In 2025, nearly 74% of gold loan borrowers had over ₹1 lakh in outstanding debt at the time of taking a new loan, up significantly from 2022.In 2025, nearly 74% of gold loan borrowers had over ₹1 lakh in outstanding debt at the time of taking a new loan, up significantly from 2022.

In 2025, nearly 74% of gold loan borrowers had over ₹1 lakh in outstanding debt at the time of taking a new loan, up significantly from 2022.In 2025, nearly 74% of gold loan borrowers had over ₹1 lakh in outstanding debt at the time of taking a new loan, up significantly from 2022.Gold loan trends: India’s gold loan market is witnessing a structural shift, transforming from a small-ticket emergency product into a mainstream credit category, with sharp growth and rising borrower exposure raising both opportunities and risks.

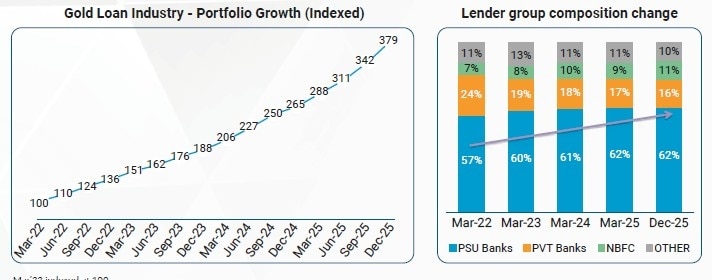

According to TransUnion CIBIL’s Gold Loan Landscape Report (April 2026), the gold loan portfolio has expanded 3.8 times since March 2022, making it one of the fastest-growing segments in retail lending. The surge has pushed gold loans to become the second-largest component of India’s retail credit portfolio after housing loans, underscoring their growing relevance in the financial system.

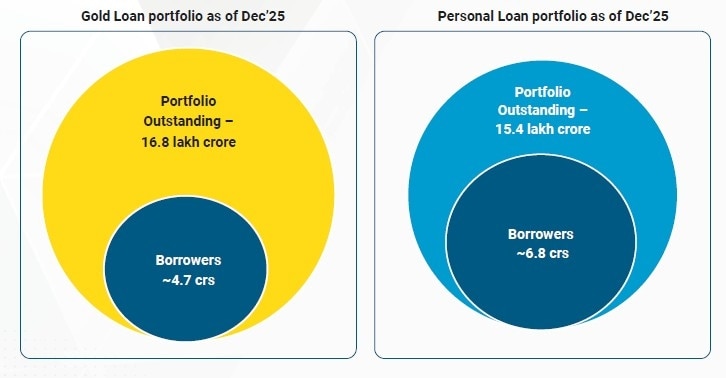

A key highlight of this growth is the sharp increase in borrower leverage. The average outstanding per borrower has risen from ₹1.9 lakh to ₹3.1 lakh, while the average ticket size has more than doubled to nearly ₹2 lakh. This indicates that borrowers are not only opting for gold loans more frequently but are also taking larger loans against their pledged gold.

Borrowing patterns

Traditionally seen as a fallback option during financial stress, gold loans are now increasingly being used as part of a broader borrowing strategy. The report notes a clear rise in borrowers who already have existing secured and unsecured loans in their credit portfolios.

In 2025, nearly 74% of gold loan borrowers had over ₹1 lakh in outstanding debt at the time of taking a new loan, up significantly from 2022. This trend suggests that gold loans are being used alongside products such as personal loans, credit cards, and other retail credit facilities, rather than as a last resort.

At the same time, the share of repeat borrowers and multiple loan accounts has increased, pointing to a growing dependence on gold-backed financing for liquidity needs.\

Bhavesh Jain, MD and CEO, TransUnion CIBIL, said, “Gold has always held deep financial and cultural relevance in India, but what we are seeing now is a structural shift in how gold-backed borrowing is being used. Gold loans are increasingly becoming a mainstream, organised and accessible form of secured credit. Their rapid growth reflects both lender confidence and rising consumer acceptance.

“What is particularly notable is that the segment is drawing more borrowers with stronger credit profiles, larger ticket sizes and repeat usage. This is an indication that gold loans are no longer being used only for short-term liquidity needs but are becoming part of broader household borrowing behaviour,” he added.

NBFCs lead, banks follow

Non-banking financial companies (NBFCs) and public sector banks (PSUs) have emerged as the primary drivers of this expansion. NBFCs, in particular, have recorded the fastest growth, benefiting from their strong distribution networks and faster loan processing capabilities.

Private banks, while present, have grown at a comparatively slower pace, indicating a more cautious approach to this segment.

Gold loans vs personal loans

The report indicates that gold loans are increasingly resembling personal loans in usage, but with distinct structural differences. While personal loans remain unsecured, gold loans—backed by collateral—are now being used beyond emergency needs for planned liquidity and credit stacking. Borrowers are taking gold loans alongside existing products, leading to higher wallet leverage and multiple concurrent loans. Notably, gold loan outstanding per borrower is now higher than personal loans, despite a smaller borrower base. The shift toward repeat borrowing, higher ticket sizes, and integration into overall credit portfolios suggests gold loans are evolving into a strategic, quasi-personal loan alternative, especially for credit-active customers.

Risk signals begin to emerge

Despite the robust growth, the report flags emerging stress indicators. Borrowers with higher exposure levels—especially above ₹2.5 lakh—show significantly higher delinquency risks, nearly 2.2 times compared to lower exposure segments.

