vs NRE vs US Fixed Deposits: Which option makes more sense for NRIs?") Unlike NRE deposits, which are maintained in Indian rupees, FCNR(B) deposits are denominated in foreign currencies such as the US dollar, pound sterling, euro and Japanese yen.

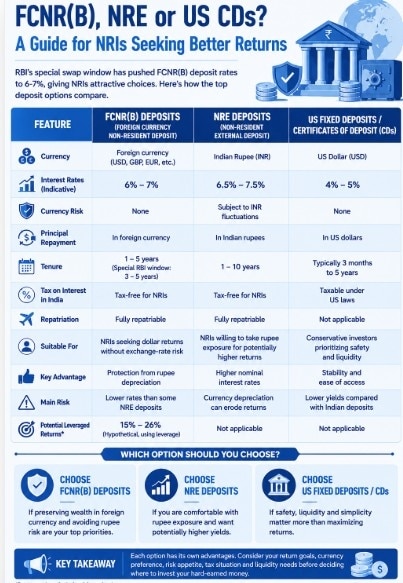

Unlike NRE deposits, which are maintained in Indian rupees, FCNR(B) deposits are denominated in foreign currencies such as the US dollar, pound sterling, euro and Japanese yen.The Reserve Bank of India's (RBI) latest measures to attract foreign currency inflows have made Foreign Currency Non-Resident Bank [FCNR(B)] deposits more attractive, prompting many Non-Resident Indians (NRIs) to reassess where they should park their money.

With Indian banks raising FCNR(B) deposit rates to 6-7%, the debate is increasingly shifting to how these deposits compare with traditional NRE fixed deposits and fixed-income products available in the US.

FCNR(B) rates climb

The RBI recently introduced a special swap facility that allows banks to mobilise FCNR(B) deposits for three to five years while the central bank bears the hedging cost. Banks also get exemptions from Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements, making such deposits more attractive.

According to a report by Motilal Oswal Financial Services, large banks have already raised FCNR(B) rates to around 6%, while some smaller lenders are offering close to 7%.

The brokerage expects these measures to bring in $40-50 billion of foreign exchange inflows during FY27.

FCNR(B) deposits

Unlike NRE deposits, which are maintained in Indian rupees, FCNR(B) deposits are denominated in foreign currencies such as the US dollar, pound sterling, euro and Japanese yen.

This means both principal and interest are repaid in the same foreign currency, shielding depositors from rupee depreciation.

For NRIs concerned about the weakening of the rupee over the long term, this feature can be a significant advantage.

NRE deposits may offer higher rates, but carry exchange-rate risk

NRE fixed deposits continue to remain popular because they offer tax-free interest and full repatriation.

MUST READ: FCNR deposit rates rise after RBI swap window; AU SFB tops 7% on USD deposits

Many banks currently offer rates of 6.5-7.5% on rupee-denominated NRE deposits. However, the returns ultimately depend on the movement of the rupee against the investor's home currency.

A sharp depreciation in the rupee can reduce the effective return for overseas investors when funds are converted back into dollars or other foreign currencies.

US fixed deposits

Three-year certificates of deposit (CDs) and fixed-income products in the US generally offer returns in the range of 4-5%.

While these products provide safety and eliminate currency-related concerns for US-based NRIs, the yield advantage has narrowed following the increase in FCNR(B) rates.

As a result, some wealth managers believe FCNR(B) deposits could emerge as an attractive middle ground between higher-yielding rupee deposits and lower-yielding US instruments.

MUST READ: FD schemes 1-year vs 3-year vs 5-year: Which tenure offers the best returns in 2026?

Can FCNR(B) deposits deliver "equity-like" returns?

Recent analyses have highlighted another dimension of the scheme. By borrowing abroad at relatively low rates and deploying those funds into higher-yielding FCNR(B) deposits, NRIs may potentially enhance returns through leverage.

According to Motilal Oswal, customers could earn returns of 15-26% on leveraged FCNR(B) deposits, while banks could gain an additional spread benefit of around 65 basis points.

Similar calculations published recently have suggested that under certain hypothetical scenarios involving leverage, annualised returns could approach equity-like levels.

However, such strategies involve borrowing and are suitable only for sophisticated investors.

Which option is better?

The answer depends largely on an investor's priorities.

Those seeking protection from currency fluctuations may find FCNR(B) deposits attractive. Investors willing to take rupee exposure in exchange for potentially higher returns may prefer NRE deposits, while those prioritising safety and simplicity may continue to favour US fixed deposits.

With Indian banks now offering some of their highest FCNR(B) rates in years, NRIs have more choices than they have had in a long time.

MUST READ: FD schemes: RBI draft rules aim to boost transparency in investments; what it means for you

TCS Q1 FY27 results: Rs 12 per share interim dividend announced; check record date

TCS Q1 FY27 results: Rs 12 per share interim dividend announced; check record date India's Nanda Devi only inbound LPG vessel at Hormuz as dark transits rise

India's Nanda Devi only inbound LPG vessel at Hormuz as dark transits rise  TCS Q1 Results LIVE Updates: Rs 12 dividend approved; check payment date, record date, earnings highlights | 'FY27 begins with growth; wins multiple AI deals'

TCS Q1 Results LIVE Updates: Rs 12 dividend approved; check payment date, record date, earnings highlights | 'FY27 begins with growth; wins multiple AI deals'  From 'Islamic Republic of Japan' to 'Putin': Trump's latest mix-ups spark fresh buzz as Iran tensions rise

From 'Islamic Republic of Japan' to 'Putin': Trump's latest mix-ups spark fresh buzz as Iran tensions rise Still have a ₹2,000 note? RBI says it's still valid & here's how you can exchange it

Still have a ₹2,000 note? RBI says it's still valid & here's how you can exchange it PM Modi Heads to Australia After Indonesia Visit, Eyes Uranium & Defence Cooperation

PM Modi Heads to Australia After Indonesia Visit, Eyes Uranium & Defence Cooperation Trump Declares Iran MoU 'Over' As Fresh US Strikes Escalate West Asia Tensions

Trump Declares Iran MoU 'Over' As Fresh US Strikes Escalate West Asia Tensions Novo Nordisk Launches Awiqli, World’s First Weekly Basal Insulin In India

Novo Nordisk Launches Awiqli, World’s First Weekly Basal Insulin In India Air India CEO Appointment Delayed; Tata Sets Up Interim Committee Amid Leadership Uncertainty

Air India CEO Appointment Delayed; Tata Sets Up Interim Committee Amid Leadership Uncertainty JD Vance Reveals The Secret Iran Deal: "We Punch Back Harder If They Shoot At Ships"

JD Vance Reveals The Secret Iran Deal: "We Punch Back Harder If They Shoot At Ships" TCS Q1 results: Net profit rises to Rs 13,349 crore, revenue up 14%| Quarterly earnings detailsTCS Q1 FY27 results: Rs 12 per share interim dividend announced; check record date

TCS Q1 results: Net profit rises to Rs 13,349 crore, revenue up 14%| Quarterly earnings detailsTCS Q1 FY27 results: Rs 12 per share interim dividend announced; check record date SBI Funds, NSE, Jio Platforms: Will mega IPOs derail secondary market momentum?

SBI Funds, NSE, Jio Platforms: Will mega IPOs derail secondary market momentum? Why Choice International shares surged nearly 9% today

Why Choice International shares surged nearly 9% today Tata Power, Adani Power, Polycab, Berger Paints: Expert decodes trading strategy

Tata Power, Adani Power, Polycab, Berger Paints: Expert decodes trading strategy