One should remember that interest earned on FDs is treated as "Income from Other Sources" under income tax rules and is added to a depositor’s total annual income.One should remember that interest earned on FDs is treated as "Income from Other Sources" under income tax rules and is added to a depositor’s total annual income.

One should remember that interest earned on FDs is treated as "Income from Other Sources" under income tax rules and is added to a depositor’s total annual income.One should remember that interest earned on FDs is treated as "Income from Other Sources" under income tax rules and is added to a depositor’s total annual income.Fixed deposits (FDs) continue to remain a preferred investment avenue for conservative investors seeking stable returns and capital protection amid ongoing market volatility. While equity markets fluctuate, FDs offer predictable returns and are widely used for emergency funds, retirement planning, and short-term financial goals.

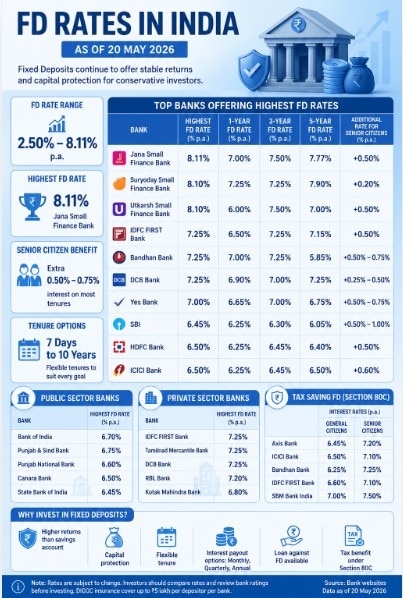

As of May 20, 2026, FD interest rates across scheduled banks range between 2.50% and 8.11% annually, depending on tenure and institution type. Small finance banks currently dominate the higher-yield segment, while public and private sector lenders continue to offer competitive rates for mainstream depositors.

Current FD rates

Among institutions offering the highest returns, Jana Small Finance Bank leads with a maximum FD rate of 8.11%, followed by Suryoday Small Finance Bank and Utkarsh Small Finance Bank, both offering up to 8.10%.

The higher rates offered by small finance banks have attracted investor interest, although experts often advise depositors to evaluate factors such as institution ratings, liquidity needs, and deposit insurance coverage before chasing returns.

Among private sector lenders, banks such as IDFC FIRST Bank, Tamilnad Mercantile Bank, DCB Bank, Bandhan Bank, and RBL Bank are offering rates ranging from around 7% to 7.25% on select tenures.

Large private sector lenders remain relatively conservative in their offerings. HDFC Bank and ICICI Bank currently provide maximum FD rates around 6.50%, while Kotak Mahindra Bank offers up to 6.80%.

Public sector banks continue to offer relatively lower but stable returns. Bank of India and Punjab & Sind Bank offer rates up to 6.70%-6.75%, while State Bank of India currently offers up to 6.45%.

Senior citizens continue to receive an additional interest benefit of around 0.50 percentage points, with certain banks offering higher premiums in select cases.

FDs remain popular because of several features beyond fixed returns. Tenures range from seven days to ten years, allowing flexibility across investment horizons. Investors can also choose periodic interest payouts, reinvestment options, premature withdrawals with penalties, and loans against deposits. Tax-saving FDs additionally offer deductions under Section 80C of the Income Tax Act.

FD and taxation

FDs are often viewed as one of the safest investment options because they offer predictable returns and guaranteed interest. However, many investors are surprised when the maturity amount or interest credited to their account falls short of expectations due to tax-related deductions. A common misconception is that the interest earned on an FD is tax-free apart from the TDS deducted by banks. In reality, the taxation process is more detailed.

Interest earned on FDs is treated as "Income from Other Sources" under income tax rules and is added to a depositor’s total annual income. The earnings are then taxed according to the individual's applicable income-tax slab rather than at a separate fixed rate.

For example, if a salaried individual earns additional income through FDs, that interest increases total taxable income and may push overall tax liability higher.

MUST READ: Bank of India revises FD Rates: 3-year deposits now offer 6.7%; here’s how it stacks up

Another point often overlooked is that TDS is not the final tax. Banks deduct tax only after interest crosses specified limits. Currently, TDS applies when annual FD interest exceeds ₹40,000 for regular depositors and ₹50,000 for senior citizens. If PAN details are unavailable or not properly linked, banks may deduct a higher TDS amount.

Tax treatment can become more complex for cumulative FDs, as interest is taxable every year on an accrual basis even if payment is received later.

Eligible individuals whose income falls below taxable limits can submit Form 15G or Form 15H to avoid TDS deductions. Understanding these rules can help investors estimate post-tax returns more accurately and avoid surprises at maturity.

MUST READ: Special FDs vs regular fixed deposits: Which option makes more sense for investors?

of up to 148,905,525 equity shares by the selling shareholders of the company.") NSE files DRHP to launch IPO: 6% stake sale via OFS route, check all key details

NSE files DRHP to launch IPO: 6% stake sale via OFS route, check all key details 'India has a great friend in White House': Trump after meeting Modi, says trade deal is 'very close'

'India has a great friend in White House': Trump after meeting Modi, says trade deal is 'very close'.") India, EU target year-end FTA as Modi meets Ursula von der Leyen at G7

India, EU target year-end FTA as Modi meets Ursula von der Leyen at G7 UK-India free trade agreement to come into force on July 15; whisky tariffs to fall from 150% to 40%

UK-India free trade agreement to come into force on July 15; whisky tariffs to fall from 150% to 40% Pune–Nashik direct semi-high-speed rail line scrapped: Vaishnaw announces new routes

Pune–Nashik direct semi-high-speed rail line scrapped: Vaishnaw announces new routes How This Fund Outperformed the Benchmark for 10 Years Straight

How This Fund Outperformed the Benchmark for 10 Years Straight IDBI Bank Led PSU Lenders Higher As Rally Deepened Into The Broader Market. Oil Fell. Rupee Rose

IDBI Bank Led PSU Lenders Higher As Rally Deepened Into The Broader Market. Oil Fell. Rupee Rose #BTSustainabilityAwards LIVE: ESG Over Profits? Redefining Business For Long -Term Value

#BTSustainabilityAwards LIVE: ESG Over Profits? Redefining Business For Long -Term Value Is This The Right Time To Buy IT Stocks? Explained By Amit Khurana

Is This The Right Time To Buy IT Stocks? Explained By Amit Khurana NSE IPO Countdown Begins: Why Experts Say Fresh Buying In BSE Is Risky

NSE IPO Countdown Begins: Why Experts Say Fresh Buying In BSE Is Risky Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty down 30 pts; key levels to watch

Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty down 30 pts; key levels to watch Top stocks in news: Bosch Home, Apollo Hospitals, RVNL, Lupin, Lemon Tree, RailTail, HFCLNSE files DRHP to launch IPO: 6% stake sale via OFS route, check all key details

Top stocks in news: Bosch Home, Apollo Hospitals, RVNL, Lupin, Lemon Tree, RailTail, HFCLNSE files DRHP to launch IPO: 6% stake sale via OFS route, check all key details SEBI warns investors against trading unlisted shares on unauthorised platforms

SEBI warns investors against trading unlisted shares on unauthorised platforms BT Closing Bell | Sensex, Nifty end higher for fourth session; more upside or rangebound movement ahead?

BT Closing Bell | Sensex, Nifty end higher for fourth session; more upside or rangebound movement ahead?