Additional risk factors include:

High concentration of gold loans within a borrower’s credit portfolio

Rising unsecured debt alongside gold loans

Recent repayment delinquencies

These trends highlight a shift toward higher leverage and increased credit risk, especially as borrowers juggle multiple credit products.

ALSO READ: Akshaya Tritiya: ₹96,000 got you 10 gm gold in 2025 but what it gets you in 2026 is shocking

Women borrowers and new regions fuel demand

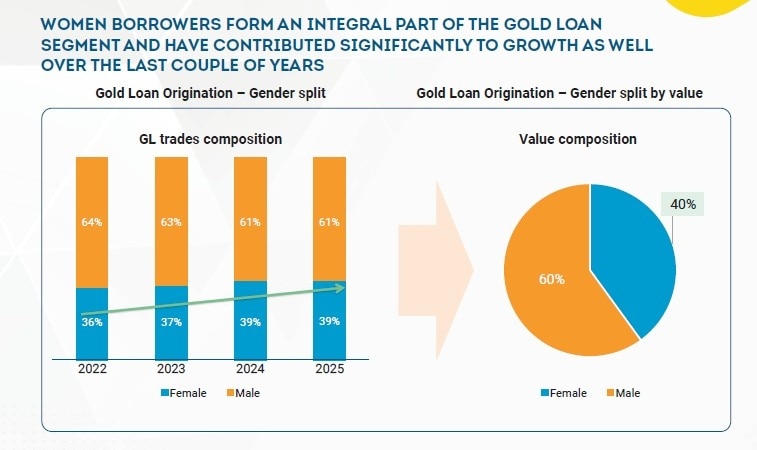

Another notable trend is the rising participation of women borrowers, who now account for nearly 40% of gold loan volumes. Geographically, while southern states continue to dominate, high growth is being recorded in northern and western regions, including Uttar Pradesh, Rajasthan, and Gujarat.

Policy focus and outlook

With the market expanding rapidly, regulators have tightened norms, including tiered loan-to-value (LTV) limits and stricter borrower-level assessments. Lenders are increasingly expected to evaluate total borrower exposure, not just the value of pledged gold.

The sharp rise in gold loans reflects their growing role as a flexible, fast-disbursing credit instrument. However, the simultaneous increase in ticket sizes and borrower leverage suggests that sustaining this growth will require stronger underwriting, risk-based pricing, and closer monitoring of borrower behaviour.

ALSO READ: Gold slump: Why your safe-haven bet fell 12% in March — what it means for you

The peace deal to be signed today: Trump announces imminent US-Iran pact

The peace deal to be signed today: Trump announces imminent US-Iran pact 'Rubio's remarks will further inflame anti-US...': American expert after Indian sailors' deaths

'Rubio's remarks will further inflame anti-US...': American expert after Indian sailors' deaths 'Blaming Infosys, Murthy, Nandan is misplaced': Startup founder says India's real AI problem is...

'Blaming Infosys, Murthy, Nandan is misplaced': Startup founder says India's real AI problem is... used the post to highlight a wide range of projects funded by Tata Trusts, spanning healthcare, education, rural development and scientific research.") ‘No hype, no publicity...’: Tata Trusts CEO counters ‘chaos’ narrative with philanthropy push

‘No hype, no publicity...’: Tata Trusts CEO counters ‘chaos’ narrative with philanthropy push 'In next 24 hours...': Pak PM Shehbaz Sharif announces imminent US-Iran peace deal

'In next 24 hours...': Pak PM Shehbaz Sharif announces imminent US-Iran peace deal Anti-Defection Law Explainer: What Is The 'Maharashtra Model' & The Legal Truth Of The 2/3rd Rule!

Anti-Defection Law Explainer: What Is The 'Maharashtra Model' & The Legal Truth Of The 2/3rd Rule! Piyush Goyal On India’s R&D Challenge: Why Private Sector Innovation Must Accelerate

Piyush Goyal On India’s R&D Challenge: Why Private Sector Innovation Must Accelerate EAM Jaishankar On Trump 2.0: ‘The World Didn’t Expect It To Be This Radical’

EAM Jaishankar On Trump 2.0: ‘The World Didn’t Expect It To Be This Radical’ India Today’s SIT Sting: Delhi’s Rs 500 Cr Expired Cosmetics Racket Selling Fake Branded Products

India Today’s SIT Sting: Delhi’s Rs 500 Cr Expired Cosmetics Racket Selling Fake Branded Products "Before 2014, India's Image Was A Country Of Poor & Corrupt": Minister Shekhawat To India Today

"Before 2014, India's Image Was A Country Of Poor & Corrupt": Minister Shekhawat To India Today SBI shares likely to hit fresh record high in a year - Rationale explained with target price

SBI shares likely to hit fresh record high in a year - Rationale explained with target price Physicswallah, Meesho, Belrise, MOFSL: 10 fresh stock ideas with upto 63% upside potential

Physicswallah, Meesho, Belrise, MOFSL: 10 fresh stock ideas with upto 63% upside potential Is CEA hinting at no urgency to tweak capital gains taxes on stocks? What has he said on topic of capital market taxation

Is CEA hinting at no urgency to tweak capital gains taxes on stocks? What has he said on topic of capital market taxation Why Motilal Oswal's Raamdeo Agrawal believes passive investing will gain ground

Why Motilal Oswal's Raamdeo Agrawal believes passive investing will gain ground Avalon, Dixon Tech, Kaynes Tech, Amber, Syrma SGS, PG Technoplast: 2 top EMS picks

Avalon, Dixon Tech, Kaynes Tech, Amber, Syrma SGS, PG Technoplast: 2 top EMS picks