to high, and my investment horizon is long term. However, I currently don’t have a formal emergency fund. I’m investing nearly 60% of my income and plan to build an emergency corpus over the next year by setting aside ₹10,000 per month in a savings account. I’m seeking advice on whether my portfolio structure is too fragmented and if I should consolidate funds across categories. Are sectoral and thematic funds appropriate at this stage, or should I focus more on core equity exposure? Also, is it prudent to continue aggressive investing while building an emergency fund gradually, or should the emergency fund be prioritised more strongly?

Advice by Subhendu Harichandan, Executive Director, Anand Rathi Wealth Limited

Hi, investor. You are currently 24 years old, investing ₹1 lakh per month across 10 mutual funds spanning equity, commodity and multi-asset categories, along with a ₹15,000 monthly gold accumulation plan. You intend to continue SIPs for the next 25 years and gradually build an emergency corpus by setting aside ₹10,000 per month.

At this stage, the objective should shift from adding more exposure to creating structure and balance. With a long investment horizon and a high savings rate, the foundation is strong — but portfolio efficiency, asset allocation clarity and emergency preparedness now become equally important as return maximisation.

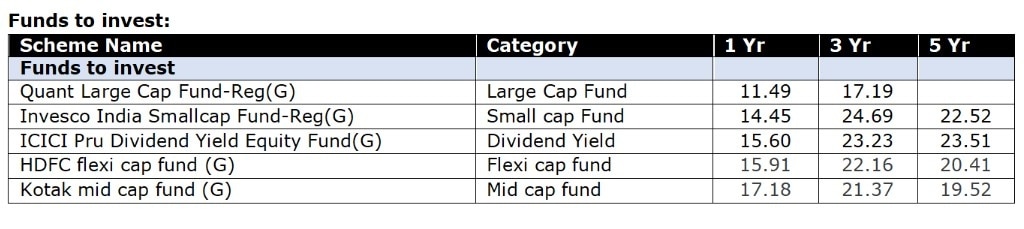

Before adding more funds or increasing SIP amounts, the focus should shift from expansion to structure. Early-career investors often drift into thematic, sectoral, hybrid or commodity funds in search of higher returns, but these categories tend to be cyclical, volatile and harder to manage within a disciplined asset allocation framework.

Current Scenario:

Portfolio Remarks:

, Wipro and Tech Mahindra have seen renewed buying interest.") IT stocks stage a comeback: Five factors supporting the strong upmove

IT stocks stage a comeback: Five factors supporting the strong upmove ‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’

‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’ 'Over 1 lakh attempts': CBSE claims cyberattacks by 'malicious actors' on revaluation portal

'Over 1 lakh attempts': CBSE claims cyberattacks by 'malicious actors' on revaluation portal Apollo Micro, Persistent Systems: These stocks set for more upside? Here what expert say

Apollo Micro, Persistent Systems: These stocks set for more upside? Here what expert say Annamalai-BJP breakup complete? Former 'Singham' has THIS plan for Tamil Nadu

Annamalai-BJP breakup complete? Former 'Singham' has THIS plan for Tamil Nadu Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services

Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early?

SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early? Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today

Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom

Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV

What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove

Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?

CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe? Hindalco Industries, APL Apollo Tubes shares: Axis Direct's top metal bets; check target prices, outlook

Hindalco Industries, APL Apollo Tubes shares: Axis Direct's top metal bets; check target prices, outlook L&T, BEML, Belrise, CG Power shares: Short-term target prices

L&T, BEML, Belrise, CG Power shares: Short-term target prices