Instagram and YouTube are flooded with short-form vertical video content, proving that India has emerged as one of the world's fastest-growing markets for microdrama and vertical-video apps.Instagram and YouTube are flooded with short-form vertical video content, proving that India has emerged as one of the world's fastest-growing markets for microdrama and vertical-video apps.

Instagram and YouTube are flooded with short-form vertical video content, proving that India has emerged as one of the world's fastest-growing markets for microdrama and vertical-video apps.Instagram and YouTube are flooded with short-form vertical video content, proving that India has emerged as one of the world's fastest-growing markets for microdrama and vertical-video apps.Buried somewhere inside The Economic Times this week was a report about Pocket FM shutting down Pocket TV, its vertical video microdrama platform. The timing of the decision is significant, as it came right ahead of a planned initial public offering (IPO). On the face of it, it looked like a routine strategic refocus. The company said it wanted to concentrate on its core audio business and overseas expansion.

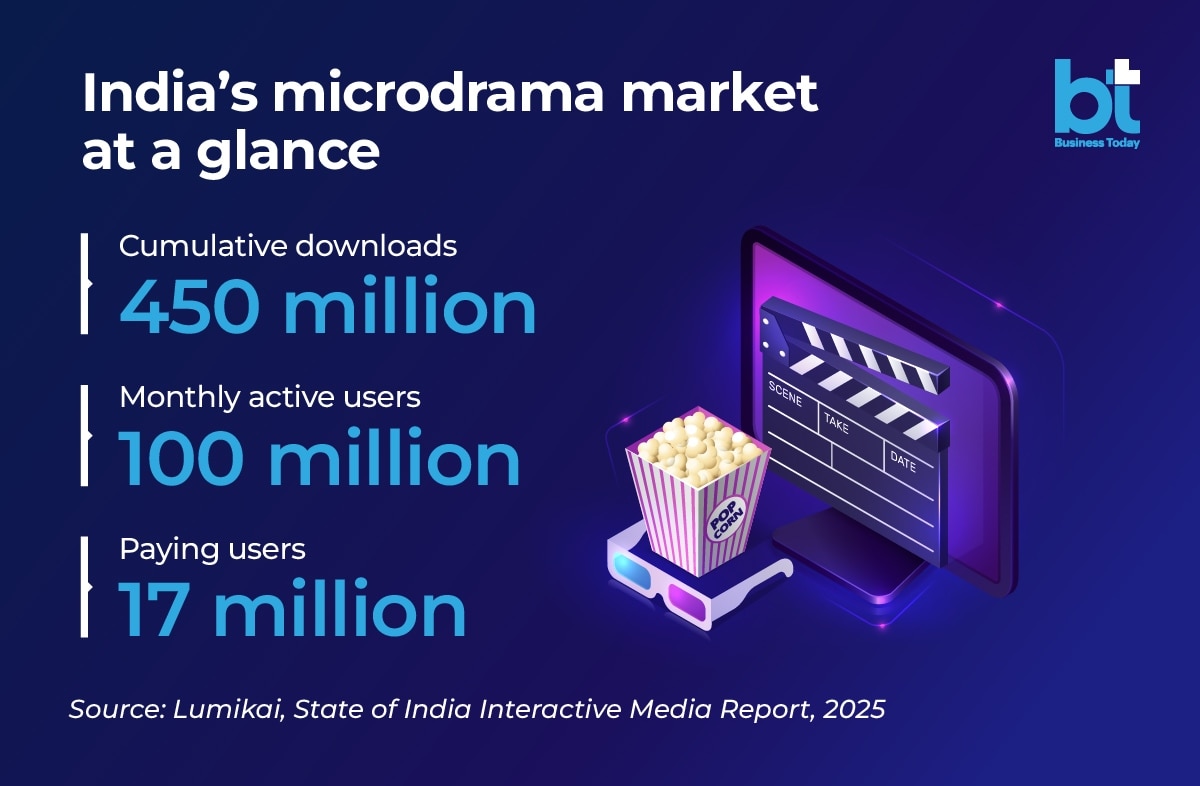

Pocket FM is walking away from one of the hottest formats in media just as everyone else seems to be rushing in. According to Lumikai's State of India Interactive Media Report 2025, the category generated over $300 million in revenue in 2025, with 100 million monthly active users and 17 million paying users. These metrics have encouraged everyone, from JioHotstar and ZEE to Kuku TV and a new crop of venture-backed start-ups, to chase the opportunity.

Yet, even as rivals double down on the format, the decision of one of its earliest movers to walk away points to a larger industry tension.

If audience demand is growing and fresh capital continues to flow into the sector, what explains the retreat?

Where does the money come from

Instagram and YouTube are flooded with short-form vertical video content, proving that India has emerged as one of the world's fastest-growing markets for microdrama and vertical-video apps. According to industry estimates, India became the largest market globally for short-drama app downloads, recording over 21 million installs in a single month. Lumikai estimates the category has already crossed 450 million cumulative downloads.

The numbers suggest there is no shortage of demand for the format, and its popularity is not difficult to explain. India is one of the world's largest mobile internet markets, data remains among the cheapest globally, and years of scrolling through Instagram Reels and YouTube Shorts have already conditioned viewers to consume entertainment in short bursts.

However, audience interest may not naturally translate into profits. Microdrama platforms typically rely on a mix of revenue models. Most allow viewers to watch the opening episodes for free before asking them to unlock subsequent chapters using virtual coins, subscribe for unlimited access or watch advertisements to continue. The approach resembles mobile gaming more than traditional television, where a small but engaged segment of users contributes a disproportionate share of revenue. The model has worked in markets such as China, but whether it can be replicated at scale in India's more price-sensitive digital ecosystem remains an open question.

While most players publicise downloads and watch time, few disclose profitability. That makes it difficult to ascertain whether user growth is translating into sustainable returns.

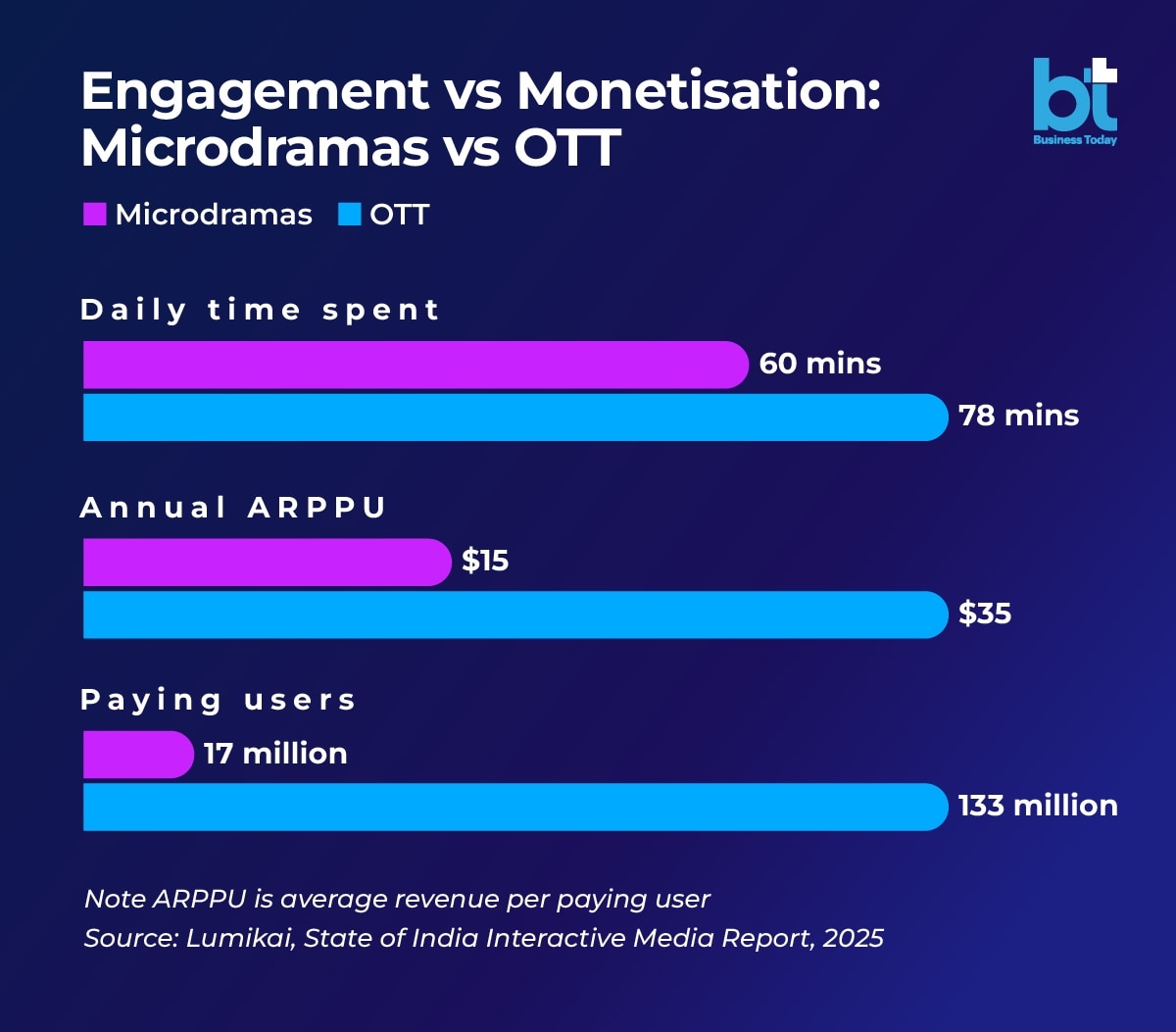

The contrast is reflected in the numbers. According to Lumikai, users spend around 60 minutes a day on microdrama apps, close to the 78 minutes spent on over-the-top (OTT) platforms. Yet average revenue per paying user remains significantly lower at $15, compared with $35 for OTT services.

Platforms are already experimenting with different ways to convert that engagement into revenue. Some rely on subscriptions, others on virtual coins and pay-per-episode purchases, while several are combining advertising with paid access. A few have also begun partnering with telecom operators, bundling access with mobile plans to reach users who may be reluctant to subscribe directly. The variety of approaches underlines an industry that is still searching for the most effective commercial model.

Rising competition

Unlike premium OTT originals and conventional television, microdramas do not require large production budgets or lengthy development cycles. Technology is accelerating this shift. AI-assisted workflows are reducing the time required for scripting, dubbing, localisation and editing, allowing platforms to produce larger volumes of content across multiple languages. Lower production costs make experimentation easier, but they also reduce barriers to entry. As creating content becomes simpler, attracting and retaining audiences becomes a more difficult competitive advantage.

The short video segment has players such as Kuku FM's Kuku TV, Amazon MX Player's MX Fatafat, ZEE Entertainment Enterprises' Bullet, alongside startups such as ReelSaga, Quick TV, Story TV, Chai Shots and others. Chinese-origin heavyweights like ReelShort and DramaBox have also entered with dubbed catalogues.

As more companies enter the category, the challenge shifts from creating content to getting noticed. Food delivery, edtech, and OTT platforms all experienced similar phases in which competition intensified, and distribution became as important as the product itself.

While Pocket FM has attributed its decision to prioritise audio as a strategic refocus, its exit comes at a time when the microdrama market is becoming crowded. However, audio also offers structural advantages over video. Production costs are significantly lower, stories can be released at a faster pace, and successful titles often have a longer shelf life because they are not tied to expensive visual production. Pocket FM has also invested heavily in AI tools to speed up scripting, localisation and publishing. According to the company, these tools have reduced content-creation timelines by more than 90%, enabling creators to release episodes more quickly and monetise them sooner.

The China Playbook

China has already established that the format can become a thriving entertainment business.

It emerged from China's "duanju" ecosystem before spreading globally. Platforms such as ReelShort and DramaBox have demonstrated that mobile-first storytelling can generate substantial revenues through subscriptions, coin systems, and pay-per-episode models.

China's experience showed not just that audiences enjoyed the format, but that they were willing to keep paying for it. Instead of relying solely on monthly subscriptions, many platforms built businesses around frequent, low-value purchases, encouraging viewers to unlock one episode after another. That commercial model has since travelled beyond China, with platforms adapting it for markets in the US, Southeast Asia and, increasingly, India.

Former Hollywood studio executives, venture investors and even major entertainment companies are investing in microdrama platforms. Media reports suggest that Disney selected DramaBox's parent company for its accelerator programme.

Despite the global success, India presents a different challenge.

The download data indicates that Indians are interested in melodrama as a genre, but it says little about their willingness to pay. Unlike China, where users have shown a greater willingness to pay for serialised digital content, historically, Indian digital entertainment has been advertising-led and price-sensitive. Monetisation remains the Achilles' heel of most content businesses.

Even Netflix, which entered India with premium pricing, was eventually forced to rethink its strategy and introduce lower-cost plans to broaden adoption. That reality is shaping business strategy across the sector. Rather than relying on a single source of revenue, platforms are increasingly mixing subscriptions, advertising and distribution partnerships to broaden their reach while lowering the barrier to payment. The focus has shifted from simply attracting viewers to finding pricing models that work in a market where free alternatives are plentiful.

India has already demonstrated that there is an audience for microdramas. What remains unsettled is the business model. The platforms that crack pricing, distribution, and monetisation will shape the next phase of the industry. Until then, downloads and watch time will tell only part of the story.

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K crore 'You're in the wrong chair': When Gita Gopinath faced bias as IMF chief economist

'You're in the wrong chair': When Gita Gopinath faced bias as IMF chief economist Can India monetise microdramas as the market booms but profitability remains elusive?

Can India monetise microdramas as the market booms but profitability remains elusive? India needs its own DeepSeek to avoid AI dependence, warns Bernstein

India needs its own DeepSeek to avoid AI dependence, warns Bernstein.") Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock WatchInfosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K croreLast chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock WatchInfosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K croreLast chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure  JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential

JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet

Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet